FAQ ini dikemaskini pada 22 November 2020

Program Bantuan Bayaran Bersasar (“TPA”) merupakan suatu usaha industri perbankan untuk menyediakan bantuan kewangan kepada pelanggan yang tersenarai sebagai penerima pakej Bantuan Sara Hidup (“BSH”) atau Bantuan Prihatin Rakyat (“BPR”).

A customer will be eligible for the TPA Programme if they meet the following requirements:

- Customers must have existing Loan / Financing facilities (except for Credit Card and/or overdraft accounts) with the Bank;

- Customers are recipients of the Bantuan Sara Hidup (“BSH”) / Bantuan Prihatin Rakyat (“BPR”) packages;

- Loan / Financing facilities must not be in arrears exceeding 90 days as at 1 December 2020; and

- Loan / Financing facilities have been approved before 1 October 2020

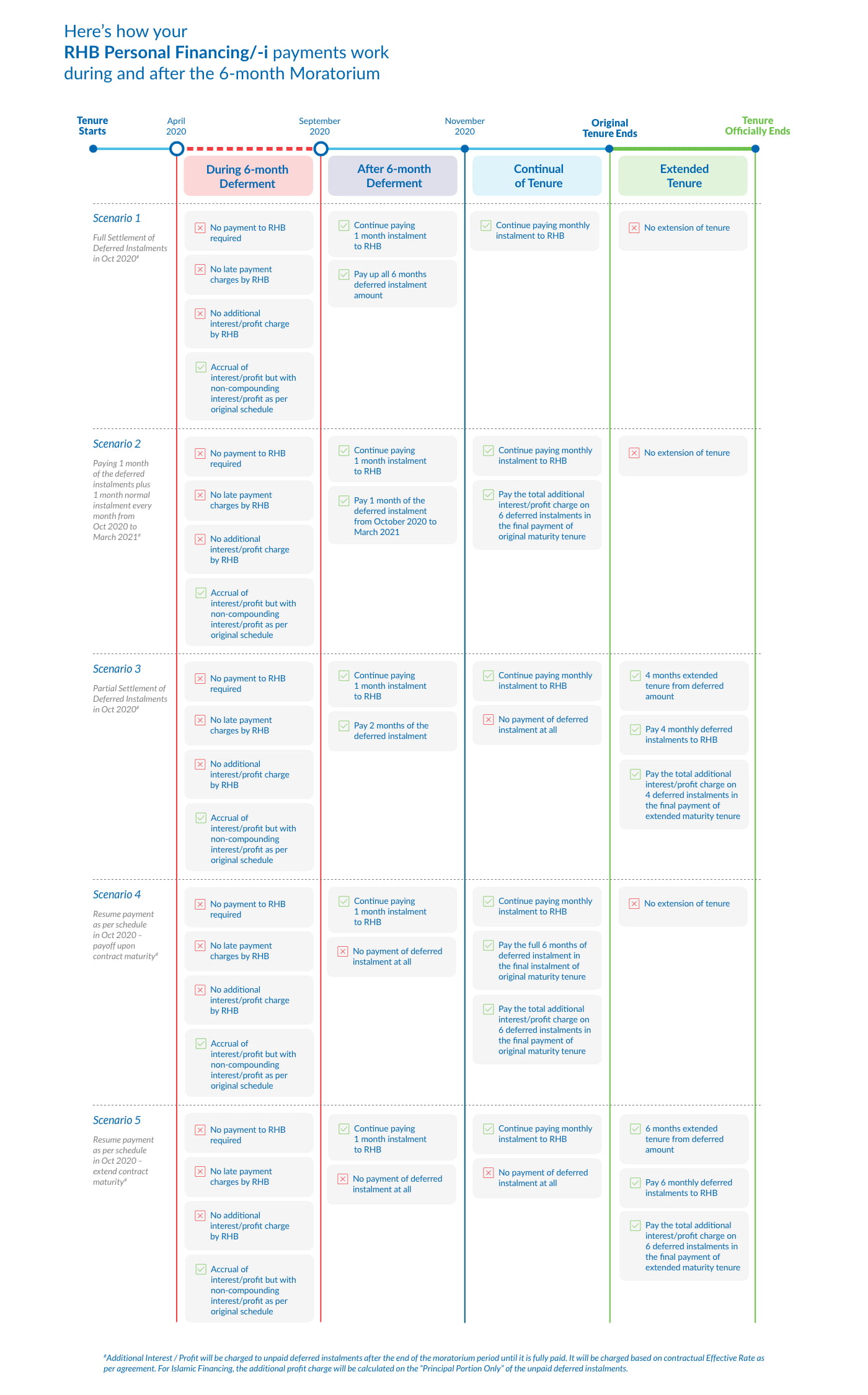

The TPA Programme will cover all Mortgage Financing, Personal Financing/-i, Hire Purchase Financing/-i and ASB Financing products.

There are 2 options available to customers under the TPA Programme. Customers may select from one of these options:

- Option 1: To defer monthly instalments for 3 months; or

- Option 2: To reduce monthly instalments by 50% for 6 months*

There are a few simple ways to apply, depending on the TPA Programme option that you choose:

If you choose Option 1 – to defer your monthly instalments for 3 months:

-

SMS:

We will be sending to you an SMS on the TPA Programme. Upon receiving the SMS from RHB, you may respond to the SMS by simply replying ‘RHBYES’.

Note: If you have recently changed your mobile number, please contact the nearest RHB Bank/ RHB Islamic Branch to update our records as soon as possible. -

e-Form

You may apply for the TPA Programme by completing our e-Form by clicking here. - Account name (e.g. Mortgage, Auto Financing, ASB Financing, etc.)

- IC number

- Account number

or

If you choose Option 2 to reduce your monthly instalments by 50% for 6 months:

To apply for the monthly instalment reduction option under the TPA Programme, please submit your request via e-mail to wecare@rhbgroup.com and include the following details:

No supporting documentation is required in applying for the TPA Programme.

However, for customers with Auto Financing facilities, you will be notified on the pre-approval of your TPA application and you would have to sign a Letter of Variation before a final approval is given by the Bank. Please contact or visit our nearest RHB Auto Finance Sales Office (for Auto Financing) to complete the required agreement upon being advised to do so.

