For a simple video guide on how to apply for the PEMULIH Repayment / Payment Assistance programme, click here for the video.

This FAQ is updated as at 6 October 2021

The RA Programme is a temporary relief programme that offers repayment / payment assistance to customers who have been affected by COVID-19 pandemic and Movement Control Order (MCO).

The Programme is available from 7 July 2021 until such time as movement control restrictions remain in place.

Options available to customers under the RA Programme are as follows. Kindly select and submit the required RA Programme stated below through the e-Form.

- Option 1: Six (6) months deferment of instalments / moratorium (Applicable to all products); or

- Option 2: 50% reduction of instalments for six (6) months; or

- Option 3: Customised reduction in monthly instalment by extension of loan / financing tenure

(Note: Option 2 and Option 3 are not applicable to accounts under progressive release, or with advance payment, or overdraft facility.)

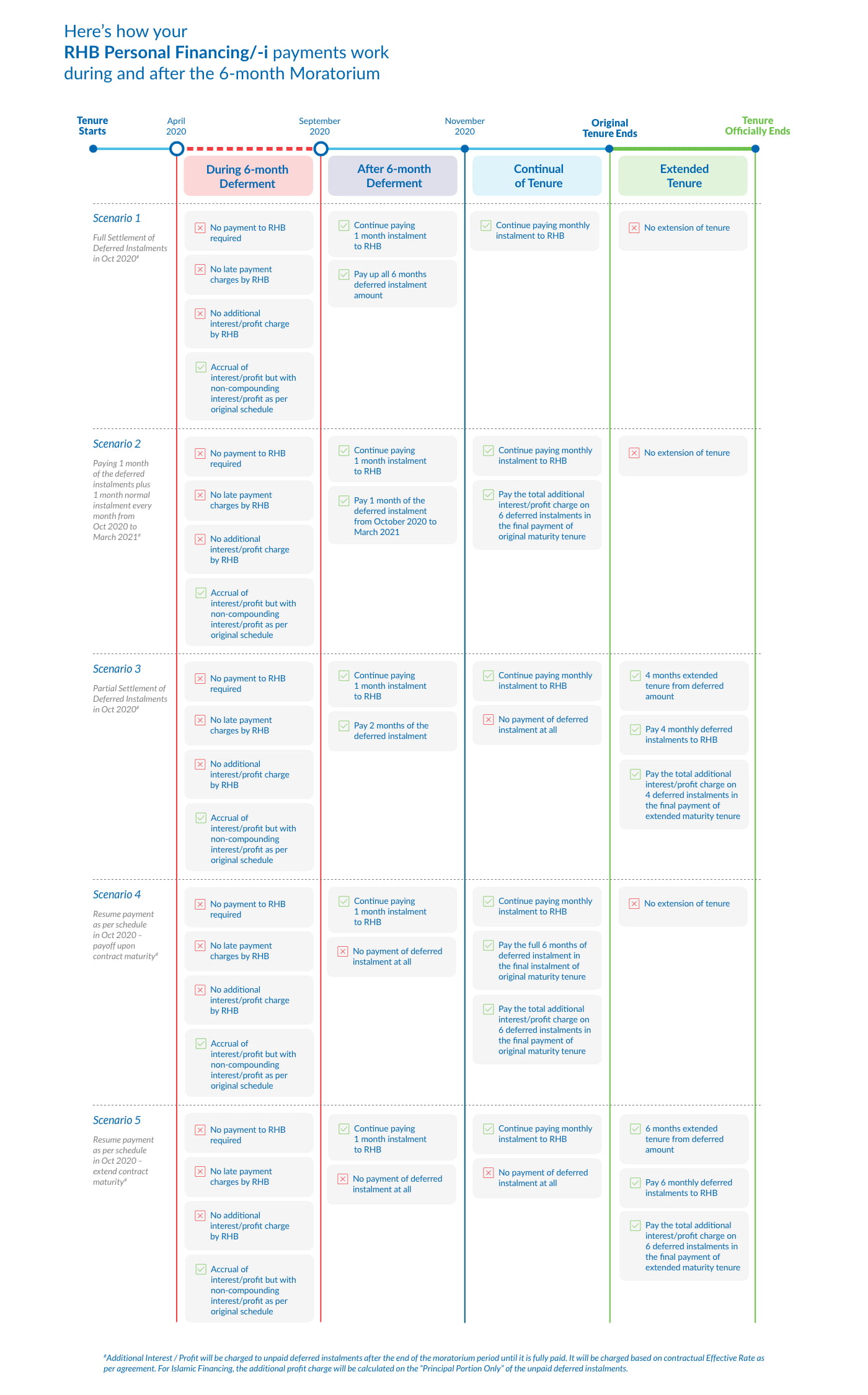

Please refer to Question 24 of this FAQ for relevant illustrations.

