Quarterly Market Outlook

Opportunity in EM bonds

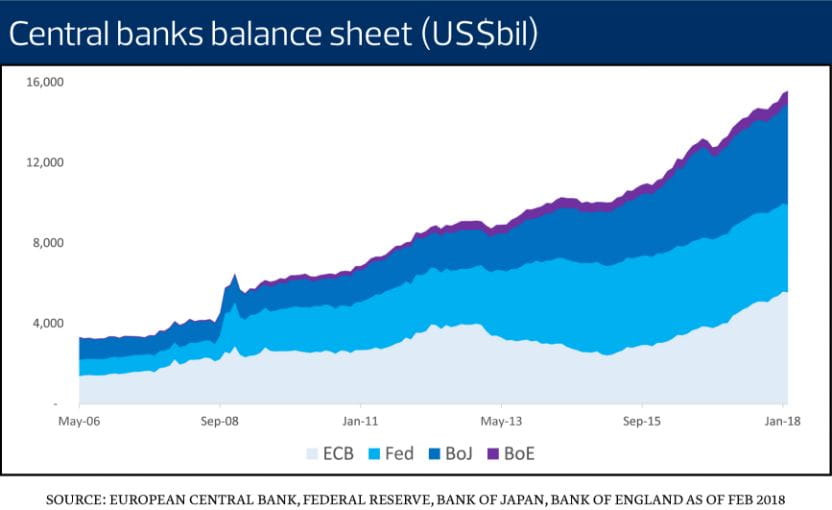

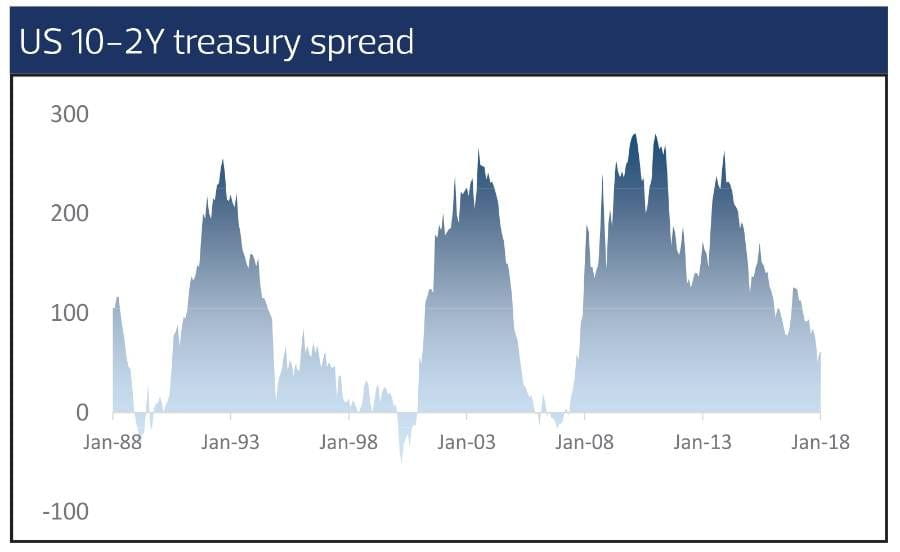

US Treasury yields are expected to spike in 2018, according to the RHB Wealth Research team, followed by European and Japan government bond yields. Bond prices will then be pressured accordingly. The fall in bond prices might take place simultaneously with the correction in share prices as the US market undergoes its long overdue correction in which witnessed in February.

On the other hand, investors should be cautious of the fixed income space and allocate more to shorter duration instruments to limit their exposure to rising rates, warns the RHB Wealth Research team. Credit spreads for Investment Grade (IG) and High-Yield (HY) bonds against the Treasuries are hovering at their lowest levels since the previous peak in early 2016. The credit market is also now pricing in economy stability and the slow and shallow path of normalisation. The spreads within US IG and US HY is now at 230 bps (the historical low is at 160 bps). At this point of time, the team prefers IG bonds against the backdrop of reduced compensation for credit risk.

However, the team underweights US, Euro and Japan bonds. Instead, emerging market (EM) bonds are preferred over developed market (DM) bonds as central banks in the EM region have not cut rates as much compared to those in DM. There is lower risk of a rate hike so there are more reasonable risk-adjusted opportunities within the EM. The team also suggest investors to underweight sovereign bonds — especially those with negative yields — because their valuations are distorted.

