Quarterly Market Outlook

We believe the budget was very balanced in addressing both growth and fiscal constraints. Relative to the MOF, we are more constructive on the fiscal outlook (Figure 1). Broadly, Budget 2021 focuses on substantial support for the economy, given the current challenging macroeconomic and financial markets backdrop, which in turn has been partially due to the COVID-19 pandemic. At the same time, the MOF also had the country’s fiscal constraints in mind when formulating the budget. We expect the budget rollout to be more aggressive in 1H21, given the more pressing need to stabilise the economy.

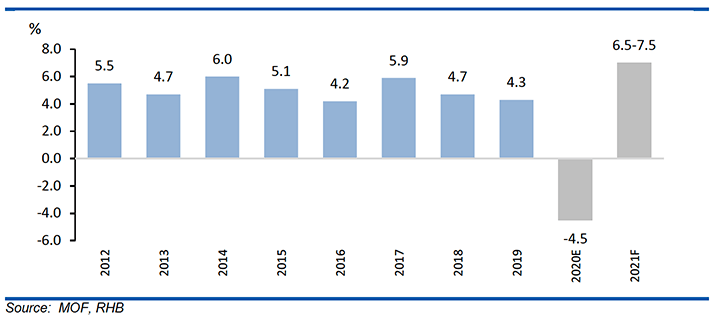

We also deem the MOF’s real GDP growth forecast of 6.5-7.5% for 2021 (from a contraction of -4.5% YoY in 2020F) as realistic (Figure 2). We are in broad agreement with the Government’s optimistic view of the economy in 2021F, with our in-house GDP growth estimated at 7% YoY.

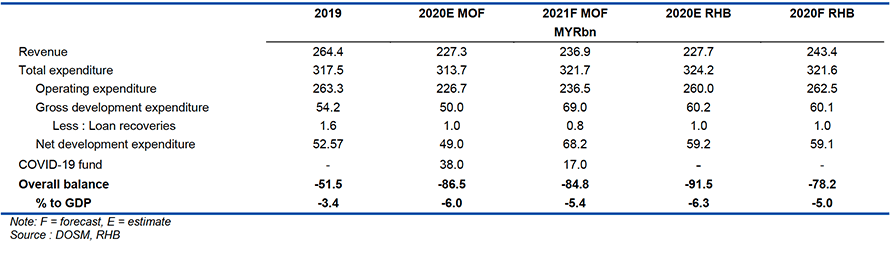

Finance Minister Datuk Seri Tengku Zafrul Tengku Abdul Aziz tabled an expansive budget worth MYR304.7bn for 2021, representing an increase of 10.5% YoY from 2020. Including a special COVID-19 fund amounting to MYR17bn in 2021, this takes the total to MYR321.7bn, implying a 2.6% increase from the previous year.

The operating expenditure (OE) allocation for 2021 will increase by 4.3% YoY to MYR236.5bn, while development expenditure (DE) will rise by a staggering 39.2% (MYR68.2bn) – far higher than the MYR50bn allocated in 2020, and the loftiest on record.

Revenue-wise, there were not many surprises. Higher contributions are expected from all segments, amid expected better economic conditions in 2021. The high dividends that the Government enjoyed in the past are no longer the case this time, with Petronas dividends falling to MYR18bn as oil prices tanked.

Budget 2021 is expected to record a narrower deficit of 5.4% of GDP or MYR84.5bn in 2021, compared to an estimated low of 6% in 2020. At this level, we believe the Government could embark on a fiscal consolidation path while stabilising the economy at the same time.

This should help allay the concerns of credit rating agencies, as the Government remains focused on getting the fiscal deficit back to 4% of GDP in the next four years, as committed to previously.

We were fairly surprised by the significantly large allocation for DE. The focus of DE is primarily towards transportation (MYR15bn; 2020: MYR10.1bn), education (MYR8.9bn; 2020: MYR5.9bn), and healthcare (MYR4.7bn; 2020: MYR2.9bn). Areas for this allocation include:

Transport-related spending. This includes the construction of an electrified doubletrack railway connecting Gemas and Johor Bahru, the Pan Borneo Highway, the Klang Valley Double Track project, the Rapid Transit System, as well as Kuantan Port and Sandakan Airport expansion;

Upgrades of schools, universities and training infrastructure;

Construction of hospitals in small districts, as well as construction of the National Centre for Food Safety.

We think the increase in allocation will likely boost construction activity and be supportive of economic growth in 2021.

On the social front, Budget 2021 has goodies for the B40 group and the public at large. The Cost of Living Allowance has been rebranded to capture a larger scope of beneficiaries (to 8.1m people from 4.3m), while the payment amount per household has been increased by about 20- 40%. On top of that, the Government has allowed the public to make withdrawals from their Employees Provident Fund (EPF) accounts – specifically, from Account 1 by MYR500.00 per month, to up to MYR6,000 a year. These, among other smaller measures, will likely continue providing support to private consumption, which is projected by the Government to rebound by 7.1% YoY next year (2020 estimate: -0.7% YoY).

Figure 1: Compared to the MOF, we are relatively constructive on the fiscal outlook for 2020…

Much to our expectation, several measures deemed successful this year have been extended. These include the continued reduction in EPF contributions from 11% to 9% (extended to end-2021). The special tax programme for companies relocating to Malaysia will be extended until end-2022. The targeted wage subsidy programme has also gotten a 3-month extension, for tourism-related jobs (until 1Q21). Meanwhile, the stamp duty for property purchases has been extended to Dec 2025.

On housing, measures to address the property overhang appear limited. Except for the extension of the stamp duty exemption, much of the measures for the property sector remain focused on the B40 group. These include an increase in the allocation for public housing, as well as the rent-to-own scheme.

For businesses, the focus is directed towards high technologies. Government has provided some incentives that include MYR1bn in investment incentives for projects in technology and high value-added areas. Another MYR1bn has been allocated for businesses’ digital transformation. We were hoping to see more measures supporting green technology, but there were almost no clear initiatives on this front. Overall, we believe these measures – while positive – will have a limited impact on private investment, unless the economic environment improves.