Normal interest / profit will continue to be charged and accrued during the deferment / moratorium period. This may result in your loan/financing tenure being extended and an increase in total repayment / payment amount.

Extension of tenure for your loan/financing facility will reduce your monthly installment. However, total repayment / payment amount will increase depending on the tenure extension.

In addition to the above, please take note of the following:

- Approvals for RA Programme applications are subject to RHB Bank’s policy on the RA Programme.

- The Bank may cancel and re-negotiate the RA Programme initially granted in the event that the Bank finds that you have provided false or misleading information in your application.

- For customers who are currently under a 3 months’ deferment of instalments / moratorium that is still ongoing in July 2021, an additional 3 months’ deferment of instalments / moratorium will be granted upon expiry of your current repayment / payment facility. Hence, the deferment of instalments / moratorium period will be 6 months in total (Example: If your existing 3 months’ deferment ends in August 2021, then an additional 3 months’ deferment of instalments / moratorium will be granted providing you with 6 months’ deferment in total).

The RA Programme is available for all individuals (including B40, M40, and T20) who require repayment / payment assistance. However, this excludes:

- Loan / Financing in arrears exceeding 90 days

- Loan / Financing approved on/after 1 July 2021

- Individuals under a bankruptcy charge

You will receive an SMS/call to inform you on the status of your application together with further instructions within five (5) calendar days after we receive your application. If you have recently changed your handphone number, please visit your nearest branch to update your records. We also recommend that you download the QMS application (from Play Store for Android or App Store for iPhone) to make an appointment to reduce waiting time at the branch.

If your application is approved, a Letter of Notification or Letter of Variation will thereafter be e-mailed to you within one (1) week from approval indicating your new payment terms:

- If you receive a Letter of Notification (for deferment of instalments / moratorium), no further action is required.

- If you receive a Letter of Variation (for reduction in monthly instalment by extension of loan / financing tenure), you are required to follow the instructions provided therein. If we don’t receive a response from you within five (5) calendar days from the date stated within the Letter of Variation, your application will be deemed as cancelled.

For customers with Hire Purchase/-i facility

- For the deferment of instalments / moratorium, you will receive an SMS within five (5) calendar days and no further action is required.

- Details of your new instalment terms will be sent to you via a Moratorium Notice within the moratorium period. This includes information on Cost of Moratorium, (for Hire Purchase facility) and Moratorium Ijarah Rental (for Hire Purchase Islamic facility) on the deferred instalment amount, which is a one-off amount that will be debited to your Hire Purchase/-i account after the end of the moratorium period.

- For Reduction in Instalment Repayment / Payment, you will receive an SMS and email within five (5) calendar days with revised Letter of Offer and Variation Agreement for customer(s)’ acceptance. The revised term can only be effected after the customer accepts the offer.

For applications made in July 2021, the assistance will be effective in the same month, i.e. from July 2021 instalment onwards.

For applications made after July 2021, RA Programme applications received, approved and accepted in

that month will be activated in the next month.

(For example - For applications received,

approved and accepted in August 2021, Repayment / Payment Assistance will start from September

2021.)

Please take note that:

If you have already made instalment payment for the month of July 2021, this amount will be treated

as an advance payment for the month after your repayment/payment assistance ends. Notwithstanding,

you are still entitled to a total of 6 months of moratorium. Under such circumstances, you will not

need to make any instalment payment until the end of January 2022.

However, you may contact the Bank should you require the amount to be reimbursed if your payment was made via transfer from an RHB Current or Savings account. The Bank will make the necessary arrangement for refund within a period of one month. However, we will not be able to process refund requests if payment was made from another bank, payment via cash, or cheque, or other methods where the Bank will not be able to ascertain the origin of payment.