Better opportunities in non-US stocks

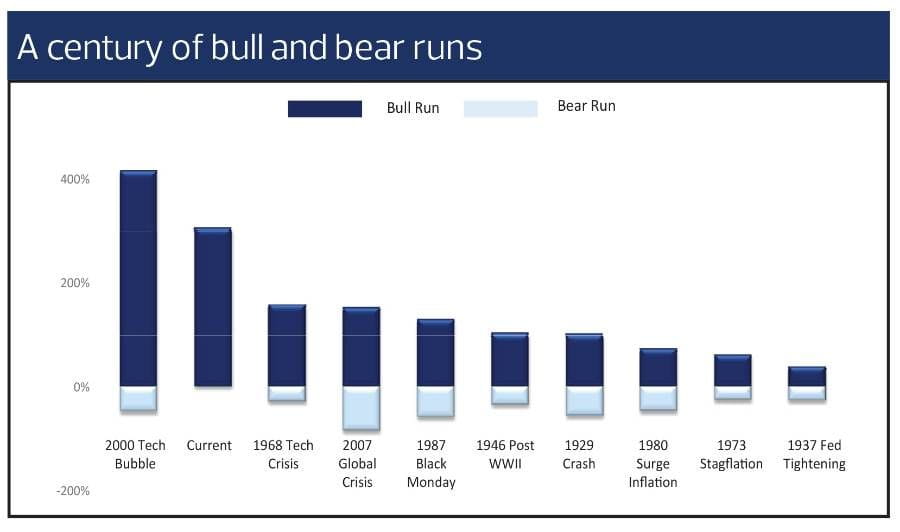

With regards to equities, the RHB Wealth Research team prefers large cap stocks rather than small and mid-cap stocks due to its stability. This is in line with the team’s view that volatility will return in 2018 after a rally in 2017, with the US stock market delivering a Sharpe ratio of close to 4.0.

US stocks are now more expensive than non-US stocks and with the mean reversion likely to happen this for non-US stocks. This is reflected by the rapidly increasing earnings momentum outside the US. The RHB Wealth Research team believes that the transformation in China and India will likely to lead the Asian equity market registering relatively higher returns. The bullishness for EM equities is echoed by Grantham, who has called for investors to own as much emerging market equity risk as they can handle.

In terms of sectors, the RHB Wealth Research team prefers energy stocks with a strong conviction given the broad-based recovery in energy prices. It will benefit profit margins of the companies, who have become leaner after years of transformation. Other sectors such as banking are also poised to benefit from higher interest rates and growth in economic activity. The team is optimistic on evergreen sectors such as healthcare, as there is growing concern regarding rising healthcare costs throughout the past decades. On the other hand, the team suggests investors avoid utilities and telco services that have lesser upside catalysts; and to grab the correction as buying opportunity. Correction shall be deemed as healthy as long as the fundamental remains solid.

Diversify into alternative investments

To achieve the benefits of diversification, investors can set aside some percentage of their portfolio and venture into alternative investments (structured products) and commodities, such as gold and oil. Major banks including JP Morgan and Bank of America Merrill Lynch have raised their Brent crude oil price targets for the year as they expect oil prices to recover after a weak performance in 2017. The asset allocation towards equity, fixed income and alternative assets such as commodities will depend on the individual’s risk appetite. Investors with a higher risk appetite can consider increasing their exposure to equities andcommodities.

For investors who want to gain exposure to these trends and themes, they can check out the wide range For instance, investors who want to gain exposure to the theme of rising commodity prices can do so via the Dual Currency Investment product Investors can also gain exposure to global synchronised growth by investing in global equity, global mixed asset and/or global fixed income via a wide range of product suites in the RHB fund shelf. They can also talk to the RHB Premier Relationship Manager on how to construct their own portfolios based on their risk appetite, time horizon and goals.

Get in touch with RHB Premier today.

