Quarterly Market Outlook

An unwelcome visitor in early 2020 — Covid-19 — took investors by surprise. The deadliness of the virus was not known until the World Health Organization declared the outbreak as a pandemic in early March. By then, the virus had spread all over the world and the number of new cases had spiked, prompting governments throughout the world to implement unprecedented measures. Borders and economies were closed to prevent the virus from spreading faster while scientists worldwide raced to find a vaccine.

The Malaysian government prioritised people’s health over the economy as global and domestic Covid-19 infections and deaths increased. It introduced the Movement Control Order (MCO) from March 18, followed by the Conditional MCO and then Recovery MCO.

The strict lockdown and border closures have adversely affected the economy. GDP in the second quarter of 2020 shrank sharply and was worse than during both the Asian and global financial crises (AFC and GFC). Malaysia recorded the worst quarterly GDP numbers in 2Q2020, plunging 17.1% year on year. It was also the most badly affected economy in Southeast Asia.

The government unveiled RM250 billion in economic stimulus, or 17% of GDP, in the first quarter of 2020. As the number of new Covid-19 cases increased sharply in recent weeks, the government announced an extension of the previous economic stimulus packages on Sept 23, bringing the total value of economic stimulus to an estimated RM295 billion, or 20% of GDP, with direct fiscal injection estimated at RM45 billion, or 3% of GDP, to counter the uncertainty surrounding domestic and global economic recovery.

Bank Negara Malaysia has also been cutting interest rates since the beginning of the year, from 3% to 1.75% to boost the economy.

The aggressive interest rate cut has resulted in a drop in 10-year government bond yields to a historical low of 2.39%, which is even lower than during the GFC’s 2.97%. In addition, Bank Negara had introduced a six-month automatic loan moratorium from April 1 to Sept 30. The waiver of debt service obligations is estimated at RM100 billion over the six-month automatic loan moratorium.

This has resulted in a liquidity surge in the local stock market as retail players search for better-yielding assets. Local retail participation has increased significantly in 2020. Apart from the liquidity, Bursa Malaysia’s ban of short selling on stocks also contributed to the positive market sentiment and the ban will continue until year-end.

Bursa Malaysia’s turnover velocity and average value and volume traded increased significantly in the first half of 2020 (1H2020). This was due to higher participation from retail investors seeking higher returns, as fixed deposits returns have dropped substantially and investors also have more money in their pockets.