Please forward your request to our channels below:

- Mortgage (Residential & Commercial Property) and ASB Loan / Financing: 03-2610 6000

- Personal Financing and Hire Purchase: 03-2776 3111

- customer.service@rhbgroup.com

The SMS you had received is still valid. If you have not responded to the SMS, and would like to apply for PEMULIH RA, you may apply by replying “MORAYES” to 66300.

Your acceptance is deemed to have been received for PEMULIH RA. No further action is required.

Kindly submit a new e-Form application as replacement.

This situation may occur if your application did not meet the eligibility criteria as per Question 2 of the FAQ. However, you may submit an appeal with additional justification / supporting documents.

Alternatively, you can seek assistance from Agensi Kaunseling dan Pengurusan Kredit (AKPK), an agency which provides advisory services and assistance to individual borrowers / customers in managing their finances.

If you require any assistance, please refer to Question 26 of this FAQ for our contact details.

Yes, you can but you will only be eligible for the balance of the total of 6 months’ assistance available to you under the PEMULIH RA Programme. Please refer to Question 1 for further explanation.

Please submit your application via e-Form and your new RA will take effect following the expiry of the existing RA Programme.

For example:

- Current RA Programme expiry date: 5 July 2021

- New RA Programme for 6-month moratorium will take effect from August 2021. However, please take note that for customers who are currently under a 3 months’ deferment of instalments / moratorium effective from June – August 2021, an additional 3 months’ deferment of instalments / moratorium will be granted upon expiry of your current repayment / payment facility. Hence, the deferment of instalments / moratorium period will be 6 months in total.

We will automatically suspend the Standing Instruction from your RA Programme commencement date and throughout the repayment / payment assistance period.

Upon approval of your RA Programme application, please cancel future dated transactions for the same loan / financing facilities (beginning the month that your RA Programme becomes effective) by logging in to RHB Now Internet Banking portal and select either one of the following:

| Steps | BillPay | IBG | Instant Transfer |

|---|---|---|---|

| STEP 1 | Go To BillPay | Go to Fund Transfer | Go to Fund Transfer |

| STEP 2 | Select Other Biller | Select Other Bank Normal Transfer (IBG) | Select Instant Transfer |

| STEP 3 | Select Manage Future Payment | Select Manage Future Transfer | Select Manage Future Transfer |

| STEP 4 | Choose Reference Number | Choose Reference Number | Choose Reference Number |

| STEP 5 | Select Delete Next/ All | Select Delete Next/ All | Select Delete Next/ All |

| STEP 6 | Submit > Successful | Submit > Successful | Submit > Successful |

Please arrange to stop your Standing Instruction (beginning the month that your RA Programme becomes effective) with your respective bank(s) once you have received approval on your RA Programme application.

If you are currently paying monthly instalments to AKPK, please reach out to them for assistance. However, if you are paying monthly instalments directly to the Bank, you are eligible for the RA Programme as long as your loan / financing facility is not in arrears exceeding 90 days.

No. Interest / profit arising from the deferred repayment / payments will not be compounded during or following the repayment / payment assistance period. This means that the interest / profit incurred during this period does not get larger over time.

However, the interest / profit will still be accrued accordingly. This means that interest / profit will continue to be charged daily or monthly. However, this will be based on your outstanding amount before the repayment / payment assistance programme period.

No, it will not. Rest assured that your interest / profit rate will not be increased under the RA Programme. Although there will be adjustments in the instalment amount should there be any revisions to the Base Rate / Base Rate Islamic / Base Lending Rate / Base Financing Rate.

Note:

Please be advised that our Base Rate (BR) / Base Rate Islamic (BFI) & Base Lending Rate (BLR) / Base Financing Rate (BFR) are 2.5% & 5.45% respectively effective 13th July 2020.

No, you will not be able to request for lower interest / profit rate through the RA programme.

Your account status will remain unchanged throughout the deferment period.

In this case, if your payment is 2 months in arrears before the RA Programme, your CCRIS report will continue to show 2 months in arrears until the end of the repayment / payment assistance period, unless the amount in arrears is paid off in full during this time.

No. Under the RA Programme, the deferment of instalments / moratorium / reduction will not adversely affect your CCRIS records and it will have no impact on new loan / financing facilities later on.

