A Divided World: Investing in an Era Where Politics Moves Markets

The world investors once understood is evolving. Globalisation is giving way to a more complex, fragmented landscape shaped by politics, national priorities, and shifting alliances. The key is learning how to navigate this changing environment.

For decades, investing followed a straightforward logic: economics led, markets followed. Growth accelerated, earnings improved, interest rates shifted, and asset prices responded accordingly. Countries focused on what they did best, supply chains stretched across continents, and capital moved freely in search of opportunity.

That environment has become more complex. Today, geopolitics is no longer a secondary consideration. It is increasingly influencing where factories are built, how supply chains are structured, where capital flows, and how investors assess risk. Trade tensions, sanctions, regional conflicts, and strategic rivalries are no longer distant headlines. They are becoming part of the investment landscape.

Read behind the headlines

Investors traditionally focus on earnings, inflation, and interest rates. Those factors remain important, but geopolitical developments can now move markets with equal speed. A new tariff can reshape an industry. Export controls can disrupt technology supply chains. Conflict in an energy-producing region can push oil prices higher and revive inflation concerns.

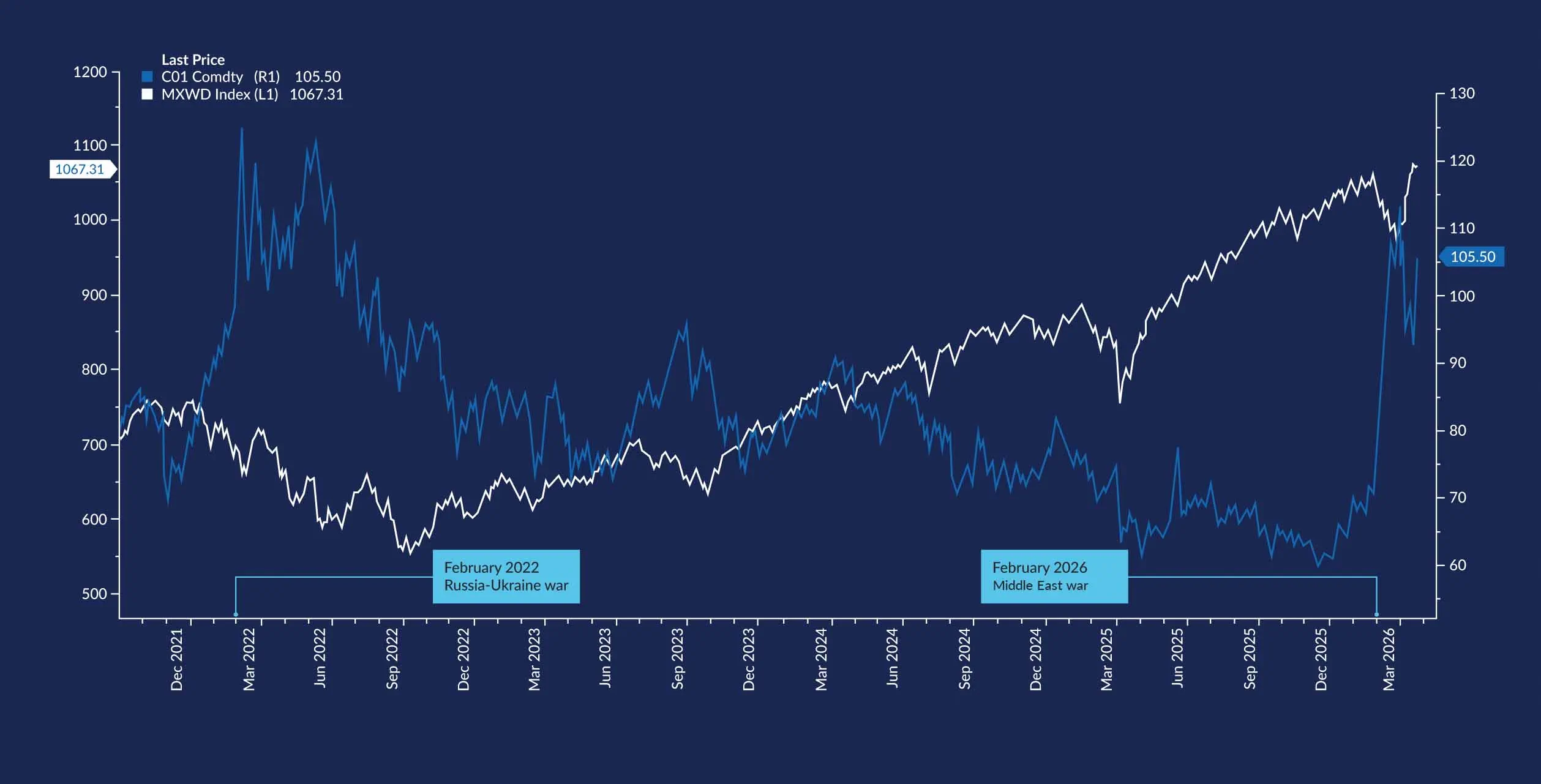

This was evident in early 2022, when Russia’s invasion of Ukraine triggered a sharp rise in energy and commodity prices. Global equities weakened, bond markets came under pressure, and sector leadership changed quickly. Energy-related companies outperformed, while many growth-oriented sectors struggled as higher inflation expectations led investors to reassess interest rate risks.

We see it again in the recent US-Iran conflict. The key lesson here? Markets don’t just respond to headlines. They respond to the economic consequences behind those headlines.

Source: Bloomberg as at 24 April 2026 from 1 October 2021 - 24 April 2026.

The highlighted periods show how major geopolitical conflicts can trigger sharp market reactions, particularly when they threaten energy supply or raise inflation concerns. In both February 2022 and February 2026, rising uncertainty was accompanied by significant moves in oil prices and shifts in investor sentiment, illustrating how geopolitics can quickly spill into financial markets.

The real impact of geopolitics

Geopolitical events often feel unprecedented in the moment, yet market reactions frequently follow a recognisable pattern.

The first phase is usually driven by uncertainty. Equities may sell off, gold often strengthens, and investors tend to rotate into defensive assets or the US dollar.

The second phase is more important. Investors begin asking whether global growth is genuinely at risk, whether oil prices are likely to remain elevated, whether central banks may need to respond, and whether company earnings are likely to be materially affected.