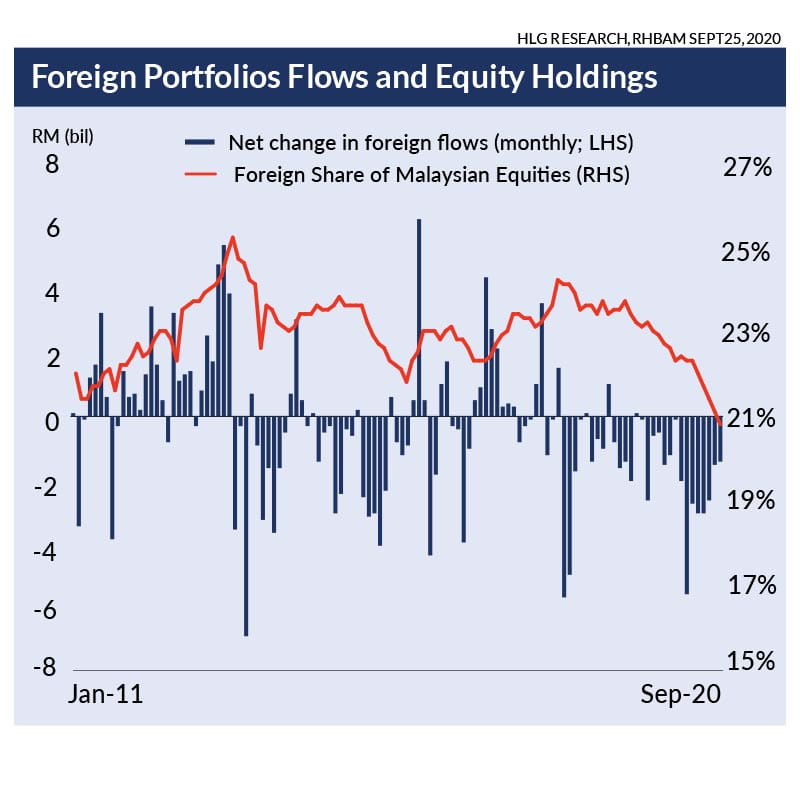

Retail participation has increased from an average of 24% from 2010 to 2019, to 33% in 1H2020, while institutional participation decreased to 67%, from an average of 76% over the past 10 years. Whilst, foreign participation has decreased further to 21% in 1H2020 compared with the average of 29% over the past 10 years.

Foreign portfolio managers have been selling Malaysian equity, owing to a less attractive earnings outlook for Malaysian corporates. Year-to-date (YTD) foreign outflows in equity are RM21.7 billion.

Foreign shareholding of Malaysia equities also fell substantially from above 24% in February 2018 to 20.8% in August 2020. This level is near the 20.7% level touched during the GFC.

The index has been trending down since touching its high of 1,611.42 on July 29. As at Sept 30, the index is down 6.6% on concerns over a selloff by retail investors, owing to the end of the six-month automatic loan moratorium on Sept 30; the escalation of tensions between the US and China as the Trump administration continues to add to the number of blacklisted sectors and companies; and fear of the delay in the recovery of the economy globally, owing to a recent spike in the number of Covid-19 cases globally.

Glove manufacturers, which have contributed significantly to the increase in the index since March, were under selling pressure from July 29, owing to the news that a Covid-19 vaccine may be made available to the public by year-end. We believe, however, that the pandemic has structurally changed the demand dynamic for gloves. They are now used by every sector in the economy globally and not only in the medical sector.

Mohd Fauzi Mohd Tahir, chief investment officer, equity Malaysia, at RHB Asset Management, says: “Despite the potential discovery of a Covid-19 vaccine by end-2020, we believe the availability is likely to be scarce. The vaccines will be made available to healthcare professionals and essential workers first, and it will take time before the vaccines will be made available to the wider general public. Thus, glove usage globally is likely to remain strong in both the medical and non-medical sectors. As the current lead times for normal glove orders have stretched to more than 18 months (into 2022), the favourable supply-demand dynamic will be able to sustain elevated glove prices. As Malaysia is a leading global exporter of gloves, growth in the export of our rubber products will continue to be strong.”

The Malaysian Rubber Glove Manufacturers Association (MARGMA) believes it will take several years for the industry to fill the current demand, which is expected to expand at least 20% to 25% post-Covid-19 compared with 8% to 10% annual growth before Covid-19.

The measures introduced by Bank Negara will soon come to an end, and it is expected that selling pressure from retail investors will come after the end of the loan moratorium, although retail participation was at 38% in September, as 70% of household loans are on variable interest rates. While domestic demand has gradually rebounded, with the reopening of the economy, unemployment numbers are still high, which means it will be difficult for people to service their household debt. As economic recovery is still sluggish, the lifting of the loan moratorium at end-September has an impact on not only stock market liquidity but will also affect domestic demand.

Therefore, will liquidity dry up and will the index be pushed lower, from current levels, or could the index merely undergo a consolidation period before it rises further?

