Quarterly Market Outlook

BY RHB WEALTH RESEARCH

Real estate investment trusts (REITs) have been performing well in many parts of the world, especially in recent months. This is mainly due to the sharp fall in interest rates globally, stemming from the slowdown in economic growth and the trade war between the US and China that have sent investor monies flowing into relatively high-yielding and defensive sectors.

The Bloomberg World REIT Index, which is a capitalisation-weighted index of the leading REIT stocks around the world, hit an all-timehigh last month. As at Sept 2, it was at 167.72 points, up 20% from 139.68 points at the start of this year. The MSCI World Equity REIT Index hit 1217.31 points on the same day, a level that is close to its ten-year high reached on Aug 30.

RHB Wealth Research team says REITs are expected to continue their outperformance moving forward as the slowing global economic growth and the US-China trade war persist.

The team points out that the slowing economic growth is already being reflected in decisions of several central banks to lower interest rates in recent months. The US Federal Reserve (Fed) cut its interest rate by 0.25% in July this year, its first rate cut in a decade. Last month, central banks in India, Thailand and New Zealand followed suit, furthering a global trend of monetary easing policy. In Malaysia, Bank Negara Malaysia cut its overnight policy rate (OPR) to 3% and several local banks expect the rate to be lowered by another 25 basis points by the end of this year.

The team adds that these actions resulted in a low interest rate environment that would benefit REITs, which offer investors relatively attractive yields.

Meanwhile, there is no end in sight for the US-China trade war and it might go on for a prolonged period of time. Other political events such as Hong Kong’s ongoing civil unrest and the uncertainties surrounding Brexit will also continue to weigh on markets, says the team.

“The durability and stability of the sector’s cash flow will continue to provide investors with attractive dividend yields that should grow in line with the sector’s earnings. This sector represents a strong opportunity for income-oriented and risk-averse investors.”

While several REIT indexes are close to their multi-year highs, the team says REITs’ valuations are not expensive as many in various countries are still traded at a discount to their net asset values. The supply and demand in the REIT sector also remains relatively balanced, underpinned by a still-growing global economy.

One way investors can capture this opportunity is to invest in the Manulife Shariah Global REIT Fund. Launched in March, it is the first Shariah REIT fund in the world that invests in REITs only and is made available to retail investors with a minimum investment amount of RM1,000.

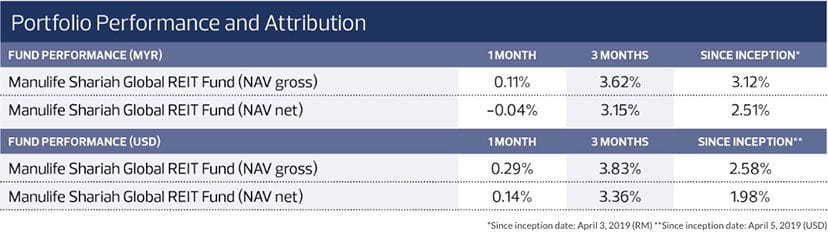

As at July 31, the fund, which aims to provide regular income and capital appreciation returns to investors, has generated a net return of 3.62% (before deducting sales and annual management charges). It has also generated a return of 3.15% since its inception in March.

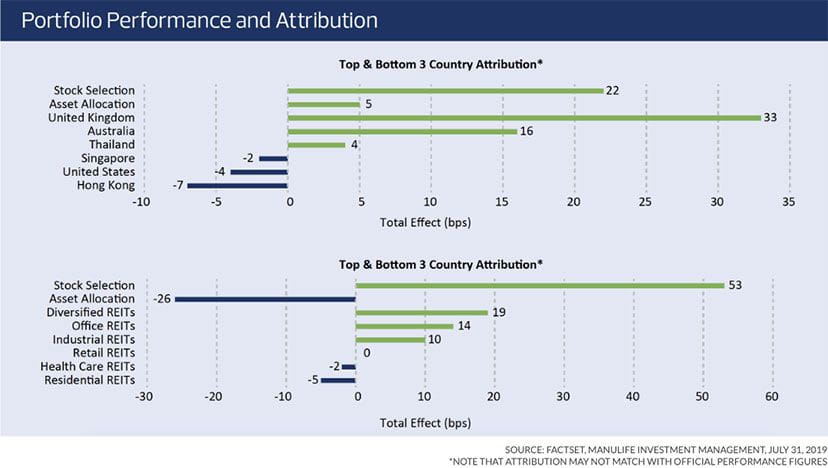

Going forward, the team says the fund favours REITs that invest in data centres and industrial properties that are expected to benefit from the growing big data and e-commerce trend.

The team says more defensive sub-sectors such as healthcare and residential properties within certain regions are also deemed attractive due to an increased uncertainty within the broader market.

