The Smart Side of Leveraging: Borrowing to Build Assets, Not Just Buy Them

Most people use leverage to buy assets. Sophisticated investors may also use it to build wealth more strategically by balancing opportunity, liquidity and risk.

We encounter leverage long before we even hear the term. We aren’t even aware of how closely it’s tied to necessities or major life milestones. It’s just part of modern life. A student loan pays for our studies. We get a car loan as soon as we start our first job, and that helps with mobility and career growth. A home loan helps us buy a property years before we can fully afford it in cash. A business loan gets us started on the entrepreneurship path. Even a credit card, when used responsibly, offers convenience and short-term cash flow management.

Leverage is often misunderstood because it draws a mental picture of reckless borrowing and financial crises. Yet in reality, leverage itself is neutral. In fact, the word “leverage” means using available resources to achieve something greater.

As we progress in life and our wealth grows, the conversation around leverage changes. It’s no longer about leveraging to afford, but how capital can be used more efficiently. That shift is where investment leverage enters the picture.

For experienced investors, leverage is not about stretching beyond their current means. In many cases, it is about balancing liquidity, opportunity and long-term portfolio strategy. They recognise that leverage, when used with discipline, can be a valuable wealth-building tool. It can help them participate in opportunities earlier and potentially improve long-term capital efficiency.

Sophisticated investors have long understood this distinction. Many high-net-worth investors do not necessarily deploy all their available cash into a single investment at once. Instead, they think about:

- preserving liquidity

- maintaining flexibility

- diversifying exposure

- managing opportunity cost

For example, an investor with substantial available cash may still choose to finance part of an investment portfolio rather than use up all their cash. This allows them to remain invested while retaining liquidity for business needs, emergencies or future opportunities.

This is sometimes referred to as capital efficiency. In simple terms, it means making your capital work harder without tying all of it up in one place.

Understanding investment leverage

Investment leverage means using financing to increase investment exposure. Rather than investing solely with personal cash, an investor combines personal capital with financing to access a larger portfolio position.

The idea is straightforward: if the investment generates returns meaningfully above financing cost, leverage may improve returns on the investor’s own capital.

However, leverage also magnifies downside outcomes. If investments perform poorly, financing costs still apply and losses may become larger relative to the investor’s original capital. A useful analogy is a magnifying glass. It can enlarge the effectiveness of a sound investment plan, but it can also magnify mistakes and emotional decision-making.

This is why leverage is best understood as a tool, and not a shortcut.

Experienced investors understand this clearly. They do not treat leverage as “free money”. Instead, they evaluate:

- financing cost,

- liquidity needs,

- downside scenarios,

- and portfolio resilience before increasing exposure.

How to fit investment leverage into wealth planning

For some investors, financing can become part of a broader portfolio strategy rather than simply a borrowing tool. For example, RHB Bank Berhad’s Wealth Leveraging solution functions as an overdraft-based financing solution linked to investment activity.

The process typically works like this:

- The investor contributes part of the investment capital.

- The Bank provides financing based on the approved Margin of Finance.

- The investment assets are pledged as collateral.

- Interest is charged only on the utilised financing amount.

The amount of financing available depends on the risk profile of the collateral. Generally, lower-risk collateral may allow a higher financing percentage, while higher-risk investments may require larger investor participation.

It’s important to remember that financing does not eliminate risk. Financing costs may change over time, and investment returns are never guaranteed.

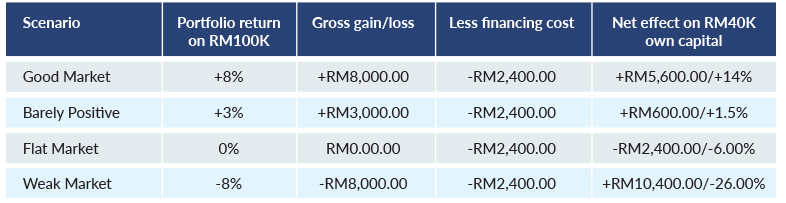

Here’s a simple example of how leverage changes outcomes:

- An investor uses RM40,000 of their own capital, topping up with RM60,000 to get an investment exposure of RM100,000.

- Financing on the RM60,000 costs 4% p.a., or RM2,400 per year.

Let’s explore the possible outcomes based on how the market performs.

In a good market, the financed amount may improve the investor’s return on their own capital. Applying it to the scenario here, an 8% gain on the RM100,000 invested results in a stronger return on the investor’s own RM40,000 capital.

In a flat or negative market, the investor still has to cover the financing cost, regardless of the portfolio’s performance. This means that small gains may be reduced significantly, and losses can become larger.

If the market falls sharply, the investor may have to top up their funds, pledge additional collateral to support the financing, or repay part of the financed capital to reduce loan exposure. As a last resort, some of the pledged collateral may be sold.

The risks investors should understand

One of the biggest dangers in investing is false confidence during strong markets. When markets rise consistently, leverage can appear easy and rewarding. But market conditions eventually change.

If collateral values fall significantly, investors may face margin calls or forced selling at unfavourable prices. This is why experienced investors focus heavily on liquidity and moderation.

In practice, this means maintaining a healthy cash reserve, avoiding excessive leverage, and ensuring financing obligations are manageable even during the slower times. Leverage becomes dangerous not because of fluctuating markets, but because of a lack of financial flexibility.

Some practical rules

- Keep Leverage Moderate

As a conservative discussion starting point, some investors may choose to keep leveraged exposure relatively small compared to total net worth, unless supported by strong liquidity and risk capacity.

- Ensure Return Potential Exceeds Financing Cost

The expected investment return should meaningfully exceed borrowing cost after accounting for fees and risk buffer.

- Protect Emergency Liquidity

Investment leverage should never depend on money needed for living expenses, business operations or emergency reserves.

- Stress-Test Before Investing

Create a scenario of a portfolio declining by 10% or 20%. What would happen? If the answer is panic or strain, leverage is too high.

The real goal is better structure

The strongest investors do not treat leverage as a shortcut to wealth. Instead, they view it as one component within a broader portfolio strategy. Ultimately, the goal is not simply to borrow more, but to build a portfolio structure resilient enough to navigate both opportunity and uncertainty over time.

For investors interested in exploring market perspectives, fund ideas and portfolio planning, our Fund Discoveries Podcast and Relationship Managers can provide further guidance on product suitability and current investment opportunities.

Disclaimer:

Investors are advised to read and understand the content of the relevant documents including but not limited to prospectus or information memorandum that have been registered with the Securities Commission and Product Highlight Sheet before investing. Investors should also consider all fees and charges involved before investing. Prices of units and income distribution, if any, may go down as well as up; where past performance is no guarantee of future performance. Units will be issued upon receipt of the registration form referred to and accompanying the Prospectus. The printed copy of the prospectus and Product Highlight Sheet is available at RHB branches/Premier Centre and investors have the right to request for a Product Highlight Sheet.

This article has not been reviewed by the Securities Commission Malaysia (SC).

RHB Bank Berhad 196501000373 (6171-M)