-

Responding to our SMS on the TPA Programme

An SMS will be sent to RHB customers registered under the Bantuan Sara Hidup (“BSH”) or Bantuan Prihatin Rakyat (“BPR”) packages before 25 November 2020. Customers who wish to enjoy the TPA Programme in the month of December 2020 must ensure that you respond “RHBYES” to our SMS before 25 November 2020. Your applications will be attended to within 24 hours.

If you do not receive our SMS by 23 November 2020 and wish to submit your TPA application, please refer to the “Other application methods” option below.

Note: If you have recently changed your mobile number, please contact the nearest RHB Bank / RHB Islamic Bank Branch to update our records as soon as possible.

-

Other application methods

TPA applications may also be submitted by using this e-form or e-mail at wecare@rhbgroup.com. Our branches can also assist with your application. All applications for the TPA Programme received through e-form or email and through our branches will only be processed after 23 November 2020, and a 2-working day turnaround time will apply.

Please visit www.rhbgroup.com for a list of Branches and Sales Offices near you.

We will send eligible RHB customers registered under the BSH or BPR an SMS before 25 November 2020 on the TPA Programme. Please respond to the SMS or submit your applications before 25 November 2020 for the TPA Programme to take effect in December 2020. Otherwise, your payment assistance may only be activated in January 2021.

You may still apply for the TPA Programme until 30 June 2021. However, we strongly urge you to submit your application or respond to our SMS within the timeline as stated above, if you wish to enjoy the TPA in December 2020.

If you miss the 25 November timeline, you can submit your TPA application by completing our TPA Programme e-form here.

For applications received after 25 November 2020:

The monthly Cut-off date for TPA applications is 15th of each month.

TPA Programme applications received and approved before 15th of each month will be activated in the next month. (e.g. Applications received and approved before 15th January 2021 – Payment Assistance will start from February 2021)

TPA Applications received and approved on/after 15th of each month will only be activated in the second month following the application being submitted (e.g. Applications received and approved on/after 15th January 2021 – Payment Assistance will start from March 2021)

Eligible customers may only apply for one TPA Programme per loan / financing account.

