Quarterly Market Outlook

From the 2nd century BCE to the 18th century, China’s Silk Road was a network of trade routes connecting East and West, playing a central role in the economic, political, cultural and religious interactions between the two hemispheres. Today, there is the New Silk Road, revived in the form of the Belt and Road Initiative.

With China firmly on its way to becoming the world’s top economic powerhouse through the New Silk Road, investors will want to get in on the action. China’s economic weight as the world’s largest trading power and manufacturer places it in a significant position, and the country is expected to overtake the US by 20281.

Its Belt and Road Initiative, adopted in 2013, will invest in 70 countries and promote global economic cooperation. As the country grows from an emerging market to an advanced economy, there is a substantial demand for Chinese equities, particularly A-shares, H-shares and American Depository Receipts (ADRs).

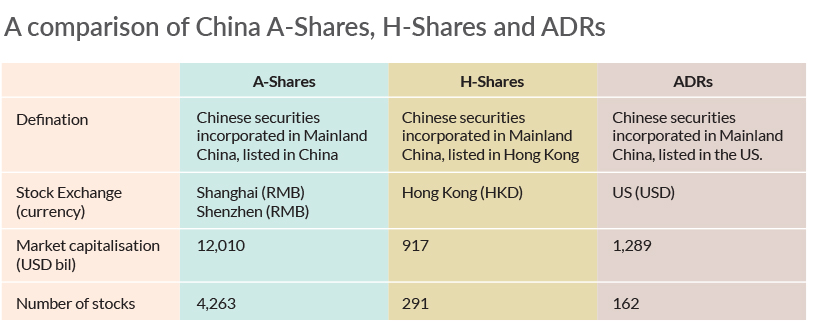

China A-shares are the stock shares of mainland China-based companies that trade on the two Chinese stock exchanges, the Shanghai Stock Exchange (SSE) and the Shenzhen Stock Exchange (SZSE). A-shares are also known as domestic shares because they use the Chinese renminbi (RMB) for valuation. Previously, due to China’s restrictions on foreign investment, China A-shares were only available for purchase by mainland citizens. However, since 2003, selected foreign institutions have been able to participate in A-shares trading through the Qualified Foreign Institutional Investor (QFII) system. This exclusivity is what sets it apart from other categories.

Chinese H-shares represent the shares of Chinese companies trading on the Hong Kong Stock Exchange. These are issued in China under Chinese regulation and are subject to the Hong Kong Stock Exchange’s listing requirements.

ADRs are stocks of larger Chinese companies that are listed on US stock exchanges, such as Alibaba, Baidu, and Weibo.

In terms of total market capitalisation and number of stocks, onshore equities (A-shares) outnumber those available offshore (B-share and H-shares). Investing in A-shares would give you direct access to these companies. The Chinese equity market is one of the largest in the world in terms of market capitalisation, and A-shares cover all the sectors that are the new economic drivers for China over the next decade, such as healthcare, consumer products, and tech.

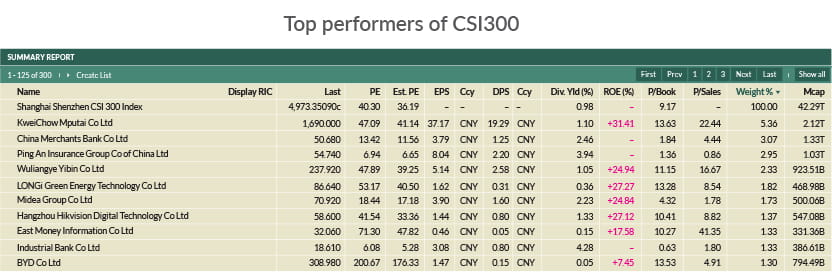

The CSI300 index tracks the performance of the top 300 A-share stocks listed on the Shanghai or Shenzhen stock exchanges.