First Integral Goal: Rakyat’s Well-Being

Strategy 1: The COVID-19 pandemic and public health

Strategy 2: Safeguarding the welfare of vulnerable groups

Measure 1: Improving financial assistance

Measure 2: Alleviating the rakyat’s cost of living

Measure 3: Assistance to farmers and fishermen

Strategy 3: Generating and retaining jobs

Measure 1: PenjanaKerja Incentive (hiring Incentive)

Measure 2: Reskilling and Upskilling

Measure 3: MySTEP

Measure 4: Targeted wage subsidy

Measure 5: Social protection

Strategy 4: Prioritising the inclusiveness agenda

Measure 1: Empowering the bumiputera

Measure 2: Upholding Islamic tenets

Measure 3: Enhancing the role of women

Measure 4: Community-based initiatives

Measure 5: Enhancing rural infrastructure

Measure 6: Youth and sports development

Strategy 5: Ensuring the well-being of the rakyat

Measure 1: Digital connectivity

Measure 2: Access to quality education

Measure 3: Increasing home ownership

Measure 4: Public transport

Measure 5: Defending the nation’s sovereignty and security

Second Integral Goal: Business Continuity

Strategy 1: Driving investments

Measure 1: Investment in key sectors:

Measure 2: Improving the business environment

Measure 3: Science, technology and innovation

Measure 4: Locally Manufactured Products

Strategy 2: Strengthening key sectors

Measure 1: Empowering the agriculture sector

Measure 2: Development of the commodity sector

Measure 3: Sustainability of the tourism industry

Strategy 3: Prioritising automation and digitalisation

Strategy 4: Enhancing access to financing

Measure 1: Micro credit financing

Measure 2: Loan guarantees

Measure 3: Alternative financing

Third Integral Goal: Economic Resilience

Strategy 1: Expansionary budget

Measure 1: Expenditure with a higher multiplier effect

Measure 2: Sustainability of government revenue

Strategy 2: Development agenda under the 12th Malaysia Plan

Measure 1: Transport infrastructure development

Measure 2: Balanced regional development

2 .EPF to continue the development of Kwasa Damansara, with an estimated value of MYR50bn;

3. MYR5.1bn and MYR4.5bn for Sabah and Sarawak in 2021 for building and upgrading infrastructure.

Strategy 3: Enhancing the role of GLCs and civil society

Measure 1: Alternative service delivery

Strategy 4: Ensuring resource sustainability

Measure 1: Sustainable development agenda

Measure 2: Sustainable finance

Measure 3: Environmental conservation

Strategy 5: Civil service

Measure 1: Strengthening public service delivery

Measure 2: Strengthening governance and integrity in Malaysia

Measure 3: Welfare of civil servants

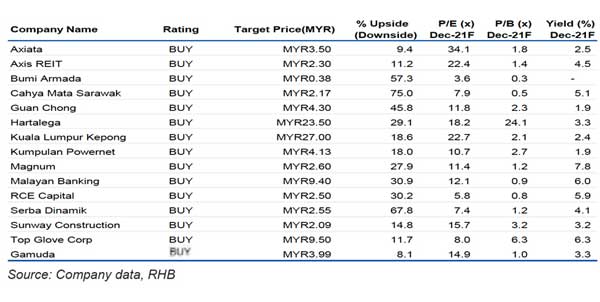

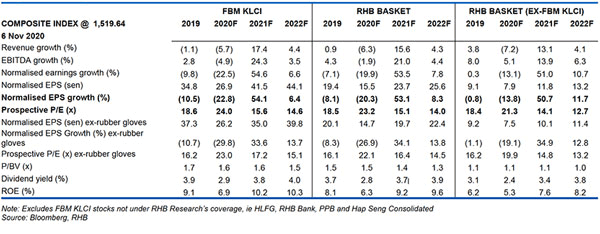

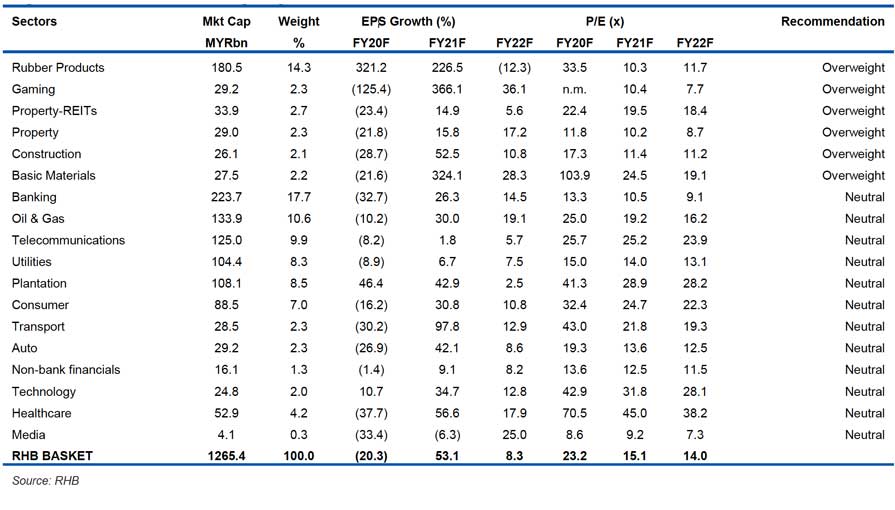

Figure 3: Earnings outlook and valuations

Sector Review

Construction – Back In The Driver’s Seat

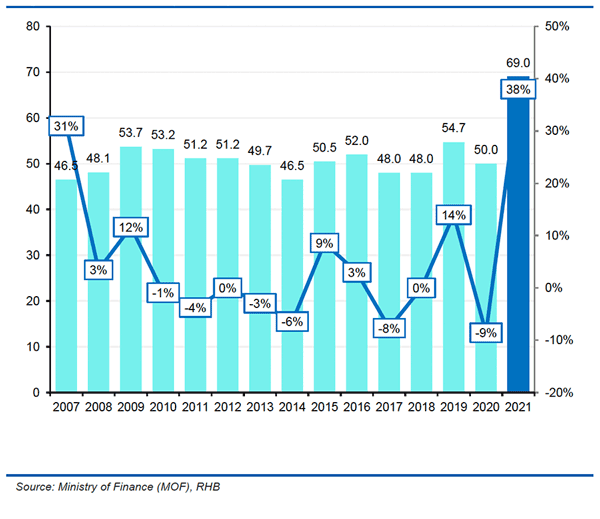

Under Budget 2021, expansionary measures are being undertaken to hasten recovery. This comes after a prolonged pandemic period, which has ravaged both the local and global economies. DE comes in to the tune of MYR69bn for 2021 – a whopping 38% YoY increase and the highest-ever figure recorded between 2007 and 2020 – from MYR50bn in 2020. The latter was revised downwards from an original estimate of MYR56bn for this year.

Out of the total amount, MYR67.3bn will be in the form of direct allocations, while another MYR1.7bn is for loans to state governments and government-linked entities. The focus is on driving the local economy back to the right direction, as well as fuelling recovery beyond the immediate term. Consequently, we expect construction to be one of the sectors that will largely benefit from the DE expansion. Opportunities from economic sub-sectors like transport is seen as encouraging, with total committed capital of MYR15bn in 2021, or 47% YoY higher when compared to 2020’s MYR10bn.

