Quarterly Market Outlook

Is there such a thing as a “safe” investment?

As investors, we want the comfort of safety. We’re human after all, and safety ranks second in Maslow’s hierarchy of needs, just after our basic physiological needs. The irony is that this inherent need for safety is the very thing that gets us into trouble. It’s this need that draws us to investments that promise returns with “no risk”.

In the world of finance, risk and return are the yin and yang. They exist on opposite realms but balance each other out. Every investment has its risks; it’s just a matter of how high or low the level of risk is. The term “safe investment” is an oxymoron, like “living dead” or “exact estimate”. A zero-risk investment can’t be an actual thing because it is impossible. If you see it written on a brochure, scratch it out and write “relatively safe investment”. There, fixed it.

Our idea of “safe” has been challenged. Swiss banking is known for its stability (and tight privacy laws), but even the biggest institutions in the most financially stable countries aren’t immune to risk. Credit Suisse, founded in 1856 to help fund the Swiss railways, recently found itself on the brink of collapse, and the Swiss government had to intervene and orchestrate a bailout by UBS to the tune of US$3.25 billion. Credit Suisse had to writedown US$17 billion worth of its AT1 bonds, a slap in the face to the reputation of bonds as the safest investment.

On the other side of the world, the abrupt collapse of the US$212 billion Silicon Valley Bank (SVB) sent shockwaves throughout the finance world. SVB was the darling of the tech industry, lending money to start ups who were turned away by conventional banks. Intoxicated by the highly lucrative tech industry, the bank turned the earnings from these loans into bonds (again, bonds!) which it then stretched out into longer terms. In its shortsightedness, SVB failed to address the risk of rising interest rates, which pushed down the market price of these longer-term bonds.

We were all caught by surprise… or were we, really? Let’s be honest with ourselves. These collapses were largely the result of poor risk management and bad decision-making. Investors place a huge amount of trust in the hands of key decision makers, which we may end up paying for in the end. It’s our responsibility to carry out our own research and due diligence before investing. We can’t be blinded by the prospects of the next “in” thing.

Nothing is sacred

So, if that’s not safe, what is? Nothing! But that doesn’t mean we should all withdraw all our money and run for the hills with bags of cash. Instead, our idea of “safe” needs to change. We really need to stop looking for that one safe investment, that holy grail to throw all our money at. Instead, we should change our approach to investing to reduce the overall risk through diversification , also known as putting your eggs in multiple baskets. This isn’t a new concept, but it is one that investors should be encouraged to take.

Spreading your risk

Diversification reduces risk by investing in various vehicles across different financial instruments, industries, and other categories. Although market risk is unavoidable, diversifying your investments drastically reduces unsystematic risk. In other words, you manage the risks that are within your control by adjusting the level of exposure within and across asset classes through proper asset allocation.

Diversifying across asset classes

A well-diversified portfolio is made up of different types of investments. The three main asset classes are stocks, bonds and cash alternatives. Some investors also add other investments, such as real estate and commodities like gold and coal to their portfolios. Each asset class tends to respond differently to similar market conditions. The gains made from one asset class would be able to partially offset the losses from another at the very least.

A non-financial example is Skittles. Ever wonder why you can’t find mass-produced single flavour packs? You like the red and green Skittles, while someone else only likes the purple ones. Yellow is the least popular flavour, according to the company website, but some people (like the writer) still like them. The company diversifies their Skittles to optimise their inventory and manufacturing and to reach as wide a market as possible. Similarly, in your portfolio, you pick a little bit of everything.