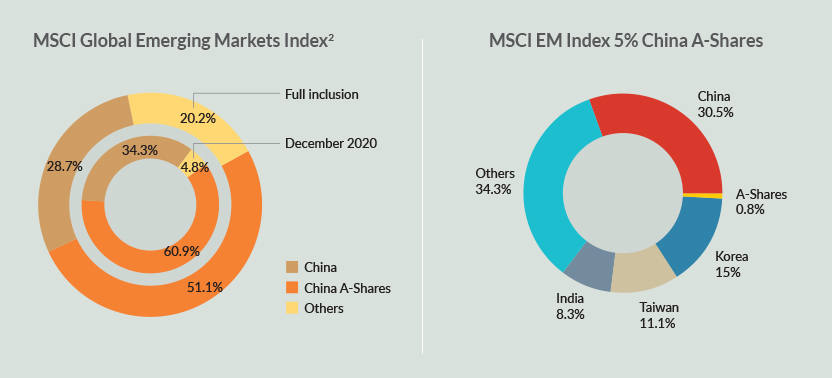

In June 2017, the MSCI Emerging Markets Index announced a two-phase plan in which it would gradually add 222 China A large-cap stocks, in phases. In May 2018, the index began to partially include China large-cap A shares, which make up 5% of the index. Full inclusion of Chinese equities would exceed 40% of the index.

To increase accessibility, the Shenzhen-Hong Kong Stock Connect is a cross-boundary investment channel that connects the Shenzhen and Hong Kong stock exchanges. Investors on each side can trade shares on the other market through their local brokers and clearing houses. Similarly, the Shanghai-Hong Kong Stock Connect links investors on either side.

You might ask, why not just invest in Chinese offshore equities? Offshore Chinese equities, which currently make up more than 50% of the MSCI China All Shares Index, are part of international capital markets. These shares tend to move in tandem with other shares that trade outside China and so are more exposed to currency fluctuations and global economic conditions, compared to A-shares which are largely isolated.

To illustrate this point, here’s a comparison of the five-year performance of the Shanghai Shenzhen CSI300 index vs the Hang Seng China Enterprises Index (HSCEI), the latter of which includes H-shares, red-chips (stocks with a sizable stake owned by the Chinese government) and private enterprises.

One of the constituents of the CSI300, Kweichou Moutai, has seen its share price increase 234.7% over the past five years, and it forecast annual earnings growth is 14.5% over the next three years.

China’s journey to becoming a global superpower is based on a two-pronged growth strategy: strengthening its domestic economy with a focus on the digital economy; and growing and sustaining its influence on regional trade with its regional counterparts.

As part of the growth strategy, China has continued to liberalise and reform its capital markets to attract more foreign asset managers and financial institutions. Despite China being the second largest market globally in terms of capitalisation value, China A-shares have remained a well-kept secret in global portfolios, making up only a small allocation. While China A-shares are underrepresented, there is also a low correlation to other equity markets, providing diversification benefits.

The China A-share space is more retail investor oriented, compared to markets like the US or even Malaysia, where institutional investors are more dominant. This creates more level playing field suited to active strategies. Here is where you can make the most of your opportunities.

Source: Wind, Goldman Sachs Global Investment Research, as at end January 2021

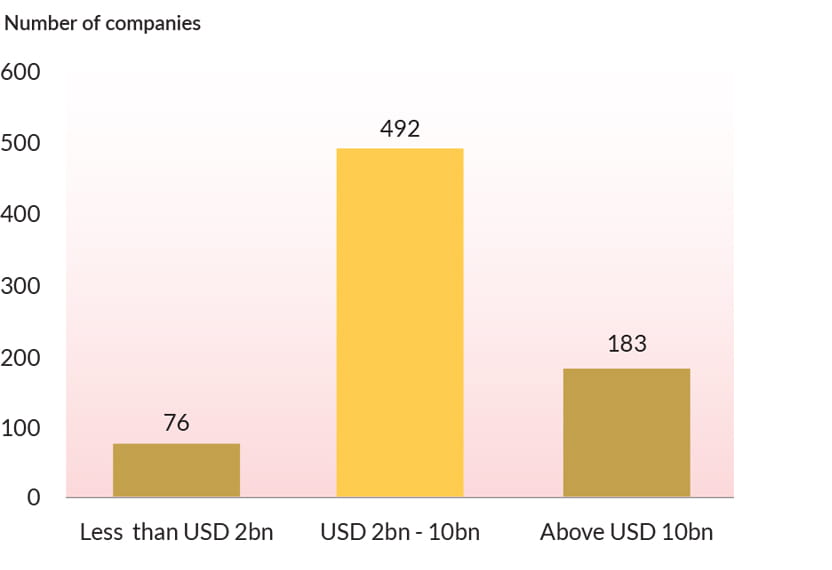

Zooming in on the equities market, we unveil a rising superstar: mid-sized companies. Mid-caps represent a larger part of the onshore investment universe, compared to offshore. A larger pool of mid-caps means more opportunities for investors to spot the outperformers.

