Quarterly Market Outlook

Strategic Shifts in Q2: Income and Value Opportunities in a Broadening Market Rally.

In our quarterly Fund Discovery series, we delve into current market conditions and provide insights and strategies to diversify your portfolio.

Listen and subscribe to the podcast version hosted by RHB Bank’s Head of Investors Advisory Nova Lui here to stay updated on the latest market developments.

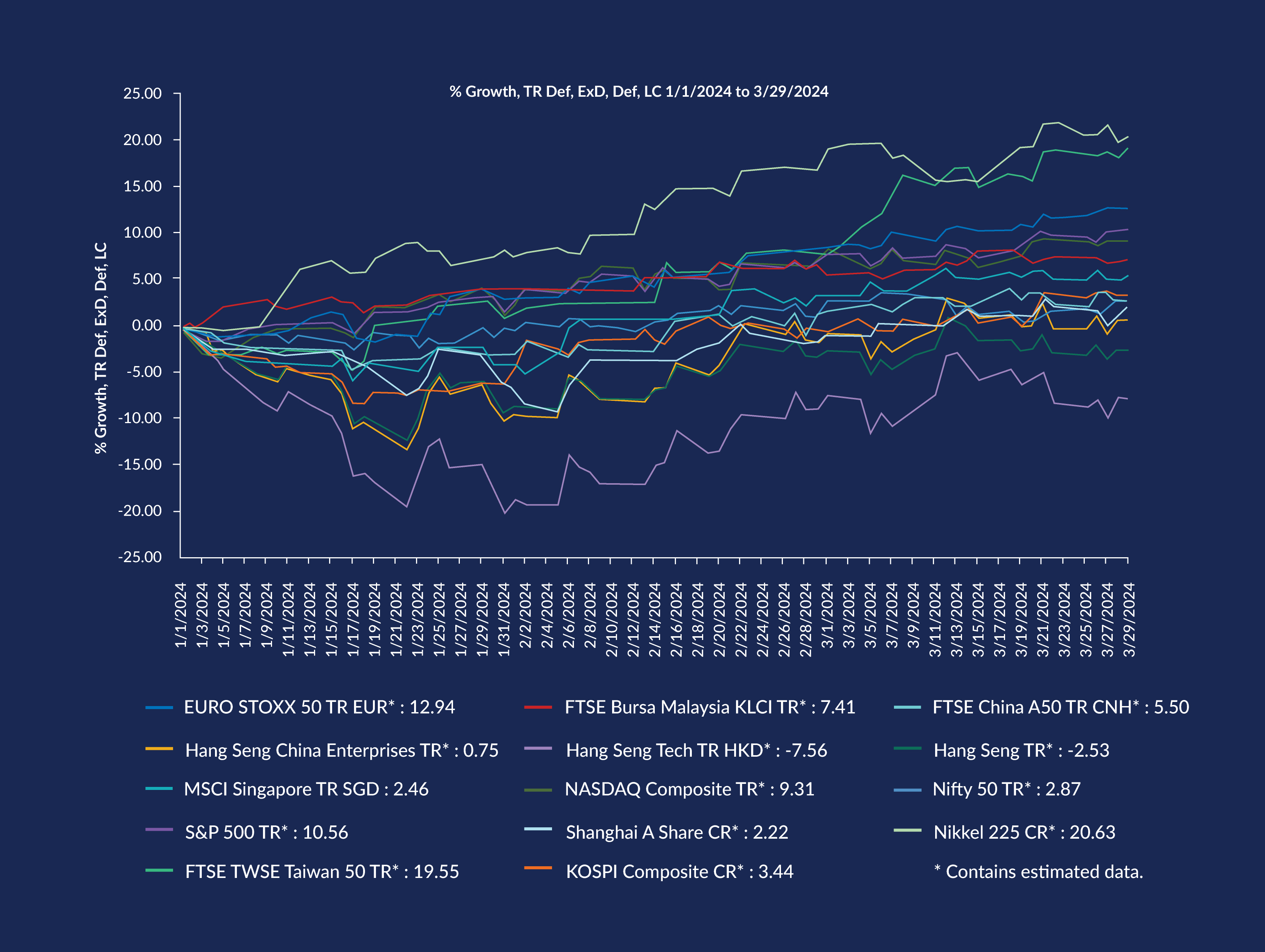

The first quarter of 2024 was a barrel of surprises. The major recession on the tips of our tongues was tactfully avoided, interest/profit rate cuts were pushed back, and the stock markets ended the quarter on a high note. As AI transitioned from buzzword to norm, technology stocks led gains in the equities space, while value stocks also claimed their fair share of attention.

In the equity market rally, developed markets such as Japan and Europe outperformed US equities. Within the US market, the S&P Index outperformed NASDAQ. Meanwhile, Taiwan proved a star player in emerging markets.

Source: Lipper Investment Management as of 31 March 2024.

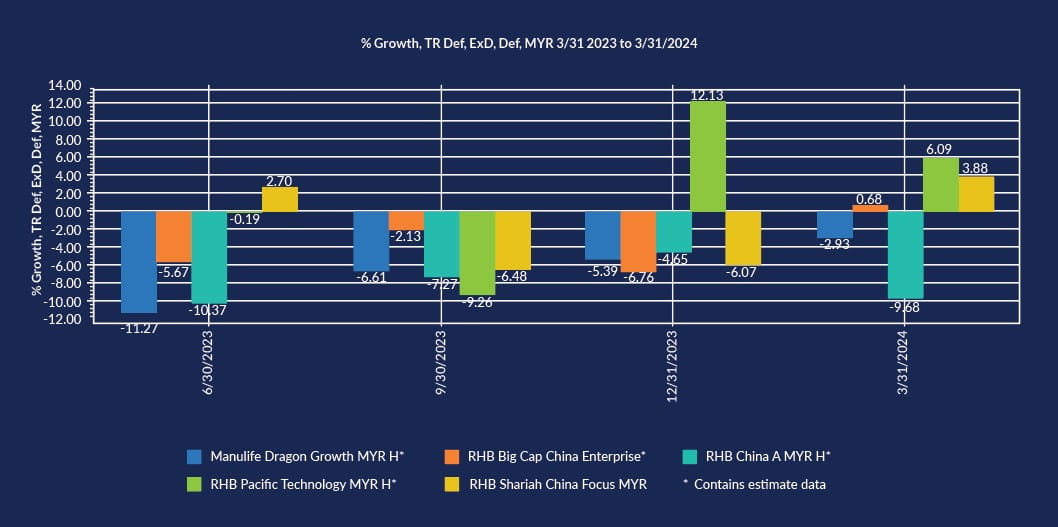

The picture was not as rosy for Hong Kong, where blue-chip stocks saw a decline. However, both the Hang Seng China Enterprise and Shanghai A Share indices ended the quarter on a slightly more positive note, gathering momentum in the second month, although it wasn’t anything to write home about. The lacklustre performance of the Chinese markets was attributed to the absence of significant stimulus measures from the government and concerns surrounding the financial health of property developers – the latter being a valid concern considering the collapse of the Evergrande Group.

Overall, Chinese equity funds showed support and signs of recovery, buoyed by their better value compared to the rest of the global equity market. Malaysia also proved to be attractive, with the market’s relative stability as its main selling point.

Source: Lipper Investment Management as of 31 March 2024.

To understand investors’ thought process, let’s look at how the money travelled in Q1.

Source: Lipper Investment Management as of 31 March 2024.

Most investors aimed for exposure, either through mixed assets or pure fixed income funds, to lock in the high fixed income yield in anticipation of aggressive rate cuts. Investors in mixed assets played safe, preferring the global space which would allow them to ride on any potential upside in equities while still keeping a hand on fixed income as a buffer. In terms of markets, the top three single-country funds were Singapore, Malaysia, and India.