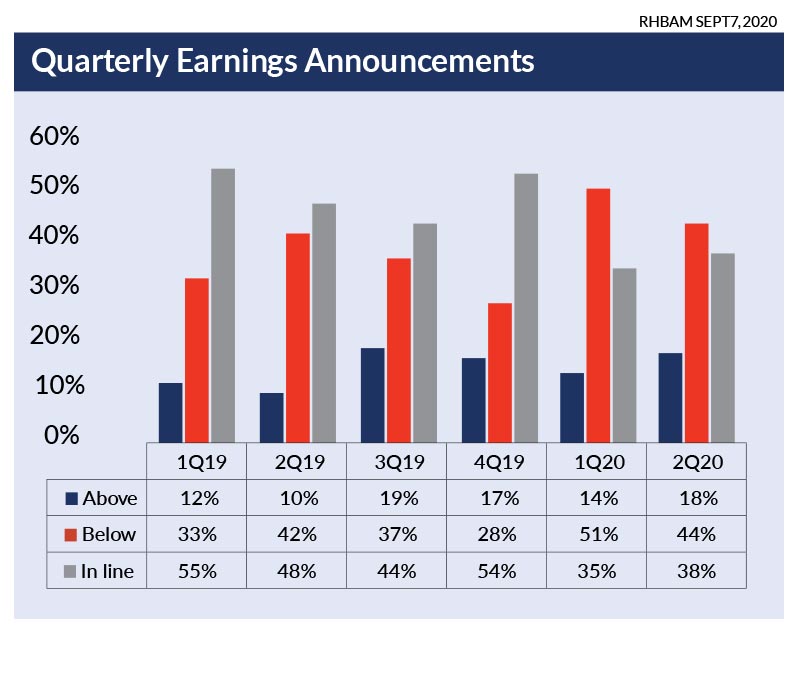

Since it is difficult to assess the amount of liquidity push in the stock market, we believe corporate earnings are key to the sustainable rise in the FBM KLCI. Moreover, we noticed that the companies which had done well in terms of price performance as index corrected are companies which delivered better earnings in the 2Q20.

Based on our coverage, the recent 2Q2020 results were better than 1Q2020 results even though GDP fell 17.1% y-o-y. More companies are now reporting profits that exceed equity market expectations.

If history repeats itself, we would see corporate earnings start to rebound from 3Q2020 but at a slower pace than the previous recession, owing to the partial lockdown in 2020.

RHB Asset Management believes corporate earnings will be stronger in 2021, owing to an improving economy as more countries reopen borders and economies and vaccines are expected to be found.

Thus, we expect that selling pressure, which may come from retail investors, may be able to be absorbed by local and foreign institutions if corporate earnings improve further. The positive point is that net foreign selling has been shrinking since July.

In conclusion, the FBM KLCI is expected to consolidate in the short term, pending 3Q2020 corporate results announcements from end-October, the extent of the absence of liquidity in the local stock market after the end of the six-month automatic loan moratorium, as well as US and China tensions, which may be prolonged until the conclusion of the US presidential election in November. Investors are also waiting for the results of the election, as it will have an impact on the country’s foreign policies.

Mohd Fauzi says: “The announcement by FTSE Russell not to remove Malaysia from the World Government Bond Index is positive in the short term, but it is still uncertain whether it will remove Malaysia in March 2021. We believe equity will remain the preferred asset class, owing to the improving economies and current low interest rate environment.”

Volatility is likely to persist, as the market will be driven by news flow, with a focus on the number of Covid-19 cases and progress on the development of the vaccines. We believe that cyclical sectors are likely to perform better as the economy improves. Even though a vaccine could be ready by 1H2020, the general population will probably be vaccinated only by end-2021, thus a negative impact on the tourism and hospitality industry is likely to be prolonged. We still believe the glove and rubber-related sectors will continue to perform, owing to the shortage of supply, and the pharmaceutical sector is also attractive from the earnings growth perspective.

Get in touch with RHB Premier today.

This publication has been prepared by RHB Bank Berhad and is solely for your information only. It may not be copied, published, circulated, reproduced or distributed in whole or part to any person without the prior written consent of RHB Bank Berhad. In preparing this article, RHB Bank Berhad has relied upon and assumed the accuracy and completeness of all information available from public references and articles or which was otherwise reviewed by RHB Bank Berhad. Accordingly, whilst we have taken all reasonable care to ensure that the information contained in this article is not untrue or misleading at the time of publication, we cannot guarantee its accuracy or completeness or fairness of such opinions and make no representation or warranty (whether expressed or implied) and accept no responsibility or liability for its accuracy or completeness. You should not act on the information contained in this article without first independently verifying its contents.