If your existing loan / financing is already under the Debt Management Programme by Agensi Kaunseling & Pengurusan Kredit (AKPK), your current CCRIS status will remain unchanged.

If following the approval of your RA Programme application, you discover that you are unable to pay the new instalment amount, please follow instructions stated in the Letter of Variation to enable us to reconsider your instalment amount.

There will be no additional fees imposed for the RA Programme except for Hire Purchase/-i facilities involving extension of tenure.

For Hire Purchase/-i, in accepting RA Programme offer, customers are required to sign a Hire Purchase Variation Agreement (Conventional), or a Hire Purchase/-i Variation Agreement (Islamic) and Supplementary Guarantee Agreement (facility with guarantor). Customers would only need to pay for the stamping and postage of these documents. The fees for stamping are detailed below:

-

Facility WITHOUT Guarantor:

- Stamp duty for Hirer - RM10

- Postage for Hirer – RM7.30

-

Facility WITH Guarantor:

- Stamp duty for Hirer & Guarantor – RM20

- Postage for Hirer & Guarantor – RM13.40

You can discuss with us at the end of the RA period on the options available for additional repayment / payment assistance solutions.

Yes. Your loan / financing facility maturity date will consequently be extended following the end of the deferment of instalments / moratorium period, subject to meeting the maximum allowable tenure allowed by prevailing guidelines. Please refer to Question 24 for more information.

The Insurance / Takaful coverage will remain unchanged up to the original loan / financing tenure. The time period where the loan / financing tenure is extended will not be covered by your original insurance / Takaful plan.

To extend your Insurance / Takaful coverage, please contact your appointed Insurer / Takaful company for further assistance.

For Conventional Life Insurance Policy under Tokio Marine Life Insurance Malaysia Bhd:

Please email to customercare@tokiomarinelife.com.my

Or contact their Customer Care Hotline at 03 – 2603 3999 (Monday - Thursday 8:40am - 5:30pm; Friday 8:40am - 5:20pm)

For Hire Purchase/-i Reducing Term Takaful (HPRTT), please email to mybancahelpdesk@takaful- malaysia.com.my

It is important that you are aware the RA Programme will increase your total repayment / payment amount.

Please see below examples of cost implications relating to Mortgage, ASB, Personal Loan / Financing (Fixed Rate) and Hire Purchase.

DEFERMENT OF INSTALMENT / MORATORIUM

-

Mortgage / ASB Loan / Financing

Your loan/financing payment is deferred for 6 months and loan/financing tenure is extended for 6 months. During the deferment of instalments / moratorium period, interest/profit will continue to accrue and this would increase the total repayment / payment amount. However, the interest/profit charged during this deferment of instalments / moratorium period is not compounded.

Your monthly instalment will not increase upon expiry of the deferment of instalments / moratorium period. As monthly instalment remains the same, the outstanding balance will then become due at the end of the loan/financing tenure, in one lump sum. This is provided that there is no change to the Base Rate (BR)/Base Rate Islamic (BRI) or Base Lending Rate (BLR)/Base Financing Rate (BFR) throughout the remaining loan/financing tenure.

This is illustrated below.

Mortgage

Before RA Programme After RA Programme Monthly Instalment Amount RM1,710.00 RM1,710.00 Total Repayment / Payment Amount at The End of Tenure RM410,400.00 RM419,612.00 Increase in Total Repayment / Payment Amount (This results from the deferred monthly instalments and interest/profit accrued during the RA Programme) - RM9,212.00

The table above includes the following assumptions:

- Principal outstanding for the loan/financing is RM300,000 before the RA Program

- Effective interest/profit rate is 3.30% p.a.

- Original Loan/Financing tenure is 25 years; with remaining tenure of 20 years (240 months)

- There is no outstanding Fire Insurance/Takaful in the loan/financing account throughout the remaining loan/financing tenure

- There is no change to the BR/BRI/BLR/BFR throughout the remaining loan/financing tenure

- The total repayment / payment amount will be higher if the RA Program is further extended

ASB Loan / Financing

The table above includes the following assumptions:Before RA Programme After RA Programme Monthly Instalment Amount RM292.00 RM292.00 Total Repayment / Payment Amount at The End of Tenure RM69,824.00 RM73,360.00 Increase in Total Repayment / Payment Amount (This results from the deferred monthly instalments and interest/profit accrued during the RA Programme) - RM3,536.00

- Principal outstanding for the loan/financing is RM50,000 before the RA Program

- Effective interest/profit rate is 3.55% p.a.

