Quarterly Market Outlook

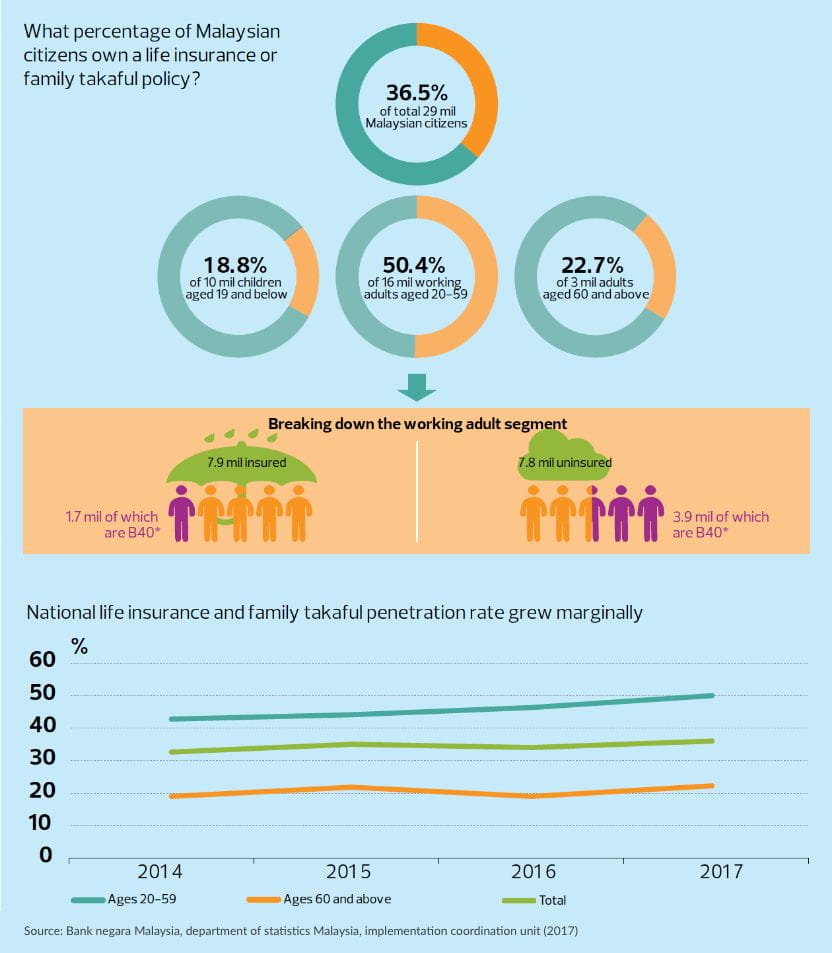

There is a lack of awareness of the importants of buying life insurance in Malaysia. According to Bank Negara Malaysia, only 36.5% of the total population owns at least one individual life insurance or family takaful plan, which is very low compared with the government’s target of 75% by 2020. Despite the penetration of the working age group (20 to 59) showing strong signs of growth to 50.4% as at 2017, national-level growth has been stagnant.

Without life insurance protection, one would most likely have to self-fund medical costs and treatment expenses. There is also the possibility of loss of income in the event of being unable to work due to a permanent disability. But if someone is adequately protected under a life policy, they would receive a permanent disability benefit of a lump-sum payout.

Even with a proper will in place, wealth distribution to the next kin or family can be a lengthy process. Therefore, in the event that an uninsured individual is the sole breadwinner of the family, the financial requirements to sustain day-to-day family life could be severely impacted.

But if one is adequately covered, the family will be financially independent regardless of age and would be able to leverage their policies to minimise disruptions to the current lifestyle and financial commitments.

Even if one is insured, one cannot assume that they are adequately insured. Many Malaysians think they have enough coverage from a policy they bought years ago, or that was bought by their parents when they were younger.

Life insurance needs will continuously change as an individual progresses through their life stages, such as marriage and having children. The needs also increase parallel to their requirements for income replacement or maintenance of lifestyle, especially if any unforeseen events take place. Therefore, it is important to periodically review one’s wealth, assets and financial obligations to ensure they match the value of the life insurance purchased.

While it may seem that the wealthy do not need life insurance as they would have sufficient financial capacity, it is still necessary and can assist them in several ways.

For one, taking up the right life insurance policy would allow affluent individuals to preserve their assets and lifestyle as insurance proceeds are almost instant — it does not attract the usual complications of administering an estate transfer. An estate equalisation can also be made, where the liquidity of life insurance can be used to balance the share of the estate to beneficiaries. RHB tailor-makes for our clients comprehensive life insurance solutions to meet their needs. Tai believes that life insurance products, such as the RHB Prime Vantagelife, offers customers who wish to build their legacy plans flexible premium payment and coverage terms that come with high protection coverage, while being able to boost wealth accumulation through guaranteed cash payments and investment top-up options.

While fundamentally a protection, the current features of life insurance plans have expanded to help an individual attain their financial goals, such as being an alternative asset class that can provide financial security, liquidity and potential returns. It also helps to build and preserve a legacy of choice for the next generation, with the flexibility to refine the estate plans when necessary.

In addition, it can support business continuity or succession, especially in the case of businesses with multiple owners. For example, in the event of the untimely death or critical illness of one of the owners, the life policy payout can be used to fund the buyout of his business interest without causing financial hardship to the business or other partners.

While the options for life insurance in the market come in many different variations, they are generally known as term life, whole life, endowment or investment-linked.