This publication has been prepared by RHB Bank Berhad and is solely for your information only. It may not be copied, published, circulated, reproduced or distributed in whole or part to any person without the prior written consent of RHB Bank Berhad. In preparing this article, RHB Bank Berhad has relied upon and assumed the accuracy and completeness of all information available from public references and articles or which was otherwise reviewed by RHB Bank Berhad. Accordingly, whilst we have taken all reasonable care to ensure that the information contained in this article is not untrue or misleading at the time of publication, we cannot guarantee its accuracy or completeness or fairness of such opinions and make no representation or warranty (whether expressed or implied) and accept no responsibility or liability for its accuracy or completeness. You should not act on the information contained in this article without first independently verifying its contents.

Any opinion, historical account, personal profile, estimate or data contained in this article is based on information available as of the date of this article and are subject to change without notice. It does not constitute any advice, offer or solicitation by RHB Bank Berhad. This document and its contents are not intended to constitute an offer for sale and/or invitation to subscribe for or purchase or otherwise acquire any of the instruments referred to herein.

Disclaimer for Video and Podcast by RHB Asset Management:The podcast provided herein is solely for information purposes only. It does not take into account the specific investment objectives, financial situations or particular needs of any particular person.

This podcast does not constitute an offer, solicitation or recommendation to buy or sell or subscribe for any security or financial instrument or to enter into any transaction or to participate in any particular trading or investment strategy. Information contained in the podcast should not be relied upon when making investment decisions. You should seek independent legal or tax advice before making any investment decisions. Investments are subject to investment risks, including the possible loss of the principal amount invested. Value of the investments and the income, if any, may fall or rise.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein and it should not be relied upon as such. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance.

Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same. RHBAM does not guarantee that all risks associated to the transactions mentioned herein have been identified, nor does it provide advice as to whether you should enter into any such transaction. The contents hereof may not be reproduced or disseminated in whole or in part without RHBAM’s written consent.

This podcast has not been reviewed by the Securities Commission Malaysia. You should not act on the information contained in this podcast without first independently verifying its contents.

Disclaimer for Video and Podcast by Economics and Market Strategy:This report is prepared for information purposes only by the Economics and Market Strategy division within RHB Bank Berhad and/or its subsidiaries related companies and affiliates, as applicable (“RHB”). All research is based on material compiled from data considered to be reliable at the time of writing, but RHB does not make any representation or warranty, express or implied, as to its accuracy, completeness or correctness.

Neither this report, nor any opinion expressed herein, should be construed as an offer to sell or a solicitation of an offer to acquire any securities or financial instruments mentioned herein. RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for any direct or consequential loss arising from the use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without prior consent of RHB and RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for the actions of third parties in this respect. Recipients are reminded that the financial circumstances surrounding any company or any market covered in the reports may change since the time of their publication. The contents of this report are also subject to change without any notification.

This report does not purport to be comprehensive or to contain all the information that a prospective investor may need in order to make an investment decision. The recipient of this report is making its own independent assessment and decisions regarding any securities or financial instruments referenced herein. Any investment discussed or recommended in this report may be unsuitable for an investor depending on the investor’s specific investment objectives and financial position. The material in this report is general information intended for recipients who understand the risks of investing in financial instruments. This report does not take into account whether an investment or course of action and any associated risks are suitable for the recipient. Any recommendations contained in this report must therefore not be relied upon as investment advice based on the recipient's personal circumstances. Investors should make their own independent evaluation of the information contained herein, consider their own investment objective, financial situation and particular needs and seek their own financial, business, legal, tax and other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report.

RHB (including its respective directors, associates, connected parties and/or employees) may own or have positions in securities or financial instruments of the company(ies) covered in this research report or any securities or financial instruments related thereto, and may from time to time add to, or dispose off, or may be materially interested in any such securities or financial instruments. Further, RHB does and seeks to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities or financial instruments of such company(ies), may sell them or buy them from customers on a principal basis and may also perform or seek to perform significant banking, advisory or underwriting services for or relating to such company(ies), as well as solicit such banking, advisory or other services from any entity mentioned in this research report.

RHB (including its respective directors, associates, connected parties and/or employees) do not accept any liability, be it directly, indirectly or consequential losses, loss of profits or damages that may arise from any reliance based on this report or further communication given in relation to this report, including where such losses, loss of profits or damages are alleged to have arisen due to the contents of such report or communication being perceived as defamatory in nature.

This podcast has not been reviewed by the Securities Commission (SC) and/or Bank Negara Malaysia (BNM).

RHB Bank Berhad 196501000373 (6171-M)