- Original loan/financing tenure is 25 years; with remaining tenure of 20 years (240 months)

- There is no change to the BR/BRI/BLR/BFR throughout the remaining loan/financing tenure

- The total repayment / payment amount will be higher if the RA Program is further extended

However, if there is a change in the BR/BRI/BLR/BFR at any time during the remainder of your loan/financing tenure, your monthly instalment amount will be revised upwards to include the principal amount deferred and interest/profit accrued during the RA period, including outstanding Fire Insurance/Takaful fee (if any). You will be notified of any future revision in BR/BRI/BLR/BFR. In this case, there should not be any one lump sum due at the end of the loan/financing tenure provided that you make prompt repayment / payment on your monthly instalments. -

Personal Loan / Financing (Fixed Rate), Hire Purchase-i (Fixed Rate)

During the 6 months MORATORIUM- Your loan/financing payment has been deferred for 6 months and no payment will become due during this 6-month moratorium period.

- There is no compounding interest / profit.

After the 6 months MORATORIUM- Your Loan / Financing facility tenure will be extended for 6 months, reflective of the moratorium period. Your monthly instalments will continue in month 7 and this amount will remain unchanged.

- Your 6 month deferred instalments will become payable over the remainder of your loan/financing tenure.

- Principal outstanding for the loan/financing is RM50,000 before the RA Program

- Interest/profit rate is 2.50% flat p.a.

- Original loan/financing tenure is 7 years; with remaining tenure of 60 months

- The total repayment / payment amount will be higher if the RA Program is further extended

- Principal outstanding for the loan/financing is RM50,000 before the RA Program

- Interest/profit rate is 2.50% flat p.a.

- Original loan/financing tenure is 5 years; with remaining tenure of 60 months

- The total repayment / payment amount will be higher if the RA Program is further extended

- Total outstanding amount for the overdraft is RM50,000 before the Deferment of Repayment / Moratorium Period

- Interest rate is 5.00% p.a.

- There is no change to the Base Rate (BR) or Base Lending Rate (BLR).

- Overdrafts against Property, Overdrafts against ASB/ASW and Overdrafts against Fixed Deposits – Additional interest of 1% per annum

- Overdrafts for Gold Debit / Cash Connect Xtra – Interest of 24% per annum

Illustration below for Personal Financing Islamic (Fixed Rate)

Before RA Programme After RA Programme Monthly Instalment Amount RM699.40 RM699.40 Total Repayment / Payment Amount at The End of Tenure RM58,750.00 RM59,539.80 Increase in Total Repayment / Payment

(This results from the deferred monthly

instalments and interest/profit accrued during

the RA Programme)- RM789.80 Lump-sum payment on last payment RM699.40 RM1,489.20

The table above includes the following assumptions:

Note: To avoid additional costs charged to the account, you are encouraged to pay down the 6 months deferred payment after the end of 6 months moratorium.

Should you require further assistance following the expiry of your moratorium period, your monthly instalment may be further reduced by extending your loan / financing facility tenure through a variation of contract (with acceptance of new Aqad for Islamic Contract). During your 6-month moratorium, we will reach out to you with more details.

Illustration below for Hire Purchase (Conventional)

Before RA Programme After RA Programme Monthly Instalment Amount RM938 RM938 Total Repayment Amount at the end of Financing Tenure RM56,250 RM57,303.98 Increase in Total Repayment / Payment

(This includes cost of moratorium on the deferred

principal monthly instalments during the 6-month

moratorium period)- RM1,053.98

The table above includes the following assumptions:

Note: Details of your new instalment terms will be sent to you via a Moratorium Notice within the moratorium period. This includes information on Cost of Moratorium (for Hire Purchase facility) and Moratorium Ijarah Rental (for Hire Purchase Islamic facility) on the deferred instalment amount, which is a one-off amount that will be debited to your Hire Purchase/-i account after the end of the moratorium period.

Please contact us at 03-27763111 or e-mail to customer.service@rhbgroup.com for further assistance to reduce your monthly instalment through a variation of contract.