Disappointed by its performance over the past year, investors exited the Absolute Return Fund, favouring a more focused exposure in spaces like the global technology market. A similar theme switch can be seen in the movement from global equities to a more singular strategy or sectoral theme, such as income, dividend, or technology.

The first quarter was marked the third consecutive quarter of net outflows from the China equity fund, as investors sought alternatives based on the China+1 story, investing in countries like India.

Key investment themes for Q2

As we enter the second quarter the question on everyone’s minds is: will the bull continue its rampage? To provide some insight, these are the three key investment themes we should pay attention to in Q2 2024.

1. A broader equity rally

Although AI remains a hot topic, fund managers are envisioning a further rally extending beyond the technology sector. While the equities market remains bullish, investors may look into areas which are more fairly valued and offer downside protection. In other words, keep your investor ears tuned out to the hype.

2. Income is IN

We see increasing inflow into “safer” strategies like REITs, dividends and income, which offer attractive yields while allowing the investor to enjoy any potential upside in the equity market. The income is handy as a buffer against any downside, while potential rate cuts could see appreciation in the equities space.

3. Value in emerging markets

Here’s the hidden dragon. Overall, the Asia Pacific equities market has shown resilience, and investors are showing interest in India and the ASEAN region, riding on the China+1 story. Malaysia offers an attractive entry point, with the advantage of being the familiar home turf.

Based on these themes, we’ve handpicked a few funds for you to diversify your portfolio with.

TA Global Absolute Alpha-i Fund

Source: Fund Fact Sheet as of 29 February 2024

Why we like this fund:

