Quarterly Market Outlook

BY RHB WEALTH RESEARCH

We live in interesting times. The rise of China challenging the US as an existing world power has resulted in a trade conflict that has caused wide-spread uncertainty in global financial markets. Arguably, this trade conflict is also driven by the large wealth and political/ideological gaps between the haves and the have-nots and between different political ideologies, according to RHB Asset Management.

History tells us that major “tipping points” in financial markets are typically difficult to predict. However, when US President Donald Trump declared the first of his many rounds of tariffs on Chinese imports in January last year, the consensus mainstream opinion was already one of concern and condemnation — that the president had just opened Pandora’s box and set the world’s two largest economies on a collision course. Their fears were realised when China retaliated shortly after-wards, sounding the horn for a lengthy and damaging trade war.

It has been nearly two years. While there were occasional breakthroughs in negotiations and, at times, it seemed like both sides were close to finding a mutually agreeable solution, most of the trade war was marked by hostile tit-for-tats resulting in a gloomy global economic outlook.

In September last year, both countries formalised tariffs on a total of US$260 billion worth of imports and, in May, after an extended period of goodwill, Trump dissipated all positive momentum by unexpectedly hiking tariffs on US$200 billion worth of Chinese goods from 10% to 25%. He also fired off a series of tweets threatening to impose tariffs of 10% on US$300 billion worth of Chinese imports, effective Sept 1.

In retaliation, China announced on Aug 23 that it would be levying new tariffs ranging from 5% to 10% on US$75 billion worth of US imports. Beijing’s new import taxes will take effect on Sept 1 and Dec 15 — the same dates Trump’s tariffs on US$300 billion in Chinese goods are slated to kick in (first tranche valued at US$112 billion) — and will include goods such as soy-beans and oil.

China will also add a 25% tariff on cars and 5% tariff on auto parts. This move triggered a furious response from Trump, who immediately retaliated by hiking tariffs on Chinese imports — the 25% imposed on the existing US$250 billion of Chinese goods will be ratcheted up to 30% from Oct 1, and the new round of tariffs on US$300 billion in goods will be taxed 15%, up from the initial 10%. What should investors expect next? A range of factors — such as the upcoming 2020 US presidential election, slowing global economic performance and political instability around the world — could play a role in shaping how the trade war and, to a larger extent, the global economy plays out for the remainder of the year.

Back in March last year, Trump infamously justified his tariff decision by bragging that trade wars are “good and easy to win”. In essence, tariffs would drive up the costs of China-produced goods to make them less competitive against US-manufactured products, which, the president argued, would bring manufacturing jobs back home, force concessions from China and “Make America Great Again”.

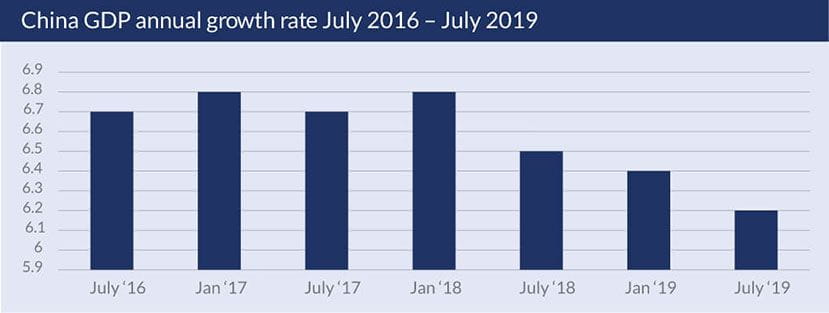

There is no denying that the figures for the first half of 2019 indicate that tariffs are causing great pain for the Chinese economy, as the country post-ed some of the lowest figures in over a decade. Gross domestic product growth dropped to a 30-year low of 6.2% while industrial output fell to a 17-year low of 4.8%. In addition, retail sales grew 7.6% year on year against an expected 8.6%, while the labour market worsened as the unemployment rate in urban areas increased to 5.3%.

The National Bureau of Statistics Purchasing Manager’s Index contract-ed for the fourth consecutive month in August to 49.5 while exports for August fell 1% year on year, with exports to the US falling 16%, marking the second largest decrease since June’s 1.3% drop.

This occurred even as the value of the renminbi declined and exporters “front-loading” US-bound shipments before the September tariffs took effect, suggesting that tariffs are probably causing a decline in external demand for Chinese exports.

However, despite the gloomy picture, the resilience of the Chinese economy and President Xi Jinping’s administration cannot be overstated. Much of it has to do with the country’s state-directed economic model that grants state-owned enterprises (SOE) and state-owned banks a significant amount of influence, as well as the government’s freedom to utilise a wide range of fiscal and monetary measures to stimulate the economy.

Furthermore, after August’s escalation in tensions, the Chinese government allowed the renminbi to fall past the key valuation level of RMB7/US dollar, even though daily fixing is on the strong end. This jolted global financial markets and drew accusations of currency manipulation by the US Treasury Department.