Overdraft Facility

Repayment on your Overdraft Facility is deferred for 6 months. During this deferment of repayment / moratorium period, interest will continue to accrue on your outstanding amount and this would increase the total outstanding amount. However, the interest charged during this deferment of repayment / moratorium period is not compounded.

The unutilised portion of your Overdraft Facility may continue to be used during the deferment of repayment / moratorium period and this will also be included as part of the deferment / moratorium amount. However, the deferment of repayment / moratorium period will remain unchanged and will end upon completion of the original 6 months’ period.

Interest accrued from the outstanding amount at the beginning of the deferment / moratorium period, including any amounts utilised under the Overdraft Facility during that period, will become payable in one lump sum upon expiry of the deferment of repayment / moratorium period.

This is illustrated below.

Overdraft Approved Limit (RM) RM60,000.00 How to derive the financing cost?

Total Outstanding Balance x Effective Interest Rate x

Days of moratorium / Number of days in a yearBefore Deferment of Repayment / Moratorium:

Total Outstanding Amount (RM) as at 30 June 2021

(Note that this is the utilised overdraft amount)RM50,000.00 Interest Rate @ 5.00% p.a RM1,260.73 After Deferment of Repayment / Moratorium RM51,260.73

The table above includes the following assumptions:

It may be possible that your Overdraft Facility Approved Limit is exceeded due to interest accumulation either during or after the deferment of repayment/moratorium period. In such instances, additional interest may be charged on amounts exceeding your Overdraft Facility Approved Limit. This applies to:

50% REDUCTION OF INSTALMENTS FOR SIX (6) MONTHS-

Mortgage / ASB Loan / Financing

Your monthly instalment will be lowered by 50% for 6 months. Upon expiry of the PEMULIH Repayment / Payment Assistance (RA) Programme, your monthly instalment will revert to the original amount and the total repayment amount will increase. As there is no extension of loan/financing tenure and monthly instalment remains the same, the outstanding balance will then become due at the end of the loan/financing tenure, in one lump sum. This is provided that there is no change to the Base Rate (BR)/Base Rate Islamic (BRI) or Base Lending Rate (BLR)/Base Financing Rate (BFR) throughout the remaining loan/financing tenure.

This is illustrated below.

MortgageWithout PEMULIH RA Programme With PEMULIH RA Programme Monthly Instalment Amount RM1,710.00 50% instalment amount: RM855.00

Upon expiry of PEMULIH RA: RM1,710.00Total Repayment / Payment Amount at The End of Tenure RM410,400.00 RM414,822.00 Increase in Total Repayment / Payment Amount - RM4,422.00 The table above includes the following assumptions:

- Principal outstanding for the loan/financing is RM300,000 before the RA Programme

- Effective interest/profit rate is 3.30% p.a.

- Original Loan/Financing tenure is 25 years; with remaining tenure of 20 years (240 months and there is no extension of loan/financing tenure)

- There is no outstanding Fire Insurance/Takaful in the loan/financing account throughout the remaining loan/financing tenure

- There is no change to the BR/BRI/BLR/BFR throughout the remaining loan/financing tenure.

- The total repayment / payment amount will be higher if the RA Programme is further extended.

ASB Loan / FinancingWithout PEMULIH RA Programme With PEMULIH RA Programme Monthly Instalment Amount RM292.00 50% instalment amount: RM146.00

Upon expiry of PEMULIH RA: RM292.00Total Repayment / Payment Amount at The End of Tenure RM69,824.00 RM70,709.00 Increase in Total Repayment / Payment Amount - RM885.00 The table above includes the following assumptions:

- Principal outstanding for the loan/financing is RM50,000 before the RA Program

- Effective interest/profit rate is 3.55% p.a.

- Original loan/financing tenure is 25 years; with remaining tenure of 20 years (240 months and there is no extension of loan/financing tenure)

- There is no change to the BR/BRI/BLR/BFR throughout the remaining loan/financing tenure.

- The total repayment / payment amount will be higher if the RA Programme is further extended.

However, if there is a change in the BR/BRI/BLR/BFR at any time during the remainder of your loan tenure, your monthly instalment amount will be revised to include the principal amount deferred and interest accrued (if any) during the RA period, including outstanding Fire Insurance fee (if any). You will be notified of any future revision in BR/BRI/BLR/BFR. In this case, there should not be any one lump sum due at the end of the loan tenure provided that you make prompt payment on your monthly instalments.