Term life refers to the most basic type of life insurance coverage, providing simple life cover with no elements of savings or profit component. The coverage is fixed for a set period with no cash values accumulated to the policy. Whole life refers to life insurance that provides coverage throughout the lifetime of the assured, as long as the premiums are paid.

Endowment is a life policy that combines protection and saving components, which can build up a lump-sum maturity benefit, usually paid out at the end of the policy period. Lastly, investment-linked is a policy that combines insurance protection with elements of investment through various investment fund types according to the assured’s risk profile. The flexibility of investment-linked policies has generated a stream of innovative product variations to cater for the different financial and protection needs.

While there will not be one best insurance product to cater for all of an individual’s needs, RHB highlights that it is crucial to seek professional advice from qualified personnel who will be able to recommend and tailor the right combination of financial solutions, including life insurance, taking into consideration the customer’s financial plans and needs.

Get in touch with RHB Premier today.

This publication has been prepared by RHB Bank Berhad and is solely for your information only. It may not be copied, published, circulated, reproduced or distributed in whole or part to any person without the prior written consent of RHB Bank Berhad. In preparing this article, RHB Bank Berhad has relied upon and assumed the accuracy and completeness of all information available from public references and articles or which was otherwise reviewed by RHB Bank Berhad. Accordingly, whilst we have taken all reasonable care to ensure that the information contained in this article is not untrue or misleading at the time of publication, we cannot guarantee its accuracy or completeness or fairness of such opinions and make no representation or warranty (whether expressed or implied) and accept no responsibility or liability for its accuracy or completeness. You should not act on the information contained in this article without first independently verifying its contents.

Any opinion, historical account, personal profile, estimate or data contained in this article is based on information available as of the date of this article and are subject to change without notice. It does not constitute any advice, offer or solicitation by RHB Bank Berhad. This document and its contents are not intended to constitute an offer for sale and/or invitation to subscribe for or purchase or otherwise acquire any of the instruments referred to herein.

Disclaimer for Video and Podcast by RHB Asset Management:The podcast provided herein is solely for information purposes only. It does not take into account the specific investment objectives, financial situations or particular needs of any particular person.

This podcast does not constitute an offer, solicitation or recommendation to buy or sell or subscribe for any security or financial instrument or to enter into any transaction or to participate in any particular trading or investment strategy. Information contained in the podcast should not be relied upon when making investment decisions. You should seek independent legal or tax advice before making any investment decisions. Investments are subject to investment risks, including the possible loss of the principal amount invested. Value of the investments and the income, if any, may fall or rise.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein and it should not be relied upon as such. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance.

Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same. RHBAM does not guarantee that all risks associated to the transactions mentioned herein have been identified, nor does it provide advice as to whether you should enter into any such transaction. The contents hereof may not be reproduced or disseminated in whole or in part without RHBAM’s written consent.

This podcast has not been reviewed by the Securities Commission Malaysia. You should not act on the information contained in this podcast without first independently verifying its contents.

Disclaimer for Video and Podcast by Economics and Market Strategy:This report is prepared for information purposes only by the Economics and Market Strategy division within RHB Bank Berhad and/or its subsidiaries related companies and affiliates, as applicable (“RHB”). All research is based on material compiled from data considered to be reliable at the time of writing, but RHB does not make any representation or warranty, express or implied, as to its accuracy, completeness or correctness.

Neither this report, nor any opinion expressed herein, should be construed as an offer to sell or a solicitation of an offer to acquire any securities or financial instruments mentioned herein. RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for any direct or consequential loss arising from the use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without prior consent of RHB and RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for the actions of third parties in this respect. Recipients are reminded that the financial circumstances surrounding any company or any market covered in the reports may change since the time of their publication. The contents of this report are also subject to change without any notification.

This report does not purport to be comprehensive or to contain all the information that a prospective investor may need in order to make an investment decision. The recipient of this report is making its own independent assessment and decisions regarding any securities or financial instruments referenced herein. Any investment discussed or recommended in this report may be unsuitable for an investor depending on the investor’s specific investment objectives and financial position. The material in this report is general information intended for recipients who understand the risks of investing in financial instruments. This report does not take into account whether an investment or course of action and any associated risks are suitable for the recipient. Any recommendations contained in this report must therefore not be relied upon as investment advice based on the recipient's personal circumstances. Investors should make their own independent evaluation of the information contained herein, consider their own investment objective, financial situation and particular needs and seek their own financial, business, legal, tax and other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report.

RHB (including its respective directors, associates, connected parties and/or employees) may own or have positions in securities or financial instruments of the company(ies) covered in this research report or any securities or financial instruments related thereto, and may from time to time add to, or dispose off, or may be materially interested in any such securities or financial instruments. Further, RHB does and seeks to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities or financial instruments of such company(ies), may sell them or buy them from customers on a principal basis and may also perform or seek to perform significant banking, advisory or underwriting services for or relating to such company(ies), as well as solicit such banking, advisory or other services from any entity mentioned in this research report.

RHB (including its respective directors, associates, connected parties and/or employees) do not accept any liability, be it directly, indirectly or consequential losses, loss of profits or damages that may arise from any reliance based on this report or further communication given in relation to this report, including where such losses, loss of profits or damages are alleged to have arisen due to the contents of such report or communication being perceived as defamatory in nature.

This podcast has not been reviewed by the Securities Commission (SC) and/or Bank Negara Malaysia (BNM).

RHB Bank Berhad 196501000373 (6171-M)