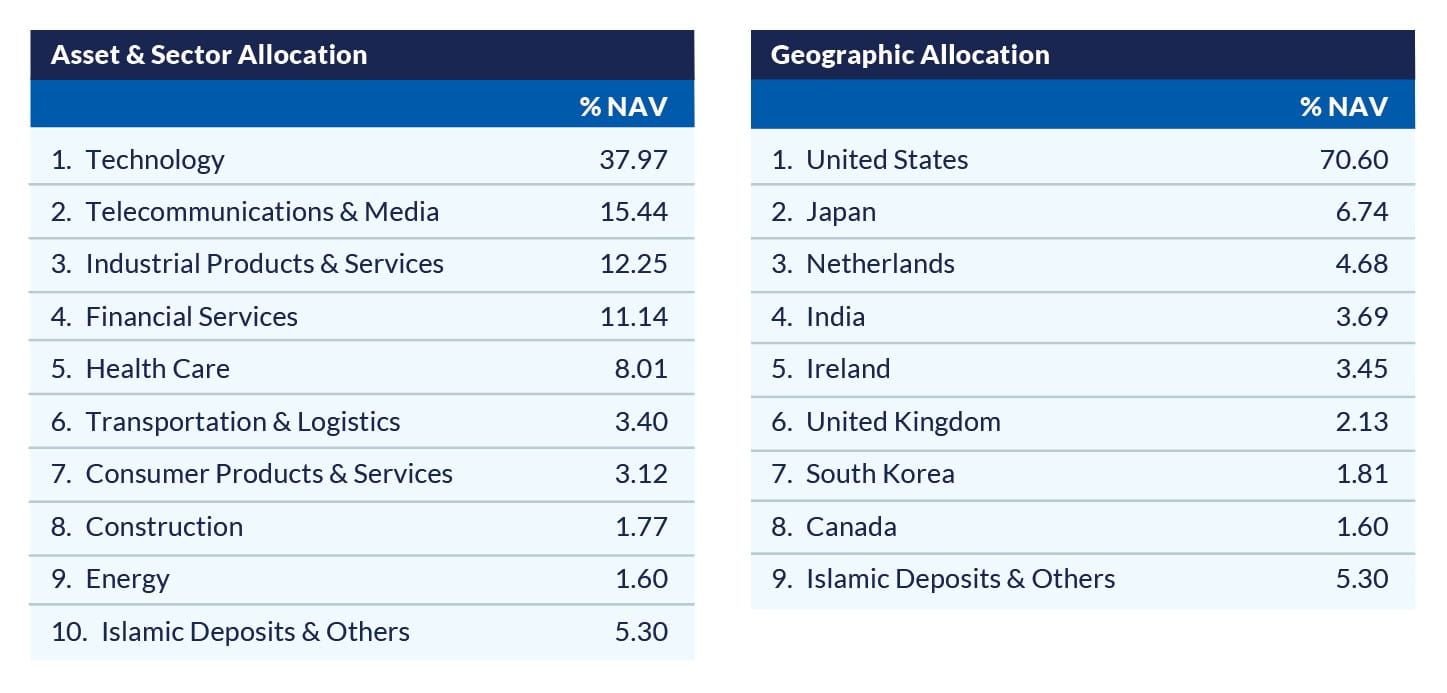

The bull will continue its run in the global equity space, but there will be a broadening out to other markets. Investors will benefit from a strategy that isn’t constrained by a benchmark. The fund mandate allows for bottom-up stock picking that is geographically agnostic. Besides the US, this fund has a relatively high exposure in Japan and Europe, and India and South Korea are in the top rankings, too.

RHB i-Sustainable Future Technology Fund

Source: Fund Fact Sheet as of 29 February 2024

Why we like this fund:

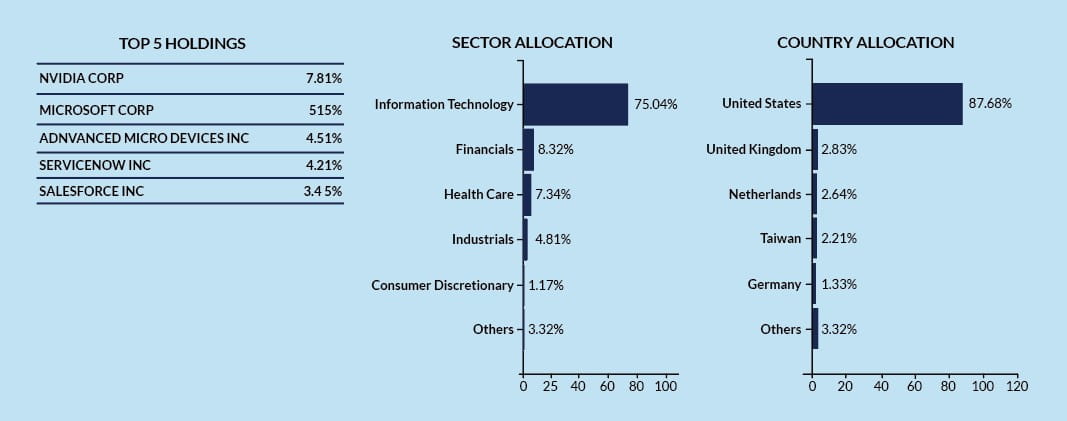

With the technology sector's solid track record so far in delivering consistent returns, it’s hard to ignore it. However, it would be wise to consider a more diversified approach for a better risk-return ratio. As proof, even the Magnificent 7 stocks haven’t all ended up in positive territory. The fund’s external manager is Janus Henderson, known for their extensive experience in managing global technology funds. Their expertise would be put to great use in stock picking.

