Quarterly Market Outlook

Opting for more shariah-compliant investments may be the key to long-term wealth protection and growth. We explain why, and how you can include Shariah-compliant tools in your financial journey.

Your sofa has a giant sinkhole in the middle. It’s been there a while, but you’ve never actually done anything about it. With the Hari Raya holidays coming up, you’re going to be hosting family and friends. You don’t want to lose any small guests in that hole, so you go online to look for a new sofa. Click and purchase.

Then you remember that your washing machine doesn’t really wash anymore; it just swirls your clothes around to look busy. You might as well buy a new one. Click and purchase.

Before you know it, you’ve spent quite a decent amount. It’s too late to cancel your orders, and you need those items anyway. As soon as the holidays are over, you promise yourself that you’re going to be good and restart your wealth management journey.

But what about the inflation rate? What about the crazy economic situation? What about my retirement fund savings? Will I ever have enough? Help! Before you spiral, take a deep breath, and read on. There’s a whole world of wealth management options out there, made just for you.

In today’s market conditions, what’s the one thing we all want as investors, besides returns? Stability! When do we want it? Now!

With rising inflation squeezing the life from our precious savings, this isn’t the right time to pick the riskiest investments just so you can get higher potential gains, unless you can afford to throw caution (and money) into the wind. In the face of uncertainty and volatility of today’s market and economy, Shariah-compliant wealth management may just be the solution for those concerned about their financial future. Safeguard your financial wellbeing in this world and your spiritual wellbeing for the afterlife.

Shariah-compliant tools are for everyone regardless of religious or financial background. The label “Shariah-compliant” may seem like an intimidating term, but it really isn’t. Think of it as an approach that is the opposite of what Jordan Belfort would do. The focus is on long-term ethical and sustainable financial planning.

Shariah-compliant banking and investment tools are available at every stage of your financial journey, whether its Wealth Creation/Accumulation (Investment Products), Wealth Protection (Takaful), Wealth Purification (Social Finance Instruments), or Wealth Distribution (Succession Planning). Put them all together for a complete financial plan, as illustrated further below in this article. You can also refer to this article for more information on the Shariah-compliant wealth journey.

In Shariah-compliant wealth management, the preservation of wealth goes beyond just the literal meaning since it also encourages the generation, accumulation, and distribution of wealth in a fair and just manner. The broader scope includes empowering communities through the provision of financial solutions that create a positive impact by integrating waqf and sadaqah within the Islamic financial ecosystem.

It's important to also note that Shariah law forbids transactions that support industries or activities that bring negative social and environmental impact, such as gambling, alcohol, non-halal foods and goods, usury (interest), and excessive speculation.

Another noteworthy area is the risk-sharing element of Shariah-compliant investing tools. Transactions should promote equality, social justice and inclusion, and economic prosperity. They must demonstrate accountability, transparency, and legal protection for all parties. Sharing the risk – and reward – incentivises minimising risk and increases transparency as all parties are likely to work towards the common goal of protecting each other’s capital. You’re in it together.

Now that we’ve explained the benefits of Shariah-compliant financial tools, here’s how you can apply them to each pillar of your financial journey to get the most benefit.

Wealth Creation/Accumulation

In Islam, wealth can be accumulated through two ways: 1) your own efforts and 2) through inheritance. Your own efforts include jobs and investments in shares or other permissible instruments. It’s allowed - and even encouraged - to work hard to build a comfortable nest egg. These tools can help you save your earnings, and even put it to good use to earn a profit.

Click here to see our Shariah-compliant wealth creation/accumulation products.

Wealth Protection

Protecting the wealth you’ve accumulated is a core component of any sound financial plan. Once you’ve accumulated wealth, it’s logical to want to protect it from any unforeseen circumstances so you can rest assured that you and your loved ones can continue to benefit. At RHB Islamic, our approach to protecting your valuable assets is tailored to your needs and goals. Click here to see our Takaful products.

Wealth Purification

Purification of wealth is a key aspect of Shariah-compliant wealth management that contributes to social wellbeing and is central to creating a positive impact through social justice and equity. During the fasting month, you’ve had a lot of time to reflect on all your blessings and good fortune, and purifying your wealth is a great way to remind yourself that worldly wealth is to be shared.

Zakat, or almsgiving, is the third pillar (rukun) of Islam and is compulsory for all able Muslims. Zakat is aimed at purifying one’s wealth by donating a specified portion to benefit the community. The zakat may be channeled for the benefit of those who are qualified to receive it, known as “asnaf”.

In RHB, you can easily pay your zakat with just a few clicks through RHB Online – no need to queue up at the zakat centre! You’re also less likely to forget.

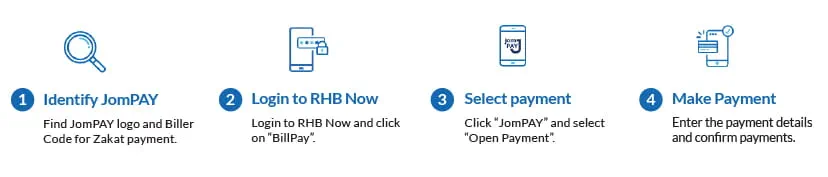

How to pay your Zakat

Follow the steps below to pay your Zakat online using JomPAY.

Wealth Distribution

The reason why we work so hard to accumulate and protect our wealth is so we can pass it on to the next generation. To avoid sticky situations and disputes that you won’t be around to resolve, it’s best to plan ahead using these Islamic wealth distribution tools. Our expert partners can assist and advise you in drawing up a comprehensive wealth plan, ensuring your needs are met and your legacy is successfully distributed in the most effective and efficient way, leaving no room for doubt.