That reassessment often determines whether a market pullback is temporary or prolonged.

Many geopolitical sell-offs have historically proven short-lived once investors concluded that the broader economy remained resilient. Others, particularly those linked to energy shocks or inflation, have taken longer to recover.

The Russia-Ukraine conflict in 2022 stood out because it coincided with already elevated inflation and aggressive interest-rate tightening. Recovery was therefore more uneven than in many earlier geopolitical episodes.

A new investment map

Geopolitics is also reshaping where opportunities may emerge. Companies are increasingly diversifying their production bases and reducing dependence on single-country supply chains. This has brought greater investor attention to markets viewed as stable, competitive, strategically positioned, and more or less on the same political wavelength.

India is benefiting from manufacturing expansion and strong domestic demand. Across ASEAN, economies such as Malaysia, Vietnam, and Thailand are attracting interest as supply chains broaden beyond China. Malaysia remains deeply integrated into global trade. According to MATRADE (Malaysia External Trade Development Corporation), electrical and electronics (E&E) products accounted for around 40%1 of total exports in recent years, reinforcing the country’s role in regional manufacturing networks.

Geography, once seen as less relevant in a highly globalised world, is becoming an investment factor again.

Which sectors will benefit?

Periods of geopolitical stress do not affect all sectors equally. Historically, investors have often rotated towards areas seen as more resilient or better positioned for the changing environment.

For example:

- Energy may benefit when higher oil and gas prices support earnings.

- Defence and security can attract attention when governments increase spending.

- Gold and precious metals are often viewed as stores of value during uncertain times.

- Infrastructure and logistics may benefit as supply chains are rebuilt, diversified, or localised.

However, there’s a caveat. Sectors that are highly rate-sensitive or heavily dependent on complex global supply chains may experience greater volatility. This is all the more reason investors shouldn’t chase headlines. They should understand how capital repositions when risks change.

What would an experienced investor do?

Seasoned investors approach geopolitical volatility differently. Rather than asking whether they should exit markets entirely, they focus on whether anything fundamental has changed. They consider whether quality assets are being sold indiscriminately, whether portfolios have become too concentrated, and whether sufficient diversification and liquidity are in place.

That perspective can be valuable. Some of the strongest long-term opportunities have emerged when fear temporarily pushed down fundamentally sound assets alongside weaker ones.