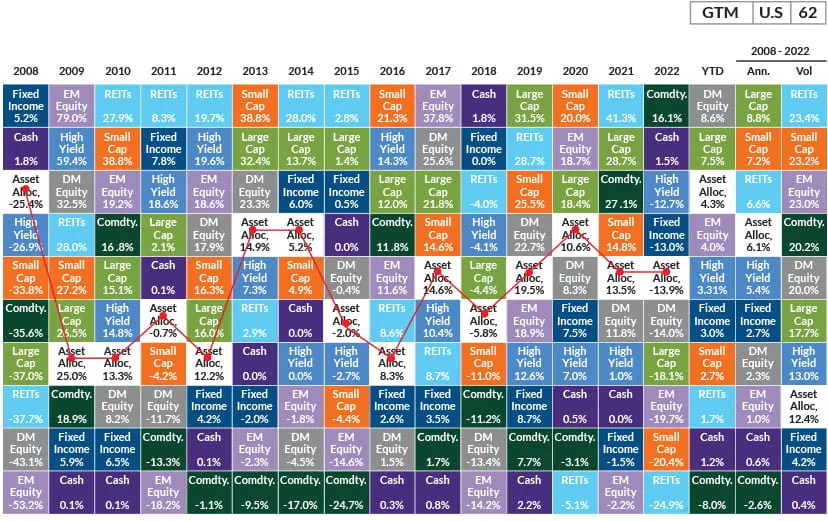

This chart below shows how having a well-diversified portfolio protects you from crazy fluctuations. Each coloured box represents an asset class, while the white box is a diversified position. Imagine if you had dumped all your money into equities. You would be a very, very stressed investor.

In the last two columns on the right, you can see the annualised returns and volume. Your diversified portfolio still ranked among the top performers, without having to shift that much volatility.

Asset class returns

Large cap: S&P 500, Small cap: Russell 2000, EM Equity: MSCI EME, DM Equity: MSCI EAFE, Comdty: Bloomberg Commodity Index, High Yield: Bloomberg Global HY Index, Fixed Income: Bloomberg US Aggregate, REITs: NAREIT Equity REIT Index, Cash: Bloomberg 1-3m Treasury. The “Asset Allocation” portfolio assumes the following weights: 25% in the S&P 500, 10% in the Russell 2000, 15% in the MSCI EAFE, 5% in the MSCI EME, 25% in the Bloomberg US Aggregate, 5% in the Bloomberg 1-3 Treasury, 5% in the Bloomberg Global Yield Index, 5% in the Bloomberg Commodity Index and 5% in the NAREIT Equity REIT Index. Balanced portfolio assumes annual rebalancing. Annualized (Ann.) return and volatility (Vol.) represents period from 12/31/2007 to 12/31/2022. All data represents total return for stated period. The “Asset Allocation” portfolio is for illustrative purposes only. Past performance is no indicative of future returns.

Guide to the Markets - U.S. Data are as of March 31, 2023.

Diversifying within an asset class

Now that you’ve picked your range of assets classes, you can diversify within the asset class. You can diversify by the size of the companies, by geography (domestic or international), and by industry and sector. Mutual funds or exchange-traded funds are a great way to diversify within an asset class without having to comb through the financials of each company you are investing in.

It’s just more fun

Diversification is also way more fun because you get to research new investments as the market improves in sophistication and accessibility, if that sort of stuff floats your boat. For example, the range of Environment, Governance and Social (ESG) focused funds has increased over the past decade, giving the investor more options. New opportunities will present themselves in your research, which your Relationship Manager will be happy to help decipher. Your Relationship Manager will also help you build a well-diversified portfolio based on your long-term goals, risk appetite and needs.

Get in touch with RHB Premier today.

This publication has been prepared by RHB Bank Berhad and is solely for your information only. It may not be copied, published, circulated, reproduced or distributed in whole or part to any person without the prior written consent of RHB Bank Berhad. In preparing this article, RHB Bank Berhad has relied upon and assumed the accuracy and completeness of all information available from public references and articles or which was otherwise reviewed by RHB Bank Berhad. Accordingly, whilst we have taken all reasonable care to ensure that the information contained in this article is not untrue or misleading at the time of publication, we cannot guarantee its accuracy or completeness or fairness of such opinions and make no representation or warranty (whether expressed or implied) and accept no responsibility or liability for its accuracy or completeness. You should not act on the information contained in this article without first independently verifying its contents.