Talk to your Relationship Manager today to create your comprehensive Shariah-compliant Wealth Management plan for your present and future.

From all of us at RHB, we wish you Selamat Hari Raya Maaf Zahir Batin!

For avoidance of doubt, RHB Islamic Bank only promotes and manages promotions in relation to RHB Islamic Bank products and its related proposition only.

Investors are advised to read and understand content of the relevant documents including but not limited to prospectus or information memorandum that has been registered with Securities Commission and Product Hsighlight Sheet before investing. Investors should also consider all fees and charges involved before investing. Prices of units and income distribution, if any, may go down as well as up; where past performance is no guarantee of future performance. Units will be issued upon receipt of the registration form referred to and accompanying the Prospectus. The printed copy of prospectus and Product Highlight Sheet is available at RHB branches/Premier Centre and investors have the right to request for a Product Highlight Sheet.

This material has not been reviewed by the Securities Commission Malaysia (SC).

RHB Islamic Bank Berhad 200501003283 (680329-V)

Get in touch with RHB Premier today.

This publication has been prepared by RHB Bank Berhad and is solely for your information only. It may not be copied, published, circulated, reproduced or distributed in whole or part to any person without the prior written consent of RHB Bank Berhad. In preparing this article, RHB Bank Berhad has relied upon and assumed the accuracy and completeness of all information available from public references and articles or which was otherwise reviewed by RHB Bank Berhad. Accordingly, whilst we have taken all reasonable care to ensure that the information contained in this article is not untrue or misleading at the time of publication, we cannot guarantee its accuracy or completeness or fairness of such opinions and make no representation or warranty (whether expressed or implied) and accept no responsibility or liability for its accuracy or completeness. You should not act on the information contained in this article without first independently verifying its contents.

Any opinion, historical account, personal profile, estimate or data contained in this article is based on information available as of the date of this article and are subject to change without notice. It does not constitute any advice, offer or solicitation by RHB Bank Berhad. This document and its contents are not intended to constitute an offer for sale and/or invitation to subscribe for or purchase or otherwise acquire any of the instruments referred to herein.

Disclaimer for Video and Podcast by RHB Asset Management:The podcast provided herein is solely for information purposes only. It does not take into account the specific investment objectives, financial situations or particular needs of any particular person.

This podcast does not constitute an offer, solicitation or recommendation to buy or sell or subscribe for any security or financial instrument or to enter into any transaction or to participate in any particular trading or investment strategy. Information contained in the podcast should not be relied upon when making investment decisions. You should seek independent legal or tax advice before making any investment decisions. Investments are subject to investment risks, including the possible loss of the principal amount invested. Value of the investments and the income, if any, may fall or rise.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein and it should not be relied upon as such. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance.

Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same. RHBAM does not guarantee that all risks associated to the transactions mentioned herein have been identified, nor does it provide advice as to whether you should enter into any such transaction. The contents hereof may not be reproduced or disseminated in whole or in part without RHBAM’s written consent.

This podcast has not been reviewed by the Securities Commission Malaysia. You should not act on the information contained in this podcast without first independently verifying its contents.

Disclaimer for Video and Podcast by Economics and Market Strategy:This report is prepared for information purposes only by the Economics and Market Strategy division within RHB Bank Berhad and/or its subsidiaries related companies and affiliates, as applicable (“RHB”). All research is based on material compiled from data considered to be reliable at the time of writing, but RHB does not make any representation or warranty, express or implied, as to its accuracy, completeness or correctness.

Neither this report, nor any opinion expressed herein, should be construed as an offer to sell or a solicitation of an offer to acquire any securities or financial instruments mentioned herein. RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for any direct or consequential loss arising from the use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without prior consent of RHB and RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for the actions of third parties in this respect. Recipients are reminded that the financial circumstances surrounding any company or any market covered in the reports may change since the time of their publication. The contents of this report are also subject to change without any notification.

This report does not purport to be comprehensive or to contain all the information that a prospective investor may need in order to make an investment decision. The recipient of this report is making its own independent assessment and decisions regarding any securities or financial instruments referenced herein. Any investment discussed or recommended in this report may be unsuitable for an investor depending on the investor’s specific investment objectives and financial position. The material in this report is general information intended for recipients who understand the risks of investing in financial instruments. This report does not take into account whether an investment or course of action and any associated risks are suitable for the recipient. Any recommendations contained in this report must therefore not be relied upon as investment advice based on the recipient's personal circumstances. Investors should make their own independent evaluation of the information contained herein, consider their own investment objective, financial situation and particular needs and seek their own financial, business, legal, tax and other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report.

RHB (including its respective directors, associates, connected parties and/or employees) may own or have positions in securities or financial instruments of the company(ies) covered in this research report or any securities or financial instruments related thereto, and may from time to time add to, or dispose off, or may be materially interested in any such securities or financial instruments. Further, RHB does and seeks to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities or financial instruments of such company(ies), may sell them or buy them from customers on a principal basis and may also perform or seek to perform significant banking, advisory or underwriting services for or relating to such company(ies), as well as solicit such banking, advisory or other services from any entity mentioned in this research report.

RHB (including its respective directors, associates, connected parties and/or employees) do not accept any liability, be it directly, indirectly or consequential losses, loss of profits or damages that may arise from any reliance based on this report or further communication given in relation to this report, including where such losses, loss of profits or damages are alleged to have arisen due to the contents of such report or communication being perceived as defamatory in nature.

This podcast has not been reviewed by the Securities Commission (SC) and/or Bank Negara Malaysia (BNM).

RHB Bank Berhad 196501000373 (6171-M)