For instance, the Russia-Ukraine conflict caused big tech shares to drop significantly, despite strong recurring enterprise revenues, high cash generation, and a dominant market position. Investors who distinguished between temporary sentiment-driven weakness and lasting fundamental damage were better positioned when these companies recovered in subsequent periods. In short: let the fundamentals speak through the noise and panic.

A Malaysian perspective

Let’s take this approach and zoom in on the Malaysian market. For Malaysian investors, the current environment presents both opportunities and risks.

Malaysia potentially stands to benefit from several structural shifts now taking place across the global economy. Supply chain diversification has encouraged multinational companies to broaden their manufacturing footprint beyond a single market, and Southeast Asia has become an increasingly important beneficiary of that trend. Malaysia’s established industrial ecosystem, skilled workforce, and strength in sectors such as electrical and electronics continue to support its relevance within regional supply chains.

Domestic opportunities may emerge in sectors linked to infrastructure, industrial parks, logistics, data centres, utilities, and selected manufacturing plays that could benefit from ongoing investment inflows. Financial institutions may also benefit over time from healthier economic activity and investment financing, while consumer-facing sectors could gain if domestic demand remains resilient.

At the same time, Malaysia remains closely tied to external demand. As a trade-oriented economy, it is still sensitive to slower global growth, weaker export markets, commodity price volatility, and shifts in investor sentiment. Developments in the United States, China, Europe, and the broader region can all influence domestic markets through trade flows, currency movements, and capital allocation trends.

On the other hand, export-oriented sectors may experience periods of volatility when global demand weakens, or geopolitical tensions disrupt trade patterns. Companies with heavy dependence on external markets or imported inputs may face margin pressure when currencies move sharply or supply chains become less efficient.

This creates a more nuanced investment backdrop, where balance is extremely important.

Rather than relying too heavily on a single sector, theme, or geography, Malaysian investors may wish to consider whether their portfolios are sufficiently diversified across domestic and international opportunities, growth, and defensive exposures, as well as income-generating assets. Exposure to structural themes such as ASEAN growth, digitalisation, healthcare, or infrastructure may complement more traditional holdings.

It may also be worth asking practical questions:

- Am I overly concentrated in one market or sector?

- Do I have enough defensive or income-oriented assets if volatility arises?

- Am I participating in long-term growth themes beyond today’s headlines?

- Is my portfolio positioned to benefit if Malaysia attracts more investment flows?

Resilience isn’t a matter of trying to pre-empt every geopolitical event. That’s impossible. It comes from owning a portfolio that can adapt as conditions change (and they will). A fund that could be a helpful addition to your portfolio is one that aims to provide consistent income, like the Principal Nasdaq Equity Premium Income Fund. Another example is the RHB Global Focused Growth Equity Fund, which gives you access to a diversified portfolio of companies across the globe, including emerging markets.

The bottom line

Investing has always been about understanding change. What’s different today is where that change is coming from. Markets are no longer shaped solely by economics. Politics, policy, and strategic competition are playing a growing role in how capital moves and how risk is priced.

This environment calls for perspective, discipline, and mindful diversification. In a divided world, investment success calls for choosing the right assets and understanding the forces that shape them.

1 Department of Statistics Malaysia; External Trade Statistics Malaysia (2023–2024).

Disclaimer:

This article is strictly for its intended recipients and should not be copied, distributed or reproduced in whole or in part, nor passed to any third party, without obtaining prior permission of RHB Bank Berhad (“RHB”).

This article has been prepared by RHB and is solely for your information only. It may not be copied, published, circulated, reproduced, or distributed in whole or part to any person without the prior written consent of RHB. In preparing this presentation, RHB has relied upon and assumed the accuracy and completeness of all information available from public sources or which was otherwise reviewed by RHB. Accordingly, whilst we have taken all reasonable care to ensure that the information contained in this presentation is not untrue or misleading at the time of publication, we cannot guarantee its accuracy or completeness and make no representation or warranty (whether expressed or implied) and accept no responsibility or liability for its accuracy or completeness. You should not act on the information contained in this podcast without first independently verifying its contents.