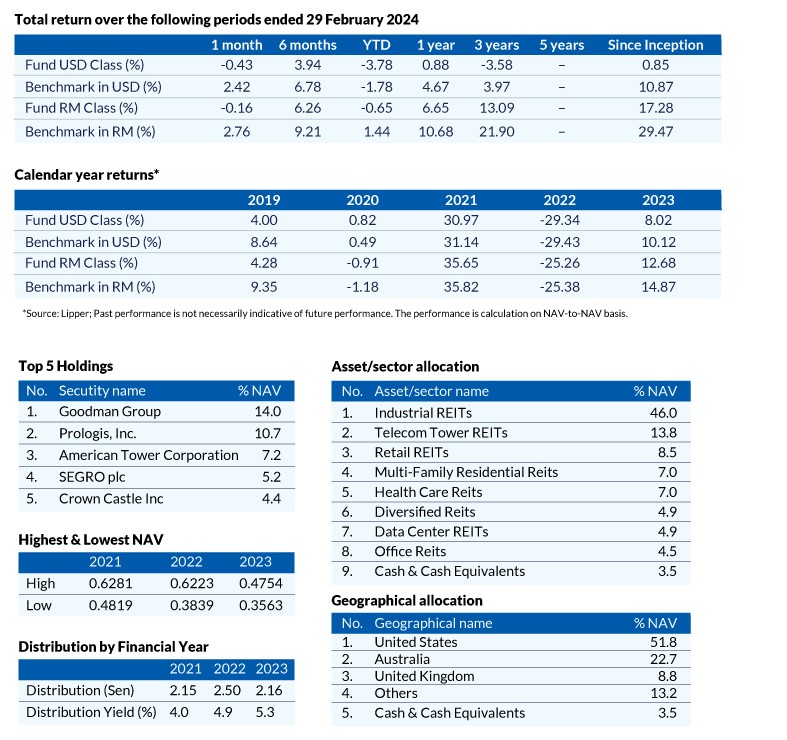

Manulife Shariah Global REIT Fund

Source: Fund Fact Sheet as of 29 February 2024

Why we like this fund:

Moving on to the income theme, this fund remains a great option for diversification. Due to the increasing pressure of rate hikes over the past two years, the fund has placed pressure on many income assets. With a pivot in interest/profit rates looming on the horizon, this fund is well-positioned to still provide the opportunity to accumulate income assets for long-term potential growth. REIT holders typically enjoy both the benefits of capital gain from the equity market and income payouts.

RHB Global Equity Premium Income Fund

Source: J.P. Morgan, RHBAM, March 2024 For illustration purposes only. The manager seeks to achieve the stated objectives. There can be no guarantee the objectives will be met.

1This is not a guaranteed annual payout. The Fund Manager may in the future review the distribution policy depending on prevailing market conditions.

Why we like this fund:

This is a new fund that we will be launching, but that’s not the only reason why we like it. This fund forms the core of our Income Investing strategy, and targets 7-9% per annum (paid out monthly). It aims to achieve a consistent payout from underlying dividends and collecting option premiums. At the same time, the fund also benefits from the upside potential of the underlying equity portfolio, which is actively managed by the J.P. Morgan Global Premium Income Investment Team.