As we have witnessed over the course of the year, the Chinese government will not hesitate to reduce taxes and cut reserve requirement ratios (RRR) for banks to inject liquidity into the economy. For the first quarter alone, the Chinese financial system pumped a record RMB8.2 trillion worth of credit into the economy, and issued RMB1.2 trillion worth of local government bonds to spend on infrastructure projects, resulting in robust growth during the period as GDP expanded 6.4% and most major indicators trend-ed upwards.

While growth momentum halted after the stimulus eased in April, the-government has not ruled out implementing further measures if the economic conditions deteriorate, or if the trade war tensions continue to take a toll on the Chinese economy.

There is no arguing that the US economy is superior in scale and level of development. However, that does not guarantee that it will come out on top in the trade war. Contrary to Trump’s claim that the US’ strong economic position would result in an easy victory, Xi and his administration have repeatedly demonstrated the ability to strike where it hurts most.

First, while China lacks the capacity to implement sweeping, indiscriminate tariffs on all US imports—given the significantly lower amount of US imports into the country — a quick study of its tariffs list would reveal that it is intentionally targeting key pressure points of the US economy.

The latest round of Chinese tariffs saw US soybean imports taxed 33%,compared with 3% for Brazilian and Argentinian producers, while the upcoming Dec 15 tariffs will see China taxing US automobiles and car parts 42.6%, com-pared with 12.6% for German and Japanese manufacturers.

Secondly, China, with its massive consumer base, remains one of the larg-est and most attractive foreign markets for US businesses. Any change in relations between the two countries would have a huge impact on US companies.

Finally, with the 2020 presidential election looming, China is aware that Trump is desperate for a strong stock market performance to justify his economic policies to voters, especially after mounting criticism of his controversial immigration policy and setbacks in diplomatic negotiations with North Korea.

Unfortunately, 2019 is shaping up to be a very turbulent year as the US economy continues to flash warning signs of a recession. On Aug 5, the US stock markets suffered the worst day of the year after Trump reignited his trade war with China.

This, coupled with a weaker than expected US Federal Reserve interest rate cut, resulted in an inversion of the US Treasury yield curve for the first time since 2007 and sparked recession fears, given that an inverted yield curve is typically a harbinger of a recession within 18 months.

In a bid to thwart Trump’s reelection prospects, China is also purposely targeting “Rust Belt” states containing some of the president’s strongest supporters by pilling tariffs on agricultural and steel imports, resulting in high unemployment levels.

If the economy fails to improve in time and Trump’s support base continues to suffer from the effects of the trade war, there is a chance that some of these voters would change their minds, spelling trouble for the president’s al-ready shaky path to re-election.

The longer the US-China trade war drags on, the heavier the toll will be for both economies. While investors find solace that both sides are still open to negotiation, there is a chance that trade hostilities and tensions will continue to persist. As China transforms into an economic heavyweight, it will almost certainly clash with the US on a multi tude of issues outside of trade as the two countries battle for global supremacy.

In fact, we could argue that the trade war is a structural conflict between two fundamentally opposing countries and that the disputes on trade are merely a disguise for far more deeply rooted issues revolving around China’s rapid ascent as a global leader in technology and innova-tion, which would directly threaten the US’ pole position in the global hegemony.

In May, the US placed 143 entities, including Chinese tech giant and global 5G leader Huawei, on its trade blacklist, citing them as individuals and organi-sations that pose significan’t risks to US security and foreign policy.

As China has yet to issue a response, we do not know the metaphorical straw that will break the camel’s back. How-ever, we do know if a battle for tech-nological supremacy does take place, it would likely be much more intense, impactful and longer lasting than ex-isting trade conflicts.

The more pressing question is this — should we be expecting a recession in the near future? It could be argued that after close to a decade of a bull mar-ket, it is time for the market to correct. And numerous indicators such as the inversion of the Treasury yield curve, weaker housing activity, soft consumer spending, and deteriorating European economies and a lower-than-expected growth forecast for China suggest that investors should brace themselves for a bumpy ride ahead.

RHB Asset Management’s view is that, despite the current trade war conditions, the global economy will stay afloat due to the strong fundamentals of both countries, along with the fact that both leaders are aware of what is at stake domestically and would hope-fully not risk destabilising the entire global economy. However, the actual likelihood of a global recession remains a distinct possibility.

As history shows, geopolitical situations can change overnight and major financial tipping points often happen in the blink of an eye. There is always a possibility that a global recession could occur if relations between the two largest economies in the world continue to deteriorate, or if the trade war continues to drag on, or in the worst-case scenario, spirals into other areas of conflicts.