Figure 9: Planned DE (MYRbn)

The emphasis is on current ongoing projects, namely Mass Rapid Transit (MRT) Line 2, Light Rail Transit (LRT) Line 3, and the West Coast Expressway and Pan Borneo Highway. These projects were reiterated by Finance Minister Tengku Zafrul bin Tengku Abdul Aziz, given their high multiplier effects to the economy. Other projects featured in the budget include the upgrading, expansion, and maintenance of highways, roads, railways, bridges, ports, and airports. Amongst these projects are:

The construction of the Electrified Double Track Gemas-Johor Bahru;

Phase 1 of the Klang Valley Double Track;

Expansions of Kuantan Port and an airport in Sandakan;

The Johor Bahru-Singapore Rapid Transit System (RTS);

MRT Line 3 (MRT3).

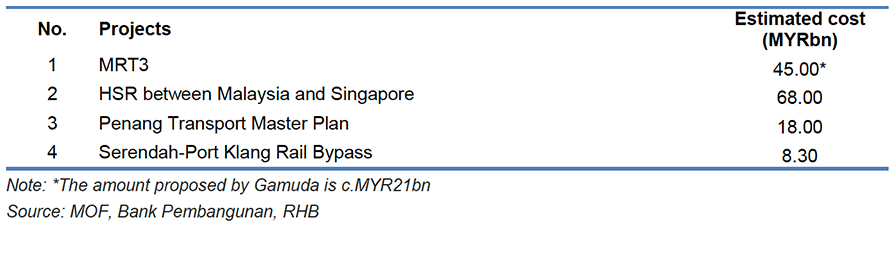

Both the RTS and MRT3 are part of the long-term development agenda under the 12th Malaysia Plan (12MP).

Setting a strong ground for local contractors... Fresh contracts of sizeable value could potentially come from the construction of the RTS, MRT3, and Bayan Lepas LRT, with estimated costs of MYR10bn, MYR45bn, and MYR8.5bn. In regards to the RTS, we expect tender submissions to begin by year’s end to allow the commencement of construction works scheduled in early 2021. Other opportunities may come from the health sub-sector, which is backed by a MYR4.7bn allocation (6.8% of total DE). Focus will be on the expansion of Malaysia’s healthcare facilities, which should lead to more new hospitals and clinics being built. Major ongoing projects under this sub-sector include the construction of the Serdang Hospital Cardiology Centre, Putrajaya Hospital Endocrine Complex, and Lawas Hospital, as well as the upgrading of the Kajang and Tawau Hospitals.

…and no one left behind. As a way to ensure that government expenditure has a high multiplier effect to the economy, we note that MYR2.5bn in total has been allocated for contractors in Classes G1 to G4 to carry out small and medium projects across the country. This includes an additional MYR200m for maintenance projects for federal roads and MYR50m for People’s Housing Project or PPR homes. In addition, the Government will extend flexibilities accorded on procurement procedures until Dec 2021 – this is to expedite the implementation of developmental projects. In addition, bumiputera contractors will also benefit from a MYR50m financing access under the Express Contract Financing Scheme or SPiKE to facilitate cash flows in implementing projects.

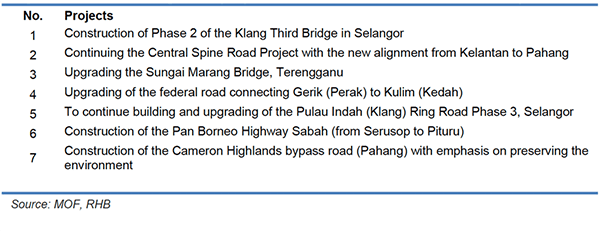

Figure 11: Several large new projects worth c. MYR3.8bn that will be implemented

Never a dull moment for East Malaysia. Sizeable allocations for East Malaysia are meant to finance rural and state developments, and cover water, electricity, and road connectivity. Both Sabah and Sarawak are allocated MYR5.1bn (2020: MYR5.2bn) and MYR4.5bn (2020: MYR4.4bn) to finance the aforementioned developments. This brings attention back to local players in these two states, such as KKB Engineering, Hock Seng Lee, and Cahya Mata Sarawak, which can benefit from federal projects – namely the Pan Borneo Highway, which runs across both states.

In Sabah, progress remains slow, however, due to a contract review exercise done in 2019. We note that more than 20 packages have yet to be awarded, leaving more opportunities for East Malaysian players to participate. Given the urgency to complete the highway stretch, we do not rule out the possibility of tender outcomes surfacing by early next year.

Other projects featured in Budget 2021 include coastal highways in Sarawak, the Baleh Hydroelectric Project, and Sarawak Water Supply Grid Programme (Phase 1). On the latter, we note that the Sarawak State Government has decided to increase the allocation for water supply projects to MYR4bn – from initial allocation of MYR2.8bn – due to its commitment to further enhance the state’s water supply system.

The passing of Budget 2021 allays multiple concerns over the sector, which hinge upon the risk of further contractions in income visibility and delays in execution. At this juncture, we believe the outlook has turned sanguine, with a higher number of major construction projects being reaffirmed by the Government. We do expect more attention to be given on execution, which should further hasten progress. This, in our view, will allow players/contractors on the ground along the logistics/economic supply chains to reap the benefits in the earliest possible period.

Large-scale projects back in the limelight. Another key event to look out for is the tabling of the 12MP in Jan 2021. Given its long-term implementation timeline, we will not be surprised to see large-scale projects being featured again, as the Government comes up with more details on their implementation. Such projects include Kuala Lumpur-Singapore High Speed Rail (HSR), Penang Transport Masterplan, and Serendah-Port Klang Rail Bypass. Total value addressable to these projects amounts to MYR139bn.

We reiterate our OVERWEIGHT call on the sector, as it is expected to rebound by 14% YoY in 2021, driven by the acceleration and revival of mega infrastructure projects, with civil engineering to continue being the main driver. Top Picks: Sunway Construction, Kerjaya Prospek, and Gamuda. Both Sunway Construction and Kerjaya Prospek offer robust earnings visibility (higher than peers) and are expected to end the year on a high note, being able as they are to achieve their internal replenishment targets.

Playing into the infrastructure theme, we like Gamuda, which has been playing key roles in the execution of mega projects and should benefit from the return of the MRT3 project. For deep value play, we prefer Gabungan AQRS in the small-/mid-cap space, as it is known for being able to benefit from the sector upcycle.