An example of a potential outperformer in the mid-cap segment is Desay SV, a company that makes advanced driver assistance systems. This company will likely benefit from the increasing adoption of smart technology for automobiles. It isn’t a small fish, either. Desay currently has a market cap of US$6.7 bil. China is currently the largest market for EVs, with 41% of the global share2. With carmakers set to launch more EV models over the next few years, companies like Desay are set to reap the benefits.

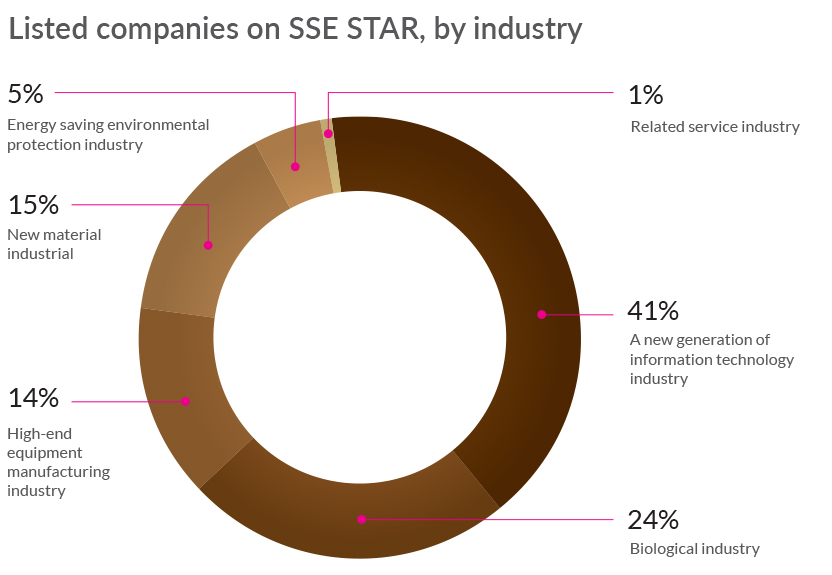

Besides EV and smart vehicle technology, the mid-cap segment is a hotbed for innovation in other tech-related areas. Launched in 2019, the SSE’s STAR Market, also known as the SSE Science and Technology Innovation Board, is the equivalent of New York’s NASDEQ and has allowed more capital to pour into the tech space, making up 47% of capital raised through the exchange.

Source: CICC, July 2020

For the first part of China’s growth strategy, the fast and wide reach of 5G will accelerate development of the digital economy. As all the telcos in China are state-owned, adoption of 5G technology across all networks has been rapid. There are already 792,000 5G base stations across the country, with a target of 1.39 million by the end of 2021. China is forecast to reach 739 million 5G subscribers by 2025, according to a recent study by ABI Research3.

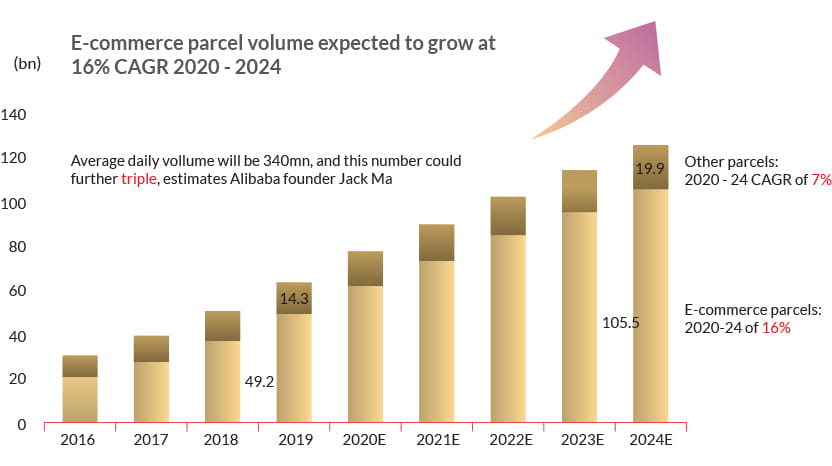

The pandemic has fuelled online activities and boosted delivery demand. Within the logistics sector, premium express delivery players will soon outpace their peers. In the chart below, we can see that e-commerce parcel volume is expected to grow at 16% CAGR from 2020-2024.