Yes, you may still apply for the TPA Programme. However, please that note the following:

-

If you are currently enjoying the deferment option under our Loan / Financing Payment

Assistance programme, you would need to apply for TPA Programme one month prior to the end of

your existing

programme.

(e.g. If your Loan / Financing Payment Assistance ends in January 2021, you can apply for the TPA Programme in December 2020) - If you are currently enrolled in any other payment assistance programmes, your future instalment amounts may be increased if we are unable to extend your Loan / Financing tenor further.

- If you have previously been enrolled in the Loan / Financing moratorium, you are also eligible for the TPA Programme.

If you require any assistance, please refer to Question 23 for our contact details.

We will automatically suspend the Standing Instruction from your TPA Programme commencement date and throughout the payment assistance period.

Upon approval of your TPA Programme application, please cancel future dated transactions for the same loan / financing facilities (beginning the month that your TPA Programme becomes effective) by logging in to RHB Now Internet Banking portal and select either one of the following:

| Steps | BillPay | IBG | Instant Transfer |

|---|---|---|---|

| STEP 1 | Go To BillPay | Go to Fund Transfer | Go to Fund Transfer |

| STEP 2 | Select Other Biller | Select Other Bank Normal Transfer (IBG) | Select Instant Transfer |

| STEP 3 | Select Manage Future Payment | Select Manage Future Transfer | Select Manage Future Transfer |

| STEP 4 | Choose Reference Number | Choose Reference Number | Choose Reference Number |

| STEP 5 | Select Delete Next/ All | Select Delete Next/ All | Select Delete Next/ All |

| STEP 6 | Submit > Successful | Submit > Successful | Submit > Successful |

Please arrange to stop your Standing Instruction (beginning the month that your TPA Programme becomes effective) with your respective bank(s) once you have received approval on your TPA Programme application.

We recommend that you speak to your Employer’s respective Human Resources team to stop your monthly payments once you have received approval on your TPA Programme application.

Note: For customers from the Personal Financing-i Civil Sector, please submit your request by the 5th of the month in order for us to instruct your employer via AG / ANGKASA to stop the salary deduction in the following month.

If your salary has been deducted by your employer, please inform us so that we may process the refund to your Savings / Current Account accordingly.

If you are currently paying monthly instalments to AKPK, please reach out to them for assistance. However, if you are paying monthly instalments directly to the Bank, you are eligible for the TPA Programme as long as your loan / financing facility is not in arrears exceeding 90 days as at 1 December 2020.

No. Interest / profit arising from the deferred payments will not be compounded during the payment assistance period. However, the interest / profit will still be accrued accordingly.

Your account status as at 1 December 2020 will remain unchanged throughout the deferment period.

In this case, your CCRIS report will continue to show 2 months in arrears until the end of the payment assistance period, unless the amount in arrears is paid off in full during this time.

No. Under the TPA Programme, the deferment / reduction will not adversely affect your CCRIS records and it will have no impact on new loan / financing facilities later on.

You can discuss with us at the end of the TPA Programme on the options available for additional payment assistance solutions.

No. There is no need to inform us if you do not want the TPA Programme. Please continue to pay your instalments as usual.

Yes. Your loan / financing facility maturity date will consequently be extended following the completion of the TPA Programme, subject to meeting the maximum allowable tenor allowed by prevailing guidelines.

You may contact the numbers below:

- Mortgage (Residential & Commercial Property) and ASB Financing: 03-2610 6000

- Personal Financing and Hire Purchase: 03-2776 3111

Ya, anda boleh menarik diri dari Program RA dengan menghantar e-mel kepada kami di wecare@rhbgroup.com atau menghubungi kami untuk menyemak semula terma pembayaran.

Anda boleh menghubungi kami di:

- Gadai janji (Harta Kediaman & Komersial) dan Pinjaman / Pembiayaan ASB: 03-2610 6000

- Pembiayaan Peribadi dan Sewa Beli Kenderaan: 03-2776 3111

- customer.service@rhbgroup.com

Anda juga boleh menghubungi Agensi Kaunseling & Pengurusan Kredit (AKPK) untuk mendapatkan nasihat dalam hal kewangan anda.