-

REDUCTION IN INSTALMENT REPAYMENTS / PAYMENTS

While this will lower your monthly instalment amount, the tenure of your credit facility is also extended and your total repayment / payment amount will increase as interest/profit will continue to accrue throughout the longer loan/financing tenure. See example below:

Please see below examples relating to Mortgage, ASB, Personal Loan / Financing (Fixed Rate) and Hire Purchase.

Mortgage

Original Terms Tenure Extension +12 Months +36 Months +60 Months Remaining Loan/ Financing Tenure (Month) 120 132 156 180 Monthly Installment Amount RM2,938.55 RM2,713.22 RM2,367.58 RM2,115.30 Total Repayment/Payment Amount at The End of Tenure (Remaining Loan/Financing Tenure x Monthly Instalment Amount) RM352,626.17 RM358,144.83 RM369,343.03 RM380,754.76 Increase in Total Repayment/Payment Amount (Revised Terms' Total Repayment/Payment Amount at The End of Tenure - Original Terms' Total Repayment/payment Amount at The End of Tenure) - RM5,518.67 RM16,716.86 RM28,128.59

The table above includes the following assumptions:- The monthly instalment has been revised and the loan/financing tenure is extended

- Principal outstanding for the loan/financing is RM300,000

- Effective interest/profit rate is 3.30% p.a.

- Original loan/financing tenure is 25 years; with remaining tenure of 10 years (120 months)

- There is no outstanding Fire Insurance/Takaful in the loan/financing account throughout the remaining loan/financing tenure

- There is no change to the BR/BRI/BLR/BFR throughout the remaining loan/financing tenure

-

ASB Loan / Financing

Original Terms Tenure Extension +12 Months +36 Months +60 Months Remaining Loan/Financing Tenure (Month) 120 132 156 180 Monthly Installment Amount RM496.00 RM459.00 RM401.00 RM359.00 Total Repayment/Payment Amount at The End of Tenure (Remaining Loan/Financing Tenure x Monthly Instalment Amount) RM59,520.00 RM60,588.00 RM62,556.00 RM64,620.00 Increase in Total Repayment/Payment Amount (Revised Terms' Total Repayment/Payment Amount at The End of Tenure - Original Terms' Total Repayment/payment Amount at The End of Tenure) - RM1,068.00 RM3,036.00 RM5,100.00

The table above includes the following assumptions:- The monthly instalment has been revised and the loan/financing tenure is extended

- Principal outstanding for the loan/financing is RM50,000

- Effective interest/profit rate is 3.55% p.a.

- Original loan/financing tenure is 25 years; with remaining tenure of 10 years (120 months)

- There is no change to the BR/BRI/BLR/BFR throughout the remaining loan/financing tenure

-

Personal Loan / Financing (Fixed Rate)

Your loan /financing facility has been extended for 24/36 months. While your monthly instalments will reduce, the Total Payment/Repayment Amount will increase.

Original Terms Tenure Extension +24 Months +36 Months Remaining Loan / Financing Tenure (Month) 84 108 120 Monthly Installment Amount RM1,608.00 RM711.58 RM617.68 Total Payment / Repayment Amount at The End of Tenure (Remaining Loan / Financing Tenure x Monthly Instalment Amount) RM135,000.00 RM139,174.60 RM140,953.54 Increase in Total Payment / Repayment Amount (Revised Terms' Total Payment / Repayment Amount at The End of Tenure - Original Terms' Total Payment / Repayment Amount at The End of Tenure) - RM4,174.60 RM5,953.54

The table above includes the following assumptions:- The monthly instalment has been revised and the financing tenure is extended

- Principal outstanding for the financing is RM100,000

- Effective profit rate is 5.00% p.a.

- Original Loan / Financing tenure is 7 years; with remaining tenure of 5 years (60 months)

Yes, you can opt out from RA Programme at any time by emailing to wecare@rhbgroup.com or visit/call us to revisit the repayment/payment term.

You may reach us at:

- Mortgage (Residential & Commercial Property) and ASB Loan / Financing: 03-2610 6000

- Personal Financing and Hire Purchase: 03-2776 3111

- customer.service@rhbgroup.com

You may also reach out Agensi Kaunseling & Pengurusan Kredit (AKPK) for assistance on your financial matters.