Source: CICC Research, Sept 2020

The Covid-19 outbreak has also resulted in travel restrictions, so the Chinese government is encouraging more domestic spending in an effort to repatriate consumption. This leaves plenty of room for growth among domestic manufacturers, retailers and service providers as consumers turn to local alternatives.

In the second part of the growth strategy, the Regional Comprehensive Economic Partnership (RCEP) will open the doors for China to develop closer trade ties with Asean countries in lower value-added manufactured goods, while it enhances cooperation with Japan and South Korea in high-end manufacturing. The RCEP is the world’s largest trade agreement, covering 15 countries that collectively contribute 29% of global GDP. The aim of the agreement is the strengthen regional integration against the backdrop of deglobalisation.

RHB China A Fund (“Fund”) provides the opportunity to participate in the rise of China onshore equities and ride along the Belt and Road initiative, while diversifying your portfolio in an investment that has a low correlation to global indices.

The Fund invests 95% of its net assets value in USD denominated share class of Schroder International Selection Fund China A (“Target Fund”), with the balance in liquid assets including money market instruments, placements of cash in any deposits or investment accounts with any financial institution(s)that are not embedded with or linked to financial derivative instruments (“Deposits”) and collective investment schemes investing in money market instruments and Deposits. This Fund is suited to investors with an aggressive risk profile.

The Target Fund’s investment manager, Schroders Investment Management (Hong Kong) Limited, has a proven long-term track record. The Target Fund aims to achieve sustainable and long-term capital growth, investing not less than 70% of its net assets in Chinese equities.

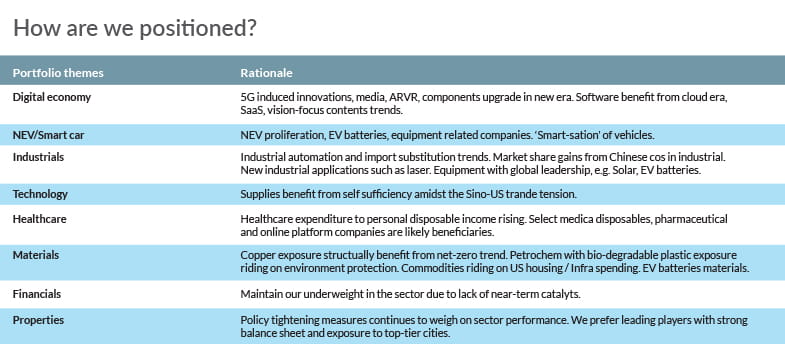

Given the extensive depth and breadth of the China A-share universe (>3,300 stocks), active management is key in sourcing opportunities beyond the top benchmark names. The Target Fund investment team leverages on Schroders’ data scientists to provide a conviction ‘edge’ to investment decisions. The Target Fund manager actively manage the Target Fund to overweight themes which has growth prospect while underweight areas where lacking of growth catalyst.

Source: Schroders, as of May 2021. Sectors shown above are for illustration purposes only. This is not intended to be relied upon as a forecast, research or investment advice and is not a recommendation, offer or solicitation to buy or sell any investments or to adopt any investment strategy. Investment involves risks and investor should conduct their own assessment before investing and seek professional advice, where necessary

1https://www.msci.com/msci-china-a-inclusion

2https://theconversation.com/what-electric-vehicle-manufacturers-can-learn-from-china-their-biggest-market-161536

3https://www.rcrwireless.com/20210423/5g/china-mobile-adds-15-million-5g-subscribers-march

Get in touch with RHB Premier today.