In addition, we also flag building material companies as ancillary beneficiaries of the new government-backed projects. We prefer cement players due to the industry’s harmonising supply-demand dynamics, while both West Malaysian – eg Malayan Cement and Hume Industries – and East Malaysian producers like Cahya Mata Sarawak – are seen as benefiting in unison from the balanced public expenditure allocations.

Downside risks: Longer-than-expected delays in progress works, failure to secure new orders, and an acute shortage of construction workers.

Muhammad Danial bin Abd Razak +603 9280 8682 (Construction)

muhammad.danial.abd@rhbgroup.com

Eddy Do Wey Qing +603 9280 8856 (Construction)

wey.qing.do@rhbgroup.com

Lester Siew +603 9280 2181 (Building Materials)

lester.siew@rhbgroup.com

Rubber Products: MYR400m to fight COVID-19

Windfall tax uncertainty removed

As mentioned in Budget 2021, the Big-4 gloves companies have indicated their commitment to contributing MYR400m in total to fight against COVID-19. The contribution will be used to partially cover the costs of COVID-19 vaccines and expenses for health equipment. Note

that the Big-4 gloves companies are Top Glove, Hartalega, Supermax, and Kossan. We understand that Top Glove has pledged MYR185m out of this MYR400m, with the other three gloves players we cover contributing MYR215m in total. We maintain our earnings forecasts, as we estimate ASP increases to be more than enough to cover the Big-4’s contributions. As it is, we estimate that November ASPs for nitrile gloves should have increased by 10-15%, while the likelihood of another rise in December is very high. This is given the record-high COVID-19 cases in many countries, leading to exceptionally high demand for personal protection equipment or PPEs.

In the absence of a windfall tax, we believe the news will be positive to gloves sector sentiment. Recall that in the past 3-6 months, there have been numerous rumours and speculations that a windfall tax will be implemented on the sector. With this uncertainty removed, we believe glove players’ share prices will react positively in the short term.

Alan Lim +603 9280 8890

alan.lim@rhbgroup.com

Banks – Targeted Repayment Assistance Enhanced

In Budget 2021, the Government announced that banks will enhance the Targeted Repayment Assistance or TRA to B40 borrowers who are Bantuan Sara Hidup or Bantuan Prihatin Rakyat recipients, and micro enterprises with loans of up to MYR150,000. Borrowers in this category will be given the following options:

Option 1: A moratorium on their instalments for a period of three months;

Option 2: Reduce their monthly repayments by 50% for a period of six months.

Eligible borrowers will only need to contact their banks to choose their options and complete the necessary documentation.

For M40 borrowers, the application process for repayment assistance will be simplified. Borrowers will only need to make a self-declaration of a reduction in income.

Separately, Bank Negara Malaysia or BNM announced that the enhanced TRA will be available to eligible borrowers (loans not in arrears for more than 90 days) between 23 Nov 2020 and 30 Jun 2021. The facility for the B40 and M40 will commence in Dec 2020.

We view the enhanced TRA for B40 borrowers and micro enterprises positively. These segments have been hard hit by the pandemic and should benefit from further financial assistance. Our channel checks following the end of automatic moratorium on 30 Sep revealed that most banks were focused on getting the TRA applications approved, with borrowers allowed to submit supporting documents later.

With the enhanced TRA, loans under relief programmes that have declined substantially post 30 Sep will likely edge up again from early 2021. Potential modification losses arising from a further 3-month moratorium should be small, as interest charges will continue to accrue rather than waived, in our view. We maintain our NEUTRAL rating for the sector.

NBFIs – Good Intentions Matter

As proposed in Budget 2021, there are two initiatives by the Government related to the insurance and takaful sectors, namely the EPF Account 2 withdrawals and the MYR50.00 Perlindungan Tenang Voucher (PTV) programme.

Firstly, EPF members will be allowed to withdraw from EPF Account 2 for the purchase of life and critical illness insurance and takaful products approved by the fund for themselves and their family members. While the withdrawal amount has yet to be decided, the goal is to increase the country’s insurance penetration rate.

We deem this initiative a positive to the sector, as it could raise the awareness of insurance and takaful products and potentially drive the demand over the long term as well. Having said that, we do not expect this initiative to immediately result in any meaningful pick-up in demand, as life and critical illness insurance and takaful products are, after all, discretionary in nature. We believe those who can afford paying the premiums – ie the middle income, mass affluent, and affluent segments of society – will not need the additional financial aid from Account 2.

All B40 aid recipients will be given a MYR50.00 voucher as financial aid to purchase Perlindungan Tenang products, such as life takaful and personal accident under the PTV programme. At the same time, the Government will also extend the stamp duty exemption period on all Perlindungan Tenang products with an annual premium or contribution value not exceeding MYR100.00 for another five years.

We view this initiative as more “social” than “financial”, as it clearly benefits only the B40 segment. Given the small ticket size, we do not foresee this initiative to be a meaningful topline driver for the insurance and takaful sectors.

Fiona Leong +603 9280 8886

fiona.leong@rhbgroup.com

Liew Wai Hoong +603 9280 8859

liew.wai.hoong@rhbgroup.com

Consumer – The Usual Winner

Unsurprisingly, yet another consumer-friendly budget. The proposed measures – including cash handouts and bonuses for civil servants – should effectively lend support to consumer spending. In addition, increased tax reliefs, tax cuts, and lower EPF contributions should translate into higher disposable income – hence, aid to contain inflationary pressures,particularly within the lower-income group. This should benefit consumer staple companies, including Nestle, QL Resources, Power Root, and NTPM.

Meanwhile, the new facility to withdraw EPF savings from Account 1 on a targeted basis (for those who lost their jobs) and other various initiatives to generate and retain jobs would likely soothe the overall consumer sentiment amidst the COVID-19 pandemic. This, in our view, will help consumer discretionary- or retail-based firms, including Aeon Co (M), Padini, and Berjaya Food, which are currently facing challenging times.

Essentially, the Government aims to improve its revenue collection strategy by addressing the smuggling of high duty goods. Hence, various measures have been proposed, with an eye to curb the rampant illicit trade in the tobacco market. Additionally, the imposition of excise duties on devices of new generation cigarettes and consumable liquids may imply the forthcoming of a proper regulatory framework for such new-generation products. Therefore, we believe the legal tobacco industry and British American Tobacco Malaysia should stand to gain from the abovementioned measures. This is as legal TIV has been diminishing, given the unfair competition from illicit and unregulated new-generation cigarettes.

All in all, we are nominally positive on Budget 2021. We maintain NEUTRAL on the sector, in anticipation of resilient consumer spending – but current valuations are not compelling. Our Top Picks include Power Root, Padini, Heineken Malaysia, and NTPM.