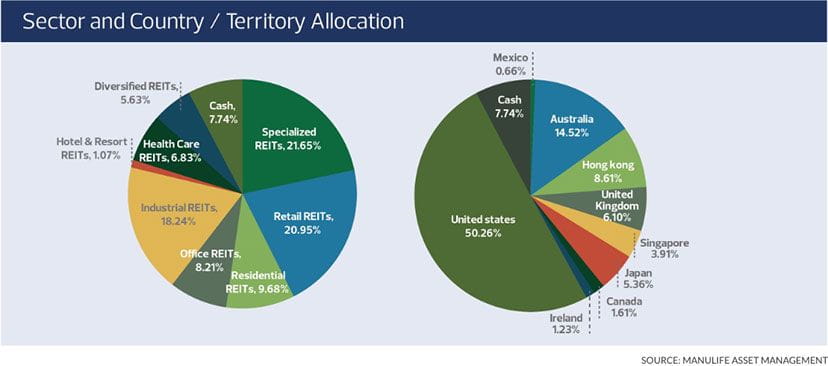

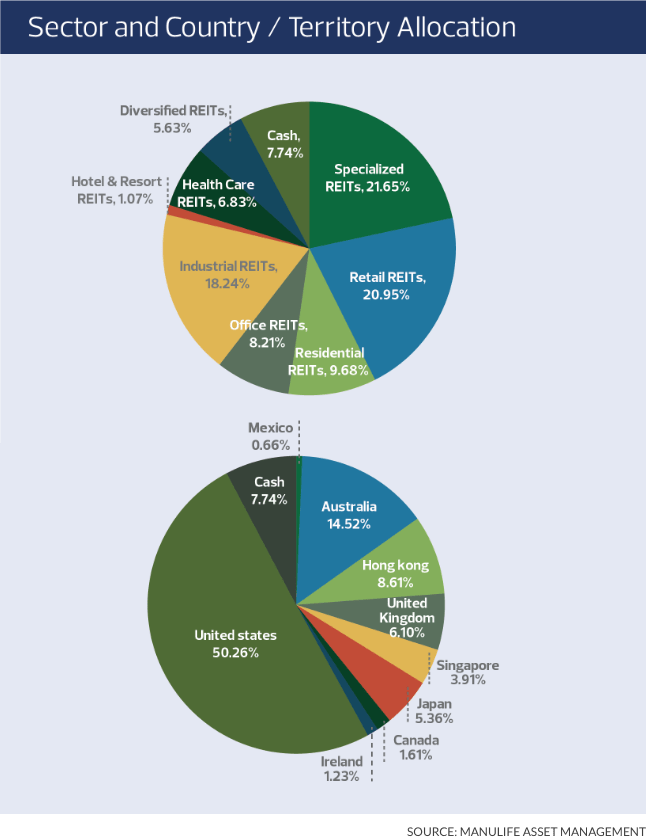

Country-wise, the fund favours the US as its economy remains healthy and its technology and telecommunication sector is developing faster than many other countries around the world. As at July, the fund had 50% exposure to the US market.

The team says Singapore is another country that offers attractive REITs investment opportunities, due to the attractive dividend yields and relatively low leverage. “We also believe that the recent slowdown in growth and the lower-than-expected inflation data [in Singapore] would trigger another round of fiscal stimulus to stabilise the country’s economic growth.”

The fund was overweight on Hong Kong earlier this year. However, the ongoing civil unrest there has persisted longer than expected and the fund has shifted its position in Hong Kong to underweight. “We believe that the impact of the ongoing protest may have a material effect on the economy. Additionally, we are not confident that the issues will be resolved in the near term,” says Ng Chze How, head of retail of wealth distribution at Manulife Asset Management Services Bhd.

Nevertheless, it says the fund is not completely shying away from the Hong Kong market. In fact, investment opportunities might emerge in the near future. “Hong Kong REITs are currently traded at an attractive valuations.”

What are the key downside risks for REITs? Ng says one of them is a sudden reversal of headwinds including the US-China trade war, Brexit uncertainties and the civil unrest in Hong Kong. This would result in a shift in investor sentiment and investor monies would flow out of defensive sectors such as REITs.

“Another major risk would be if market volatility increases to the extent that debt markets become strained, causing interest rate spreads to widen. This would impact the REITs’ ability to finance their operations.”

Ng says it is difficult to predict the outcome of these events but it is likely that the US-China trade war would continue while global economic growth slows.

“However, we expect many central banks to remain vigilant and be ready to act [by introducing] more easing measures to support economic growth globally. And we think it will be some time before central banks resume interest rate hikes as the current headwinds facing the market will not be resolved in the near term.”

Ng also dismisses the possibility of a recession happening in the US anytime soon, even though the US Treasury yield curve inverted twice last month. An inverted yield curve is being used as a key indicator by market players to gauge if the US economy is heading towards a recession. Since 1950, all nine major economic recessions in the country were preceded by an inverted yield curve.

He says there are a few factors that give fund managers’ confidence that the US is not slipping into a recession as yet. “For instance, the fixed income spreads have not widened, especially in the high-yield bond markets. Additionally, the recent second-quarter earnings in the US were better than expected.”