Any opinion, historical account, personal profile, estimate or data contained in this article is based on information available as of the date of this article and are subject to change without notice. It does not constitute any advice, offer or solicitation by RHB Bank Berhad. This document and its contents are not intended to constitute an offer for sale and/or invitation to subscribe for or purchase or otherwise acquire any of the instruments referred to herein.

Disclaimer for Video and Podcast by RHB Asset Management:The podcast provided herein is solely for information purposes only. It does not take into account the specific investment objectives, financial situations or particular needs of any particular person.

This podcast does not constitute an offer, solicitation or recommendation to buy or sell or subscribe for any security or financial instrument or to enter into any transaction or to participate in any particular trading or investment strategy. Information contained in the podcast should not be relied upon when making investment decisions. You should seek independent legal or tax advice before making any investment decisions. Investments are subject to investment risks, including the possible loss of the principal amount invested. Value of the investments and the income, if any, may fall or rise.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein and it should not be relied upon as such. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance.

Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same. RHBAM does not guarantee that all risks associated to the transactions mentioned herein have been identified, nor does it provide advice as to whether you should enter into any such transaction. The contents hereof may not be reproduced or disseminated in whole or in part without RHBAM’s written consent.

This podcast has not been reviewed by the Securities Commission Malaysia. You should not act on the information contained in this podcast without first independently verifying its contents.

Disclaimer for Video and Podcast by Economics and Market Strategy:This report is prepared for information purposes only by the Economics and Market Strategy division within RHB Bank Berhad and/or its subsidiaries related companies and affiliates, as applicable (“RHB”). All research is based on material compiled from data considered to be reliable at the time of writing, but RHB does not make any representation or warranty, express or implied, as to its accuracy, completeness or correctness.

Neither this report, nor any opinion expressed herein, should be construed as an offer to sell or a solicitation of an offer to acquire any securities or financial instruments mentioned herein. RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for any direct or consequential loss arising from the use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without prior consent of RHB and RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for the actions of third parties in this respect. Recipients are reminded that the financial circumstances surrounding any company or any market covered in the reports may change since the time of their publication. The contents of this report are also subject to change without any notification.

This report does not purport to be comprehensive or to contain all the information that a prospective investor may need in order to make an investment decision. The recipient of this report is making its own independent assessment and decisions regarding any securities or financial instruments referenced herein. Any investment discussed or recommended in this report may be unsuitable for an investor depending on the investor’s specific investment objectives and financial position. The material in this report is general information intended for recipients who understand the risks of investing in financial instruments. This report does not take into account whether an investment or course of action and any associated risks are suitable for the recipient. Any recommendations contained in this report must therefore not be relied upon as investment advice based on the recipient's personal circumstances. Investors should make their own independent evaluation of the information contained herein, consider their own investment objective, financial situation and particular needs and seek their own financial, business, legal, tax and other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report.

RHB (including its respective directors, associates, connected parties and/or employees) may own or have positions in securities or financial instruments of the company(ies) covered in this research report or any securities or financial instruments related thereto, and may from time to time add to, or dispose off, or may be materially interested in any such securities or financial instruments. Further, RHB does and seeks to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities or financial instruments of such company(ies), may sell them or buy them from customers on a principal basis and may also perform or seek to perform significant banking, advisory or underwriting services for or relating to such company(ies), as well as solicit such banking, advisory or other services from any entity mentioned in this research report.

RHB (including its respective directors, associates, connected parties and/or employees) do not accept any liability, be it directly, indirectly or consequential losses, loss of profits or damages that may arise from any reliance based on this report or further communication given in relation to this report, including where such losses, loss of profits or damages are alleged to have arisen due to the contents of such report or communication being perceived as defamatory in nature.

This podcast has not been reviewed by the Securities Commission (SC) and/or Bank Negara Malaysia (BNM).

RHB Bank Berhad 196501000373 (6171-M)