Soong Wei Siang +603 9280 8865

soong.wei.siang@rhbgroup.com

Plantation – Incentives for local labour hires

The main initiatives in Budget 2021 that affect the plantation industry include:

For sectors that are highly reliant on foreign workers such as construction and plantations, a special incentive of 60% of monthly wages will be provided. Here, 40% will be channelled to the employer, while 20% will be channelled as a wage top-up to the local worker replacing the foreign worker. This incentive will be in effect for a period of six months;

A government grant, split into MYR20m to encourage planters to obtain Malaysian Sustainable Palm Oil (MSPO) certification, and MYR30m to encourage the industry’s investments in mechanisation and automation;

Providing an inventive of MYR16m to encourage latex production; and

Under the 12th Malaysia Plan, to provide a revolving fund of MYR500m for the Forest Plantation Development Loan Programme. The funds are for the development of forest plantations of 4ha and above.

Overall, we believe Budget 2021 is relatively neutral for the plantation industry. Incentives to reduce the reliance on foreign workers are not new, and are unlikely to have much of an impact. This incentive to hire locals instead of foreign workers may work more for other sectors like industrial and manufacturing, but is not really suitable for plantations – where the bulk of the work is considered hard labour, involving hours of work in the field.

The grant to encourage planters to achieve MSPO certification is not extremely significant, but could help some smallholders achieve the nation’s 100% certification target faster.

Lastly, the revolving fund of MYR500m for forest plantation would be positive for timber players that have commitments to develop forest plantations, and who would be able to apply for the grant. We estimate that the MYR500m would enable approximately 125,000ha of forest plantations to be developed. Currently, the Sarawak State Government has a target of cultivating 1m ha of forest plantations by 2025, of which only about 420,000ha has been planted as at early 2020.

Overall, we believe Budget 2021 should have a net neutral impact on the sector. We make no changes to our NEUTRAL sector call.

Hoe Lee Leng, +603 9280 8860

hoe.lee.leng@rhbgroup.com

Property: Stamp duty waiver for another five years

In Budget 2021, the Government proposed the following measures:

Full stamp duty exemption on instruments of transfer and loan agreements for firsttime home buyers is now extended to 31 Dec 2025. The limit of the stamp duty waiver for the first residential property is also raised to MYR500,000 (from MYR300,000). This is effective for sale-and-purchase agreements executed from 1 Jan 2021 to 31 Dec 2025;

Stamp duty exemptions on loan agreements and instruments of transfer given to rescuing contractors and the original house purchasers are extended for another five years. This exemption is effective for loan agreements and instruments of transfer executed from 1 Jan 2021 to 31 Dec 2025, for abandoned housing projects certified by the Ministry of Housing & Local Government or KPKT;

A total of MYR1.2bn will be allocated to build low-cost housing under Program Perumahan Rakyat, Rumah Mesra Rakyat by Syarikat Perumahan Nasional, Malaysia Civil Servants Housing Programme or PPAM and maintain low-cost and medium-low stratified housing;

The Government will collaborate with selected financial institutions to provide a rent-to-own (RTO) scheme, to be implemented until 2022 involving 5,000 PR1MA houses worth >MYR1bn and reserved for first-time home buyers.

The extension of the stamp duty waiver for first-time home buyers for another five years is only mildly positive/neutral to the property sector. As the country is now fighting the COVID-19 pandemic, we think buyers for properties priced MYR500,000 and below are typically the mid- to low-income group – which will be very likely to hold back on buying real estate due to the uncertain economic outlook and rising concerns on job security.

Meanwhile, the RTO scheme is already ongoing, and may now be extended to PR1MA houses. Therefore, the direct impact to developers should be rather minimal. Currently, in order to unwind their unsold inventory and boost sales for new launches, developers already have their existing marketing schemes in place.

We are rather disappointed that Budget 2021 offers very few benefits for the property sector. We previously thought that the real property gains tax could be adjusted for both locals and foreigners, so that buying activities can be stimulated – given the current ultra-low interest rate. The stamp duty waiver will not likely spur demand, as property buyers can already enjoy the same benefit under the existing Home Ownership Campaign, which will end on 31 May 2021. Given the lack of positive catalysts as well as the resurgence of COVID-19 cases in Malaysia, we downgrade the property sector to NEUTRAL. Our Top Picks remain Mah Sing and Sime Darby Property.

Loong Kok Wen, CFA +603 9280 8861

loong.kok.wen@rhbgroup.com

Telecommunications: B40 goodies

8m individuals under the B40 category will be eligible to receive MYR180.00 in telecommunication credit – a one-off benefit – each (totalling MYR1.5bn) in 1Q21. This can be used to pay for internet/data subscriptions, or to defray the cost of purchasing a handset. The telcos will also provide matching benefits in the form of products or services (including data) valued at MYR1.5bn. We are generally positive on the budget goodies. The one-off credit works out to MYR15.00 per month, which is about a third to one-half of the prices of entry-level postpaid/prepaid monthly subscriptions, and about one-fifth of the prices of entrylevel fixed/fibre broadband (FBB) plans in the market. This should go some way in alleviating the pressure faced by the price-sensitive segment (prepaid users), due to the pandemic. We believe this could also incentivise the B40 segment to switch from narrowband to broadband, and/or trade-up to higher-value FBB/mobile data plans. Further details of the credit scheme will be announced in due course by industry players.

The MYR500m allocation to improve connectivity in 430 schools nationwide in 2021, and MYR7.4bn to expand broadband services/coverage in 2021-2022 are part of the MYR21bn National Digitalisation Infrastructure Plan (NDIP/JENDELA) announced by the Government earlier. This will be funded by the Universal Service Provisioning (USP) fund, which is administered by the Malaysian Communications & Multimedia Commission (MCMC). Key beneficiaries are the telcos and telco-infrastructure-based companies such as OCK Group, Redtone, and Binacom.

Jeffrey Tan, +603 9280 8863

jeffrey.tan@rhbgroup.com

RHB Guide to Investment Ratings

Buy: Share price may exceed 10% over the next 12 months

Trading Buy: Share price may exceed 15% over the next 3 months, however longerterm outlook remains uncertain

Neutral: Share price may fall within the range of +/- 10% over the next 12 months

Take Profit: Target price has been attained. Look to accumulate at lower levels

Sell: Share price may fall by more than 10% over the next 12 months

Not Rated: Stock is not within regular research coverage

Investment Research Disclaimers

RHB has issued this report for information purposes only. This report is intended for circulation amongst RHB and its affiliates’ clients generally or such persons as may be deemed eligible by RHB to receive this report and does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. This report is not intended, and should not under any circumstances be construed as, an offer or a solicitation of an offer to buy or sell the securities referred to herein or any related financial instruments.