Investors should understand that the investment journey is never a smooth ride and it is in their best interests to diversify their investments via a portfolio with different asset classes. At RHB, we do have a few model portfolio to cater for different clients’ risk profiles. Through diversification of unit trust funds, clients will be able to reduce concentration risk via investments in different asset classes such as equity, fixed income and commodity. In these volatile times, RHB also offers close-ended funds such as the RHB Strategic Income Series 7. This fund has simple features with only 1½ years’ tenure and rides the underlying fund performances of a well-known global fixed income fund via Option. For more insights, consult our investment specialists by contacting a relationship manager.

Get in touch with RHB Premier today.

This publication has been prepared by RHB Bank Berhad and is solely for your information only. It may not be copied, published, circulated, reproduced or distributed in whole or part to any person without the prior written consent of RHB Bank Berhad. In preparing this article, RHB Bank Berhad has relied upon and assumed the accuracy and completeness of all information available from public references and articles or which was otherwise reviewed by RHB Bank Berhad. Accordingly, whilst we have taken all reasonable care to ensure that the information contained in this article is not untrue or misleading at the time of publication, we cannot guarantee its accuracy or completeness or fairness of such opinions and make no representation or warranty (whether expressed or implied) and accept no responsibility or liability for its accuracy or completeness. You should not act on the information contained in this article without first independently verifying its contents.

Any opinion, historical account, personal profile, estimate or data contained in this article is based on information available as of the date of this article and are subject to change without notice. It does not constitute any advice, offer or solicitation by RHB Bank Berhad. This document and its contents are not intended to constitute an offer for sale and/or invitation to subscribe for or purchase or otherwise acquire any of the instruments referred to herein.

Disclaimer for Video and Podcast by RHB Asset Management:The podcast provided herein is solely for information purposes only. It does not take into account the specific investment objectives, financial situations or particular needs of any particular person.

This podcast does not constitute an offer, solicitation or recommendation to buy or sell or subscribe for any security or financial instrument or to enter into any transaction or to participate in any particular trading or investment strategy. Information contained in the podcast should not be relied upon when making investment decisions. You should seek independent legal or tax advice before making any investment decisions. Investments are subject to investment risks, including the possible loss of the principal amount invested. Value of the investments and the income, if any, may fall or rise.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein and it should not be relied upon as such. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance.

Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same. RHBAM does not guarantee that all risks associated to the transactions mentioned herein have been identified, nor does it provide advice as to whether you should enter into any such transaction. The contents hereof may not be reproduced or disseminated in whole or in part without RHBAM’s written consent.

This podcast has not been reviewed by the Securities Commission Malaysia. You should not act on the information contained in this podcast without first independently verifying its contents.

Disclaimer for Video and Podcast by Economics and Market Strategy:This report is prepared for information purposes only by the Economics and Market Strategy division within RHB Bank Berhad and/or its subsidiaries related companies and affiliates, as applicable (“RHB”). All research is based on material compiled from data considered to be reliable at the time of writing, but RHB does not make any representation or warranty, express or implied, as to its accuracy, completeness or correctness.

Neither this report, nor any opinion expressed herein, should be construed as an offer to sell or a solicitation of an offer to acquire any securities or financial instruments mentioned herein. RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for any direct or consequential loss arising from the use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without prior consent of RHB and RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for the actions of third parties in this respect. Recipients are reminded that the financial circumstances surrounding any company or any market covered in the reports may change since the time of their publication. The contents of this report are also subject to change without any notification.

This report does not purport to be comprehensive or to contain all the information that a prospective investor may need in order to make an investment decision. The recipient of this report is making its own independent assessment and decisions regarding any securities or financial instruments referenced herein. Any investment discussed or recommended in this report may be unsuitable for an investor depending on the investor’s specific investment objectives and financial position. The material in this report is general information intended for recipients who understand the risks of investing in financial instruments. This report does not take into account whether an investment or course of action and any associated risks are suitable for the recipient. Any recommendations contained in this report must therefore not be relied upon as investment advice based on the recipient's personal circumstances. Investors should make their own independent evaluation of the information contained herein, consider their own investment objective, financial situation and particular needs and seek their own financial, business, legal, tax and other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report.

RHB (including its respective directors, associates, connected parties and/or employees) may own or have positions in securities or financial instruments of the company(ies) covered in this research report or any securities or financial instruments related thereto, and may from time to time add to, or dispose off, or may be materially interested in any such securities or financial instruments. Further, RHB does and seeks to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities or financial instruments of such company(ies), may sell them or buy them from customers on a principal basis and may also perform or seek to perform significant banking, advisory or underwriting services for or relating to such company(ies), as well as solicit such banking, advisory or other services from any entity mentioned in this research report.

RHB (including its respective directors, associates, connected parties and/or employees) do not accept any liability, be it directly, indirectly or consequential losses, loss of profits or damages that may arise from any reliance based on this report or further communication given in relation to this report, including where such losses, loss of profits or damages are alleged to have arisen due to the contents of such report or communication being perceived as defamatory in nature.

This podcast has not been reviewed by the Securities Commission (SC) and/or Bank Negara Malaysia (BNM).

RHB Bank Berhad 196501000373 (6171-M)