Any opinion, management forecast or estimate contained in this article is based on information available as the date of this article and is subject to change without notice. It does not constitute an offer or solicitation to deal in units of any RHB fund and does not have regard to the specific investment objectives, financial situation or the particular needs of any specific person who may receive this. Investors may wish to seek advice from a financial adviser/unit trust consultant before purchasing units of any funds. In the event that the investor chooses not to seek advice from a financial adviser/unit trust consultant, he should consider whether the fund in question is suitable for him. Past performance of the fund or the manager, and any economic and market trends or forecast, are not necessarily indicative of the future or likely performance of the fund or the manager. The value of units in the fund, and the income accrued to the units, if any, from the fund, may fall as well as rise.

Product Highlights Sheets (“PHS”) highlighting the key features and risks of thePrincipal Nasdaq Equity Premium Income Fund dated 21 February 2025 and RHB Global Focused Growth Equity Fund dated 28 January 2026 (“Fund”) are available and investors have the right to request for a PHS.

Investors are advised to obtain, read and understand the PHS and the contents of the Information Memorandum and its supplementary (ies) (if) (“the Information Memorandum”) before investing. The Information Memorandum has been registered with the Securities Commission Malaysia (“SC”) who takes no responsibility for its contents. The SC’s approval and authorization of the registration of the Information Memorandum should not be taken to indicate that the SC has recommended or endorsed the Fund. Amongst others, investors should consider the fees and charges involved. Investors should also note that the price of units and distributions payable, if any, may go down as well as up. Where a distribution is declared, investors are advised that following the issue of additional units/distribution, the NAV per unit will be reduced from cum distribution NAV to ex-distribution NAV. Any issue of units to which the Information Memorandum relates will only be made on receipt of a form of application referred to in the Information Memorandum. The printed copy of prospectus and Product Highlight Sheet is available at RHB branches/Premier Centre and investors have the right to request for a Product Highlight Sheet. Investors are advised that investments are subject to investment risk and that there can be no guarantee that any investment objectives will be achieved. Investors should conduct their own assessment before investing and seek professional advice, where necessary and should not make an investment decision based solely on this update.

The Manager wishes to highlight the general risks for the Principal Nasdaq Equity Premium Income Fund are Market Risk, Inflation Risk, Manager Risk, Financing Risk, Liquidity Risk, and the investment of the fund is subject to market fluctuations and its inherent risk, meaning the returns and capital for this fund is not guaranteed. The specific risks to the Principal Nasdaq Equity Premium Income Fund are Currency Risk, Target Fund Investment Manager Risk, and Country Risk. Other risks associated with investments in the Target Fund of the Principal Nasdaq Equity Premium Income Fund are Availability of investment opportunities, Balance sheet risk, Cash positions and temporary defensive positions, Collection account risk, Collateral risk, Costs of buying or selling shares risk, Counterparty risk, Currency risk, Cyber security risk, Derivative risk, Settlement risk, Short selling risk, Warrants, Dividends, Fluctuation of net asset value and market pricing risk, Indemnification obligations, Legal risk – Over-the-counter (“OTC”) derivatives, reverse repurchase transactions, securities lending and re-used collateral, Liquidity risk, Listing, Market risk, Political and/or regulatory, Risks in relation to equity securities, Particular risks of exchange traded derivative transactions, Particular risks of OTC derivative transactions, Investment in Real Estate Investment Trusts (REITs), Secondary market trading risk, Securities lending, Suspension of share dealings, Tax risk, Underperformance risk, Volcker rule, and Sustainability risk. The key risks of the RHB Global Focused Growth Equity Fund are Fund Management Risk, Liquidity Risk, Currency Risk, Country Risk, Financial Derivatives Risk, Credit and Default Risk, Interest Rate Risk, Suspension of Redemption Risk, and Distribution out of Capital Risk. The key risks of the target fund associated with the RHB Global Focused Growth Equity Fund are Conflicts of Interest Risk, Counterparty Risk, Custody Risk, Cybersecurity Risks, Environmental, Social, and Governance Risk, Operational Risk, Currency Risk, Derivatives Risk, Emerging Market Risk, Equity Risk, Sustainability Risk, Inflation Risk, Investment Fund Risk, Market Liquidity Risk, Market Risk, Geographic Concentration Risk, Hedging Risk, Small and Mid-cap Risk, Security Liquidity Risk, Style Risk, and other general risks are elaborated in the Information Memorandum/Prospectus.

This article has not been reviewed by the Securities Commission Malaysia (SC).

RHB Bank Berhad 196501000373 (6171-M)