This report may further consist of, whether in whole or in part, summaries, research, compilations, extracts or analysis that has been prepared by RHB’s strategic, joint venture and/or business partners. No representation or warranty (express or implied) is given as to the accuracy or completeness of such information and accordingly investors should make their own informed decisions before relying on the same.

This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to the applicable laws or regulations. By accepting this report, the recipient hereof (i) represents and warrants that it is lawfully able to receive this document under the laws and regulations of the jurisdiction in which it is located or other applicable laws and (ii) acknowledges and agrees to be bound by the limitations contained herein. Any failure to comply with these limitations may constitute a violation of applicable laws.

All the information contained herein is based upon publicly available information and has been obtained from sources that RHB believes to be reliable and correct at the time of issue of this report. However, such sources have not been independently verified by RHB and/or its affiliates and this report does not purport to contain all information that a prospective investor may require. The opinions expressed herein are RHB’s present opinions only and are subject to change without prior notice. RHB is not under any obligation to update or keep current the information and opinions expressed herein or to provide the recipient with access to any additional information. Consequently, RHB does not guarantee, represent or warrant, expressly or impliedly, as to the adequacy, accuracy, reliability, fairness or completeness of the information and opinion contained in this report. Neither RHB (including its officers, directors, associates, connected parties, and/or employees) nor does any of its agents accept any liability for any direct, indirect or consequential losses, loss of profits and/or damages that may arise from the use or reliance of this research report and/or further communications given in relation to this report. Any such responsibility or liability is hereby expressly disclaimed.

Whilst every effort is made to ensure that statement of facts made in this report are accurate, all estimates, projections, forecasts, expressions of opinion and other subjective judgments contained in this report are based on assumptions considered to be reasonable and must not be construed as a representation that the matters referred to therein will occur. Different assumptions by RHB or any other source may yield substantially different results and recommendations contained on one type of research product may differ from recommendations contained in other types of research. The performance of currencies may affect the value of, or income from, the securities or any other financial instruments referenced in this report. Holders of depositary receipts backed by the securities discussed in this report assume currency risk. Past performance is not a guide to future performance. Income from investments may fluctuate. The price or value of the investments to which this report relates, either directly or indirectly, may fall or rise against the interest of investors.

This report does not purport to be comprehensive or to contain all the information that a prospective investor may need in order to make an investment decision. The recipient of this report is making its own independent assessment and decisions regarding any securities or financial instruments referenced herein. Any investment discussed or recommended in this report may be unsuitable for an investor depending on the investor’s specific investment objectives and financial position. The material in this report is general information intended for recipients who understand the risks of investing in financial instruments. This report does not take into account whether an investment or course of action and any associated risks are suitable for the recipient. Any recommendations contained in this report must therefore not be relied upon as investment advice based on the recipient's personal circumstances. Investors should make their own independent evaluation of the information contained herein, consider their own investment objective, financial situation and particular needs and seek their own financial, business, legal, tax and other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report.

This report may contain forward-looking statements which are often but not always identified by the use of words such as “believe”, “estimate”, “intend” and “expect” and statements that an event or result “may”, “will” or “might” occur or be achieved and other similar expressions. Such forward-looking statements are based on assumptions made and information currently available to RHB and are subject to known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievement to be materially different from any future results, performance or achievement, expressed or implied by such forward-looking statements. Caution should be taken with respect to such statements and recipients of this report should not place undue reliance on any such forward-looking statements. RHB expressly disclaims any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or circumstances after the date of this publication or to reflect the occurrence of unanticipated events.

The use of any website to access this report electronically is done at the recipient’s own risk, and it is the recipient’s sole responsibility to take precautions to ensure that it is free from viruses or other items of a destructive nature. This report may also provide the addresses of, or contain hyperlinks to, websites. RHB takes no responsibility for the content contained therein. Such addresses or hyperlinks (including addresses or hyperlinks to RHB own website material) are provided solely for the recipient’s convenience. The information and the content of the linked site do not in any way form part of this report. Accessing such website or following such link through the report or RHB website shall be at the recipient’s own risk.

This report may contain information obtained from third parties. Third party content providers do not guarantee the accuracy, completeness, timeliness or availability of any information and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such content. Third party content providers give no express or implied warranties, including, but not limited to, any warranties of merchantability or fitness for a particular purpose or use. Third party content providers shall not be liable for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including lost income or profits and opportunity costs) in connection with any use of their content.

The research analysts responsible for the production of this report hereby certifies that the views expressed herein accurately and exclusively reflect his or her personal views and opinions about any and all of the issuers or securities analysed in this report and were prepared independently and autonomously. The research analysts that authored this report are precluded by RHB in all circumstances from trading in the securities or other financial instruments referenced in the report, or from having an interest in the company(ies) that they cover.

The contents of this report is strictly confidential and may not be copied, reproduced, published, distributed, transmitted or passed, in whole or in part, to any other person without the prior express written consent of RHB and/or its affiliates. This report has been delivered to RHB and its affiliates’ clients for information purposes only and upon the express understanding that such parties will use it only for the purposes set forth above. By electing to view or accepting a copy of this report, the recipients have agreed that they will not print, copy, videotape, record, hyperlink, download, or otherwise attempt to reproduce or re-transmit (in any form including hard copy or electronic distribution format) the contents of this report. RHB and/or its affiliates accepts no liability whatsoever for the actions of third parties in this respect.

The contents of this report are subject to copyright. Please refer to Restrictions on Distribution below for information regarding the distributors of this report. Recipients must not reproduce or disseminate any content or findings of this report without the express permission of RHB and the distributors.

The securities mentioned in this publication may not be eligible for sale in some states or countries or certain categories of investors. The recipient of this report should have regard to the laws of the recipient’s place of domicile when contemplating transactions in the securities or other financial instruments referred to herein. The securities discussed in this report may not have been registered in such jurisdiction. Without prejudice to the foregoing, the recipient is to note that additional disclaimers, warnings or qualifications may apply based on geographical location of the person or entity receiving this report.

The term “RHB” shall denote, where appropriate, the relevant entity distributing or disseminating the report in the particular jurisdiction referenced below, or, in every other case, RHB Investment Bank Berhad and its affiliates, subsidiaries and related companies.

RESTRICTIONS ON DISTRIBUTIONThis report is issued and distributed in Malaysia by RHB Investment Bank Berhad (“RHBIB”). The views and opinions in this report are our own as of the date hereof and is subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. RHBIB has no obligation to update its opinion or the information in this report.