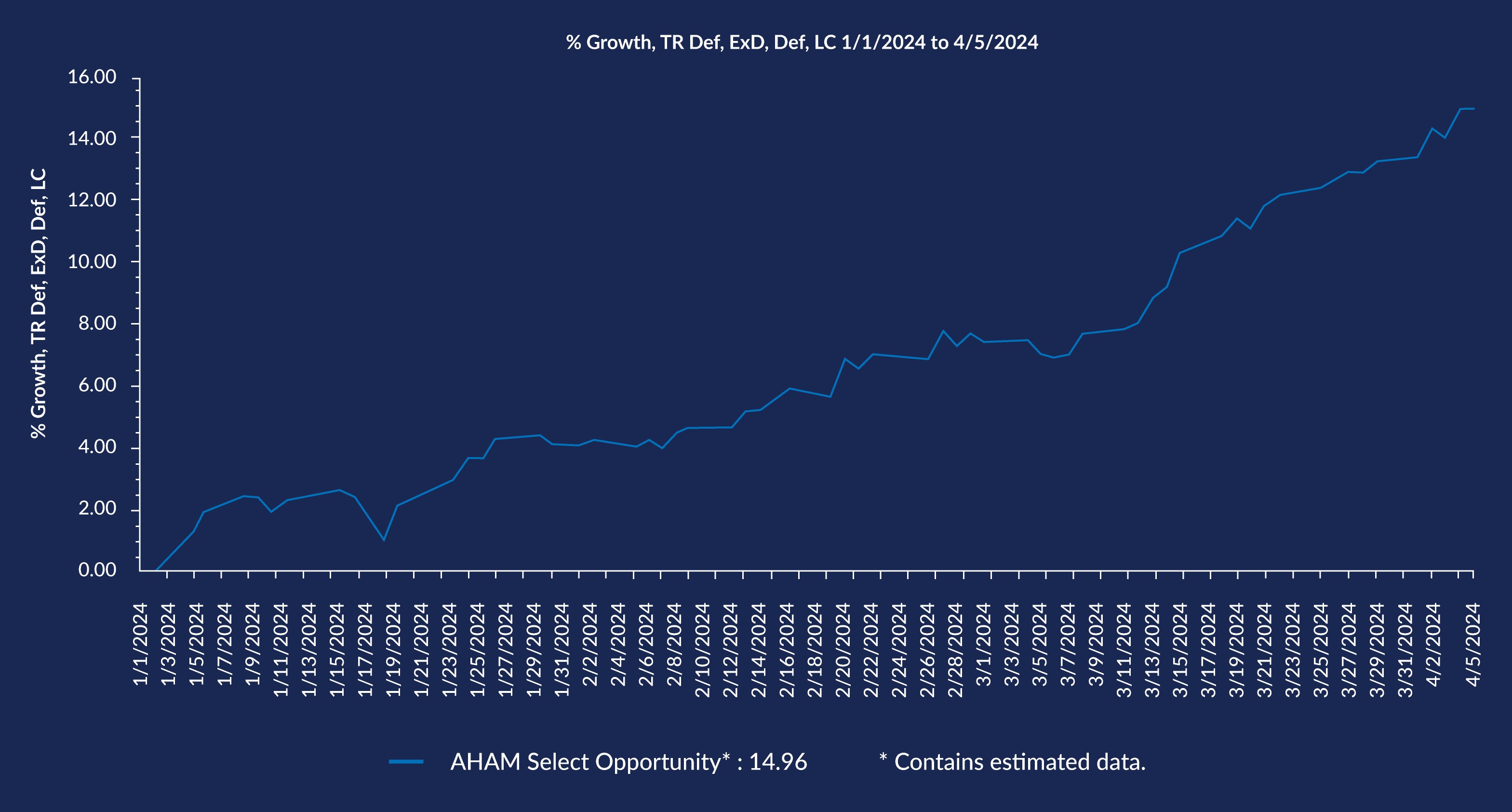

AHAM Select Opportunity Fund

Source: Lipper Investment Management as of 31 March 2024

Why we like this fund:

While it isn’t as attractive compared with a global technology fund, there is still plenty of merit here considering its relatively low volatility and gradual upward momentum, with returns averaging close to 15% annually. Since its launch, annualised returns stand at 11.3% offering a good opportunity for long-term growth in a more fairly valued emerging market space.

Finally, to reiterate our point on the grass being just as green on this side, investors should take the opportunity to relook into Malaysian funds. The entry point is attractive, and the weaker ringgit will be hard for foreign investors to resist. The Rapid Transit System (RTS) and other infrastructure projects are a good prospect to boost sentiment, backed by a relatively accommodative monetary policy.

Investing is dynamic, so keep your eye on market conditions and regularly review your portfolio. Get in touch with your Relationship Manager to see which of the options we mentioned would best suit your risk profile and goals.

Get in touch with RHB Premier today.

This publication has been prepared by RHB Bank Berhad and is solely for your information only. It may not be copied, published, circulated, reproduced or distributed in whole or part to any person without the prior written consent of RHB Bank Berhad. In preparing this article, RHB Bank Berhad has relied upon and assumed the accuracy and completeness of all information available from public references and articles or which was otherwise reviewed by RHB Bank Berhad. Accordingly, whilst we have taken all reasonable care to ensure that the information contained in this article is not untrue or misleading at the time of publication, we cannot guarantee its accuracy or completeness or fairness of such opinions and make no representation or warranty (whether expressed or implied) and accept no responsibility or liability for its accuracy or completeness. You should not act on the information contained in this article without first independently verifying its contents.