Any opinion, historical account, personal profile, estimate or data contained in this article is based on information available as of the date of this article and are subject to change without notice. It does not constitute any advice, offer or solicitation by RHB Bank Berhad. This document and its contents are not intended to constitute an offer for sale and/or invitation to subscribe for or purchase or otherwise acquire any of the instruments referred to herein.

Disclaimer for Video and Podcast by RHB Asset Management:The podcast provided herein is solely for information purposes only. It does not take into account the specific investment objectives, financial situations or particular needs of any particular person.

This podcast does not constitute an offer, solicitation or recommendation to buy or sell or subscribe for any security or financial instrument or to enter into any transaction or to participate in any particular trading or investment strategy. Information contained in the podcast should not be relied upon when making investment decisions. You should seek independent legal or tax advice before making any investment decisions. Investments are subject to investment risks, including the possible loss of the principal amount invested. Value of the investments and the income, if any, may fall or rise.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein and it should not be relied upon as such. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance.

Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same. RHBAM does not guarantee that all risks associated to the transactions mentioned herein have been identified, nor does it provide advice as to whether you should enter into any such transaction. The contents hereof may not be reproduced or disseminated in whole or in part without RHBAM’s written consent.

This podcast has not been reviewed by the Securities Commission Malaysia. You should not act on the information contained in this podcast without first independently verifying its contents.

Disclaimer for Video and Podcast by Economics and Market Strategy:This report is prepared for information purposes only by the Economics and Market Strategy division within RHB Bank Berhad and/or its subsidiaries related companies and affiliates, as applicable (“RHB”). All research is based on material compiled from data considered to be reliable at the time of writing, but RHB does not make any representation or warranty, express or implied, as to its accuracy, completeness or correctness.

Neither this report, nor any opinion expressed herein, should be construed as an offer to sell or a solicitation of an offer to acquire any securities or financial instruments mentioned herein. RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for any direct or consequential loss arising from the use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without prior consent of RHB and RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for the actions of third parties in this respect. Recipients are reminded that the financial circumstances surrounding any company or any market covered in the reports may change since the time of their publication. The contents of this report are also subject to change without any notification.

This report does not purport to be comprehensive or to contain all the information that a prospective investor may need in order to make an investment decision. The recipient of this report is making its own independent assessment and decisions regarding any securities or financial instruments referenced herein. Any investment discussed or recommended in this report may be unsuitable for an investor depending on the investor’s specific investment objectives and financial position. The material in this report is general information intended for recipients who understand the risks of investing in financial instruments. This report does not take into account whether an investment or course of action and any associated risks are suitable for the recipient. Any recommendations contained in this report must therefore not be relied upon as investment advice based on the recipient's personal circumstances. Investors should make their own independent evaluation of the information contained herein, consider their own investment objective, financial situation and particular needs and seek their own financial, business, legal, tax and other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report.

RHB (including its respective directors, associates, connected parties and/or employees) may own or have positions in securities or financial instruments of the company(ies) covered in this research report or any securities or financial instruments related thereto, and may from time to time add to, or dispose off, or may be materially interested in any such securities or financial instruments. Further, RHB does and seeks to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities or financial instruments of such company(ies), may sell them or buy them from customers on a principal basis and may also perform or seek to perform significant banking, advisory or underwriting services for or relating to such company(ies), as well as solicit such banking, advisory or other services from any entity mentioned in this research report.

RHB (including its respective directors, associates, connected parties and/or employees) do not accept any liability, be it directly, indirectly or consequential losses, loss of profits or damages that may arise from any reliance based on this report or further communication given in relation to this report, including where such losses, loss of profits or damages are alleged to have arisen due to the contents of such report or communication being perceived as defamatory in nature.

This podcast has not been reviewed by the Securities Commission (SC) and/or Bank Negara Malaysia (BNM).

RHB Bank Berhad 196501000373 (6171-M)