ThailandThis report is issued and distributed in the Kingdom of Thailand by RHB Securities (Thailand) PCL, a licensed securities company that is authorised by the Ministry of Finance, regulated by the Securities and Exchange Commission of Thailand and is a member of the Stock Exchange of Thailand. The Thai Institute of Directors Association has disclosed the Corporate Governance Report of Thai Listed Companies made pursuant to the policy of the Securities and Exchange Commission of Thailand. RHB Securities (Thailand) PCL does not endorse, confirm nor certify the result of the Corporate Governance Report of Thai Listed Companies

IndonesiaThis report is issued and distributed in Indonesia by PT RHB Sekuritas Indonesia. This research does not constitute an offering document and it should not be construed as an offer of securities in Indonesia. Any securities offered or sold, directly or indirectly, in Indonesia or to any Indonesian citizen or corporation (wherever located) or to any Indonesian resident in a manner which constitutes a public offering under Indonesian laws and regulations must comply with the prevailing Indonesian laws and regulations.

SingaporeThis report is issued and distributed in Singapore by RHB Bank Berhad (Singapore branch) which is a holder of a full bank licence and an exempt capital markets services licence and financial adviser regulated by the Monetary Authority of Singapore. RHB Bank Berhad (Singapore branch) may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, RHB Bank Berhad (Singapore branch) accepts legal responsibility for the contents of the report to such persons

This report was prepared by RHB and is being distributed solely and directly to “major” U.S. institutional investors as defined under, and pursuant to, the requirements of Rule 15a-6 under the U.S. Securities and Exchange Act of 1934, as amended (the “Exchange Act”). Accordingly, access to this report via Bursa Marketplace or any other Electronic Services Provider is not intended for any party other than “major” US institutional investors, nor shall be deemed as solicitation by RHB in any manner. RHB is not registered as a broker-dealer in the United States and does not offer brokerage services to U.S. persons. Any order for the purchase or sale of the securities discussed herein that are listed on Bursa Malaysia Securities Berhad must be placed with and through Auerbach Grayson (“AG”). Any order for the purchase or sale of all other securities discussed herein must be placed with and through such other registered U.S. broker-dealer as appointed by RHB from time to time as required by the Exchange Act Rule 15a-6. This report is confidential and not intended for distribution to, or use by, persons other than the recipient and its employees, agents and advisors, as applicable. Additionally, where research is distributed via Electronic Service Provider, the analysts whose names appear in this report are not registered or qualified as research analysts in the United States and are not associated persons of Auerbach Grayson AG or such other registered U.S. broker-dealer as appointed by RHB from time to time and therefore may not be subject to any applicable restrictions under Financial Industry Regulatory Authority (“FINRA”) rules on communications with a subject company, public appearances and personal trading. Investing in any non-U.S. securities or related financial instruments discussed in this research report may present certain risks. The securities of non-U.S. issuers may not be registered with, or be subject to the regulations of, the U.S. Securities and Exchange Commission. Information on non-U.S. securities or related financial instruments may be limited. Foreign companies may not be subject to audit and reporting standards and regulatory requirements comparable to those in the United States. The financial instruments discussed in this report may not be suitable for all investors. Transactions in foreign markets may be subject to regulations that differ from or offer less protection than those in the United States.

DISCLOSURE OF CONFLICTS OF INTEREST

RHB Investment Bank Berhad, its subsidiaries (including its regional offices) and associated companies, (“RHBIB Group”) form a diversified financial group, undertaking various investment banking activities which include, amongst others, underwriting, securities trading, market making and corporate finance advisory.

As a result of the same, in the ordinary course of its business, any member of the RHBIB Group, may, from time to time, have business relationships with, hold any positions in the securities and/or capital market products (including but not limited to shares, warrants, and/or derivatives), trade or otherwise effect transactions for its own account or the account of its customers or perform and/or solicit investment, advisory or other services from any of the subject company(ies) covered in this research report.

While the RHBIB Group will ensure that there are sufficient information barriers and internal controls in place where necessary, to prevent/manage any conflicts of interest to ensure the independence of this report, investors should also be aware that such conflict of interest may exist in view of the investment banking activities undertaken by the RHBIB Group as mentioned above and should exercise their own judgement before making any investment decisions.

In Singapore, investment research activities are conducted under RHB Bank Berhad (Singapore branch), and the disclaimers above similarly apply.

Save as disclosed in the following link RHB Research conflict disclosures – November 2020 and to the best of our knowledge, RHBIB hereby declares that:

RHBIB does not have a financial interest in the securities or other capital market products of the subject company(ies) covered in this report.

RHBIB is not a market maker in the securities or capital market products of the subject company(ies) covered in this report.

None of RHBIB’s staff or associated person serve as a director or board member* of the subject company(ies) covered in this report.

*For the avoidance of doubt, the confirmation is only limited to the staff of research department

RHBIB did not receive compensation for investment banking or corporate finance services from the subject company in the past 12 months.

RHBIB did not receive compensation or benefit (including gift and special cost arrangement e.g. company/issuer-sponsored and paid trip) in relation to the production of this report.

Save as disclosed in the following link RHB Research conflict disclosures – November 2020 and to the best of our knowledge, RHB Securities (Thailand) PCL hereby declares that:

RHB Securities (Thailand) PCL does not have a financial interest in the securities or other capital market products of the subject company(ies) covered in this report.

RHB Securities (Thailand) PCL is not a market maker in the securities or capital market products of the subject company(ies) covered in this report.

None of RHB Securities (Thailand) PCL’s staff or associated person serve as a director or board member* of the subject company(ies) covered in this report.

*For the avoidance of doubt, the confirmation is only limited to the staff of research department

RHB Securities (Thailand) PCL did not receive compensation for investment banking or corporate finance services from the subject company in the past 12 months.

RHB Securities (Thailand) PCL did not receive compensation or benefit (including gift and special cost arrangement e.g. company/issuer-sponsored and paid trip) in relation to the production of this report.

Save as disclosed in the following link RHB Research conflict disclosures – November 2020 and to the best of our knowledge, RHB Securities (Thailand) PCL hereby declares that:

PT RHB Sekuritas Indonesia and its investment analysts, does not have any interest in the securities of the subject company(ies) covered in this report. For the avoidance of doubt, interest in securities include the following:

Managing or jointly with other parties managing such parties as referred to in(a), (b) or (c) above.

PT RHB Sekuritas Indonesia is not a market maker in the securities or capital market products of the subject company(ies) covered in this report.