On top of that, REITs have performed quite well after the last two major yield curve inversions that occurred in 2000 and 2006, says Ng. “REITs significantly outperformed the broader market in the following 12 months. We believe that the REIT sector will likely outperform once again in this environment as low interest rates and the defensive nature of the sector should continue to be viewed positively by investors.”

Get in touch with RHB Premier today.

This publication has been prepared by RHB Bank Berhad and is solely for your information only. It may not be copied, published, circulated, reproduced or distributed in whole or part to any person without the prior written consent of RHB Bank Berhad. In preparing this article, RHB Bank Berhad has relied upon and assumed the accuracy and completeness of all information available from public references and articles or which was otherwise reviewed by RHB Bank Berhad. Accordingly, whilst we have taken all reasonable care to ensure that the information contained in this article is not untrue or misleading at the time of publication, we cannot guarantee its accuracy or completeness or fairness of such opinions and make no representation or warranty (whether expressed or implied) and accept no responsibility or liability for its accuracy or completeness. You should not act on the information contained in this article without first independently verifying its contents.

Any opinion, historical account, personal profile, estimate or data contained in this article is based on information available as of the date of this article and are subject to change without notice. It does not constitute any advice, offer or solicitation by RHB Bank Berhad. This document and its contents are not intended to constitute an offer for sale and/or invitation to subscribe for or purchase or otherwise acquire any of the instruments referred to herein.

Disclaimer for Video and Podcast by RHB Asset Management:The podcast provided herein is solely for information purposes only. It does not take into account the specific investment objectives, financial situations or particular needs of any particular person.

This podcast does not constitute an offer, solicitation or recommendation to buy or sell or subscribe for any security or financial instrument or to enter into any transaction or to participate in any particular trading or investment strategy. Information contained in the podcast should not be relied upon when making investment decisions. You should seek independent legal or tax advice before making any investment decisions. Investments are subject to investment risks, including the possible loss of the principal amount invested. Value of the investments and the income, if any, may fall or rise.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein and it should not be relied upon as such. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance.

Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same. RHBAM does not guarantee that all risks associated to the transactions mentioned herein have been identified, nor does it provide advice as to whether you should enter into any such transaction. The contents hereof may not be reproduced or disseminated in whole or in part without RHBAM’s written consent.

This podcast has not been reviewed by the Securities Commission Malaysia. You should not act on the information contained in this podcast without first independently verifying its contents.

Disclaimer for Video and Podcast by Economics and Market Strategy:This report is prepared for information purposes only by the Economics and Market Strategy division within RHB Bank Berhad and/or its subsidiaries related companies and affiliates, as applicable (“RHB”). All research is based on material compiled from data considered to be reliable at the time of writing, but RHB does not make any representation or warranty, express or implied, as to its accuracy, completeness or correctness.

Neither this report, nor any opinion expressed herein, should be construed as an offer to sell or a solicitation of an offer to acquire any securities or financial instruments mentioned herein. RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for any direct or consequential loss arising from the use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without prior consent of RHB and RHB (including its officers, directors, associates, connected parties, and/or employees) accepts no liability whatsoever for the actions of third parties in this respect. Recipients are reminded that the financial circumstances surrounding any company or any market covered in the reports may change since the time of their publication. The contents of this report are also subject to change without any notification.

This report does not purport to be comprehensive or to contain all the information that a prospective investor may need in order to make an investment decision. The recipient of this report is making its own independent assessment and decisions regarding any securities or financial instruments referenced herein. Any investment discussed or recommended in this report may be unsuitable for an investor depending on the investor’s specific investment objectives and financial position. The material in this report is general information intended for recipients who understand the risks of investing in financial instruments. This report does not take into account whether an investment or course of action and any associated risks are suitable for the recipient. Any recommendations contained in this report must therefore not be relied upon as investment advice based on the recipient's personal circumstances. Investors should make their own independent evaluation of the information contained herein, consider their own investment objective, financial situation and particular needs and seek their own financial, business, legal, tax and other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report.

RHB (including its respective directors, associates, connected parties and/or employees) may own or have positions in securities or financial instruments of the company(ies) covered in this research report or any securities or financial instruments related thereto, and may from time to time add to, or dispose off, or may be materially interested in any such securities or financial instruments. Further, RHB does and seeks to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities or financial instruments of such company(ies), may sell them or buy them from customers on a principal basis and may also perform or seek to perform significant banking, advisory or underwriting services for or relating to such company(ies), as well as solicit such banking, advisory or other services from any entity mentioned in this research report.

RHB (including its respective directors, associates, connected parties and/or employees) do not accept any liability, be it directly, indirectly or consequential losses, loss of profits or damages that may arise from any reliance based on this report or further communication given in relation to this report, including where such losses, loss of profits or damages are alleged to have arisen due to the contents of such report or communication being perceived as defamatory in nature.

This podcast has not been reviewed by the Securities Commission (SC) and/or Bank Negara Malaysia (BNM).

RHB Bank Berhad 196501000373 (6171-M)