Any opinion, historical account, personal profile, estimate or data contained in this article is based on information available as of the date of this article and are subject to change without notice. It does not constitute any advice, offer or solicitation by RHB Bank Berhad. This document and its contents are not intended to constitute an offer for sale and/or invitation to subscribe for or purchase or otherwise acquire any of the instruments referred to herein.

Disclaimer for Video and Podcast by RHB Asset Management:The podcast provided herein is solely for information purposes only. It does not take into account the specific investment objectives, financial situations or particular needs of any particular person.

This podcast does not constitute an offer, solicitation or recommendation to buy or sell or subscribe for any security or financial instrument or to enter into any transaction or to participate in any particular trading or investment strategy. Information contained in the podcast should not be relied upon when making investment decisions. You should seek independent legal or tax advice before making any investment decisions. Investments are subject to investment risks, including the possible loss of the principal amount invested. Value of the investments and the income, if any, may fall or rise.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein and it should not be relied upon as such. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance.

Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same. RHBAM does not guarantee that all risks associated to the transactions mentioned herein have been identified, nor does it provide advice as to whether you should enter into any such transaction. The contents hereof may not be reproduced or disseminated in whole or in part without RHBAM’s written consent.

This podcast has not been reviewed by the Securities Commission Malaysia. You should not act on the information contained in this podcast without first independently verifying its contents.

Disclaimer for Video and Podcast by Economics and Market Strategy:This report is prepared for information purposes only by the Economics and Market Strategy division within RHB Bank Berhad and/or its subsidiaries related companies and affiliates, as applicable (“RHB”). All research is based on material compiled from data considered to be reliable at the time of writing, but RHB does not make any representation or warranty, express or implied, as to its accuracy, completeness or correctness.

Neither this report, nor any opinion expressed herein, should be construed as an offer to sell or a solicitation of an offer to acquire any securities or financial instruments mentioned herein. RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for any direct or consequential loss arising from the use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without prior consent of RHB and RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for the actions of third parties in this respect. Recipients are reminded that the financial circumstances surrounding any company or any market covered in the reports may change since the time of their publication. The contents of this report are also subject to change without any notification.

This report does not purport to be comprehensive or to contain all the information that a prospective investor may need in order to make an investment decision. The recipient of this report is making its own independent assessment and decisions regarding any securities or financial instruments referenced herein. Any investment discussed or recommended in this report may be unsuitable for an investor depending on the investor’s specific investment objectives and financial position. The material in this report is general information intended for recipients who understand the risks of investing in financial instruments. This report does not take into account whether an investment or course of action and any associated risks are suitable for the recipient. Any recommendations contained in this report must therefore not be relied upon as investment advice based on the recipient's personal circumstances. Investors should make their own independent evaluation of the information contained herein, consider their own investment objective, financial situation and particular needs and seek their own financial, business, legal, tax and other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report.

RHB (including its respective directors, associates, connected parties and/or employees) may own or have positions in securities or financial instruments of the company(ies) covered in this research report or any securities or financial instruments related thereto, and may from time to time add to, or dispose off, or may be materially interested in any such securities or financial instruments. Further, RHB does and seeks to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities or financial instruments of such company(ies), may sell them or buy them from customers on a principal basis and may also perform or seek to perform significant banking, advisory or underwriting services for or relating to such company(ies), as well as solicit such banking, advisory or other services from any entity mentioned in this research report.

RHB (including its respective directors, associates, connected parties and/or employees) do not accept any liability, be it directly, indirectly or consequential losses, loss of profits or damages that may arise from any reliance based on this report or further communication given in relation to this report, including where such losses, loss of profits or damages are alleged to have arisen due to the contents of such report or communication being perceived as defamatory in nature.

This podcast has not been reviewed by the Securities Commission (SC) and/or Bank Negara Malaysia (BNM).

RHB Bank Berhad 196501000373 (6171-M)