None of PT RHB Sekuritas Indonesia’s staff** or associated person serve as a director or board member* of the subject company(ies) covered in this report.

PT RHB Sekuritas Indonesia did not receive compensation for investment banking or corporate finance services from the subject company in the past 12 months.

PT RHB Sekuritas Indonesia** did not receive compensation or benefit (including gift and special cost arrangement e.g. company/issuer-sponsored and paid trip) in relation to the production of this report:

Notes: *The overall disclosure is limited to information pertaining to PT RHB Sekuritas Indonesia only.

**The disclosure is limited to Research staff of PT RHB Sekuritas Indonesia only.

Save as disclosed in the following link RHB Research conflict disclosures – November 2020 and to the best of our knowledge, the Singapore Research department of RHB Bank Berhad (Singapore branch) hereby declares that:

RHB Bank Berhad, its subsidiaries and/or associated companies do not make a market in any issuer covered by the Singapore research analysts in this report.

RHB Bank Berhad, its subsidiaries and/or its associated companies and its analysts do not have a financial interest (including a shareholding of 1% or more) in the issuer covered by the Singapore research analysts in this report.

RHB Bank Berhad’s Singapore research staff or connected persons do not serve on the board or trustee positions of the issuer covered by the Singapore research analysts in this report.

RHB Bank Berhad, its subsidiaries and/or its associated companies do not have and have not within the last 12 months had any corporate finance advisory relationship with the issuer covered by the Singapore research analysts in this report or any other relationship that may create a potential conflict of interest.

RHB Bank Berhad’s Singapore research analysts, or person associated or connected to it do not have any interest in the acquisition or disposal of, the securities, specified securities based derivatives contracts or units in a collective investment scheme covered by the Singapore research analysts in this report.

RHB Bank Berhad’s Singapore research analysts do not receive any compensation or benefit in connection with the production of this research report or recommendation on the issuer covered by the Singapore research analysts.

The analyst(s) who prepared this report, and their associates hereby, certify that: (1) they do not have any financial interest in the securities or other capital market products of the subject companies mentioned in this report, except for:

Get in touch with RHB Premier today.

This publication has been prepared by RHB Bank Berhad and is solely for your information only. It may not be copied, published, circulated, reproduced or distributed in whole or part to any person without the prior written consent of RHB Bank Berhad. In preparing this article, RHB Bank Berhad has relied upon and assumed the accuracy and completeness of all information available from public references and articles or which was otherwise reviewed by RHB Bank Berhad. Accordingly, whilst we have taken all reasonable care to ensure that the information contained in this article is not untrue or misleading at the time of publication, we cannot guarantee its accuracy or completeness or fairness of such opinions and make no representation or warranty (whether expressed or implied) and accept no responsibility or liability for its accuracy or completeness. You should not act on the information contained in this article without first independently verifying its contents.

Any opinion, historical account, personal profile, estimate or data contained in this article is based on information available as of the date of this article and are subject to change without notice. It does not constitute any advice, offer or solicitation by RHB Bank Berhad. This document and its contents are not intended to constitute an offer for sale and/or invitation to subscribe for or purchase or otherwise acquire any of the instruments referred to herein.

Disclaimer for Video and Podcast by RHB Asset Management:The podcast provided herein is solely for information purposes only. It does not take into account the specific investment objectives, financial situations or particular needs of any particular person.

This podcast does not constitute an offer, solicitation or recommendation to buy or sell or subscribe for any security or financial instrument or to enter into any transaction or to participate in any particular trading or investment strategy. Information contained in the podcast should not be relied upon when making investment decisions. You should seek independent legal or tax advice before making any investment decisions. Investments are subject to investment risks, including the possible loss of the principal amount invested. Value of the investments and the income, if any, may fall or rise.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein and it should not be relied upon as such. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance.

Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same. RHBAM does not guarantee that all risks associated to the transactions mentioned herein have been identified, nor does it provide advice as to whether you should enter into any such transaction. The contents hereof may not be reproduced or disseminated in whole or in part without RHBAM’s written consent.

This podcast has not been reviewed by the Securities Commission Malaysia. You should not act on the information contained in this podcast without first independently verifying its contents.

Disclaimer for Video and Podcast by Economics and Market Strategy:This report is prepared for information purposes only by the Economics and Market Strategy division within RHB Bank Berhad and/or its subsidiaries related companies and affiliates, as applicable (“RHB”). All research is based on material compiled from data considered to be reliable at the time of writing, but RHB does not make any representation or warranty, express or implied, as to its accuracy, completeness or correctness.

Neither this report, nor any opinion expressed herein, should be construed as an offer to sell or a solicitation of an offer to acquire any securities or financial instruments mentioned herein. RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for any direct or consequential loss arising from the use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without prior consent of RHB and RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for the actions of third parties in this respect. Recipients are reminded that the financial circumstances surrounding any company or any market covered in the reports may change since the time of their publication. The contents of this report are also subject to change without any notification.

This report does not purport to be comprehensive or to contain all the information that a prospective investor may need in order to make an investment decision. The recipient of this report is making its own independent assessment and decisions regarding any securities or financial instruments referenced herein. Any investment discussed or recommended in this report may be unsuitable for an investor depending on the investor’s specific investment objectives and financial position. The material in this report is general information intended for recipients who understand the risks of investing in financial instruments. This report does not take into account whether an investment or course of action and any associated risks are suitable for the recipient. Any recommendations contained in this report must therefore not be relied upon as investment advice based on the recipient's personal circumstances. Investors should make their own independent evaluation of the information contained herein, consider their own investment objective, financial situation and particular needs and seek their own financial, business, legal, tax and other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report.

RHB (including its respective directors, associates, connected parties and/or employees) may own or have positions in securities or financial instruments of the company(ies) covered in this research report or any securities or financial instruments related thereto, and may from time to time add to, or dispose off, or may be materially interested in any such securities or financial instruments. Further, RHB does and seeks to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities or financial instruments of such company(ies), may sell them or buy them from customers on a principal basis and may also perform or seek to perform significant banking, advisory or underwriting services for or relating to such company(ies), as well as solicit such banking, advisory or other services from any entity mentioned in this research report.

RHB (including its respective directors, associates, connected parties and/or employees) do not accept any liability, be it directly, indirectly or consequential losses, loss of profits or damages that may arise from any reliance based on this report or further communication given in relation to this report, including where such losses, loss of profits or damages are alleged to have arisen due to the contents of such report or communication being perceived as defamatory in nature.

This podcast has not been reviewed by the Securities Commission (SC) and/or Bank Negara Malaysia (BNM).

RHB Bank Berhad 196501000373 (6171-M)