This publication has been prepared by RHB Bank Berhad and is solely for your information only. It may not be copied, published, circulated, reproduced or distributed in whole or part to any person without the prior written consent of RHB Bank Berhad. In preparing this article, RHB Bank Berhad has relied upon and assumed the accuracy and completeness of all information available from public references and articles or which was otherwise reviewed by RHB Bank Berhad. Accordingly, whilst we have taken all reasonable care to ensure that the information contained in this article is not untrue or misleading at the time of publication, we cannot guarantee its accuracy or completeness or fairness of such opinions and make no representation or warranty (whether expressed or implied) and accept no responsibility or liability for its accuracy or completeness. You should not act on the information contained in this article without first independently verifying its contents.

Any opinion, historical account, personal profile, estimate or data contained in this article is based on information available as of the date of this article and are subject to change without notice. It does not constitute any advice, offer or solicitation by RHB Bank Berhad. This document and its contents are not intended to constitute an offer for sale and/or invitation to subscribe for or purchase or otherwise acquire any of the instruments referred to herein.

Disclaimer for Video and Podcast by RHB Asset Management:The podcast provided herein is solely for information purposes only. It does not take into account the specific investment objectives, financial situations or particular needs of any particular person.

This podcast does not constitute an offer, solicitation or recommendation to buy or sell or subscribe for any security or financial instrument or to enter into any transaction or to participate in any particular trading or investment strategy. Information contained in the podcast should not be relied upon when making investment decisions. You should seek independent legal or tax advice before making any investment decisions. Investments are subject to investment risks, including the possible loss of the principal amount invested. Value of the investments and the income, if any, may fall or rise.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein and it should not be relied upon as such. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance.

Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same. RHBAM does not guarantee that all risks associated to the transactions mentioned herein have been identified, nor does it provide advice as to whether you should enter into any such transaction. The contents hereof may not be reproduced or disseminated in whole or in part without RHBAM’s written consent.

This podcast has not been reviewed by the Securities Commission Malaysia. You should not act on the information contained in this podcast without first independently verifying its contents.

Disclaimer for Video and Podcast by Economics and Market Strategy:This report is prepared for information purposes only by the Economics and Market Strategy division within RHB Bank Berhad and/or its subsidiaries related companies and affiliates, as applicable (“RHB”). All research is based on material compiled from data considered to be reliable at the time of writing, but RHB does not make any representation or warranty, express or implied, as to its accuracy, completeness or correctness.

Neither this report, nor any opinion expressed herein, should be construed as an offer to sell or a solicitation of an offer to acquire any securities or financial instruments mentioned herein. RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for any direct or consequential loss arising from the use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without prior consent of RHB and RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for the actions of third parties in this respect. Recipients are reminded that the financial circumstances surrounding any company or any market covered in the reports may change since the time of their publication. The contents of this report are also subject to change without any notification.

This report does not purport to be comprehensive or to contain all the information that a prospective investor may need in order to make an investment decision. The recipient of this report is making its own independent assessment and decisions regarding any securities or financial instruments referenced herein. Any investment discussed or recommended in this report may be unsuitable for an investor depending on the investor’s specific investment objectives and financial position. The material in this report is general information intended for recipients who understand the risks of investing in financial instruments. This report does not take into account whether an investment or course of action and any associated risks are suitable for the recipient. Any recommendations contained in this report must therefore not be relied upon as investment advice based on the recipient's personal circumstances. Investors should make their own independent evaluation of the information contained herein, consider their own investment objective, financial situation and particular needs and seek their own financial, business, legal, tax and other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report.

RHB (including its respective directors, associates, connected parties and/or employees) may own or have positions in securities or financial instruments of the company(ies) covered in this research report or any securities or financial instruments related thereto, and may from time to time add to, or dispose off, or may be materially interested in any such securities or financial instruments. Further, RHB does and seeks to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities or financial instruments of such company(ies), may sell them or buy them from customers on a principal basis and may also perform or seek to perform significant banking, advisory or underwriting services for or relating to such company(ies), as well as solicit such banking, advisory or other services from any entity mentioned in this research report.

RHB (including its respective directors, associates, connected parties and/or employees) do not accept any liability, be it directly, indirectly or consequential losses, loss of profits or damages that may arise from any reliance based on this report or further communication given in relation to this report, including where such losses, loss of profits or damages are alleged to have arisen due to the contents of such report or communication being perceived as defamatory in nature.

This podcast has not been reviewed by the Securities Commission (SC) and/or Bank Negara Malaysia (BNM).

RHB Bank Berhad 196501000373 (6171-M)